Both can make or break your property deal, so understanding these two key terms (and how they differ) is crucial.

As a boxing contest, ‘due diligence vs earnest money’ wouldn’t make for a fascinating main event. Understanding the nuances of each term, however, could help real estate investors close that knockout property deal they’ve been looking at.

In the United States, a growing number of real estate transactions now require these fees thanks to growing demand in the property market. US property experts Chase Properties have gone as far to say that ‘most sellers now ask for earnest money’, while Forbes have cited the widespread demand for due diligence fees in ‘all but very seller-friendly markets’.

Investors are under pressure to know exactly what they’re dealing with in a tight lending market which has experienced a notable decline in property financing options in 2023, according to research from PwC.

Buyers must study concepts like due diligence vs earnest money, know exactly how each process works, and the costs involved with them if they are to get the most out of their purchases.

Yet deeply understanding the nuances of the two terms can be tricky for those who may already feel overwhelmed by the intricacies of a home buying process or commercial property purchase.

It includes knowing exactly what agents and sellers are referring to when discussing the sale of their property. It also means understanding the difference between a down payment and soft deposit or between earnest money and due diligence money, and knowing how to act when confronted with each concept during the buying process.

In this piece, we shine a light on the due diligence vs earnest money question, what makes them different, and how each one might affect a crucial property deal.

Looking for a quick and secure way of funding earnest money for your next commercial property purchase? Sign up to Duckfund and find out how our low-cost LLC-based method can get you funding within 48 hours.

Purchasing real estate is a stressful process.

Due diligence helps soothe buyer concerns by letting them examine various aspects of a property before taking it on, including its physical condition, title deeds, issues with its surrounding environment, and related legal matters.

The due diligence period, then, is the time when the purchaser has to carry out these checks before finalizing an offer. This requires paying a due diligence fee, sometimes known as an option fee, and typically involves a property survey, a title search, and a new home inspection (including a HVAC check) for buyers.

The buyer then has the chance to negotiate any issues with the seller/homeowner at the end of the due diligence period. Let’s say a termite inspection uncovers a small mound on the premises: they might negotiate the cost of dealing with its removal, which both parties can then build into the deal.

When done well, the due diligence process builds confidence in the transaction and pushes the property deal much closer toward completion.

Sellers often demand compensation for the due diligence time period as they must take the property off the market for it to take place. This is where a due diligence fee kicks in.

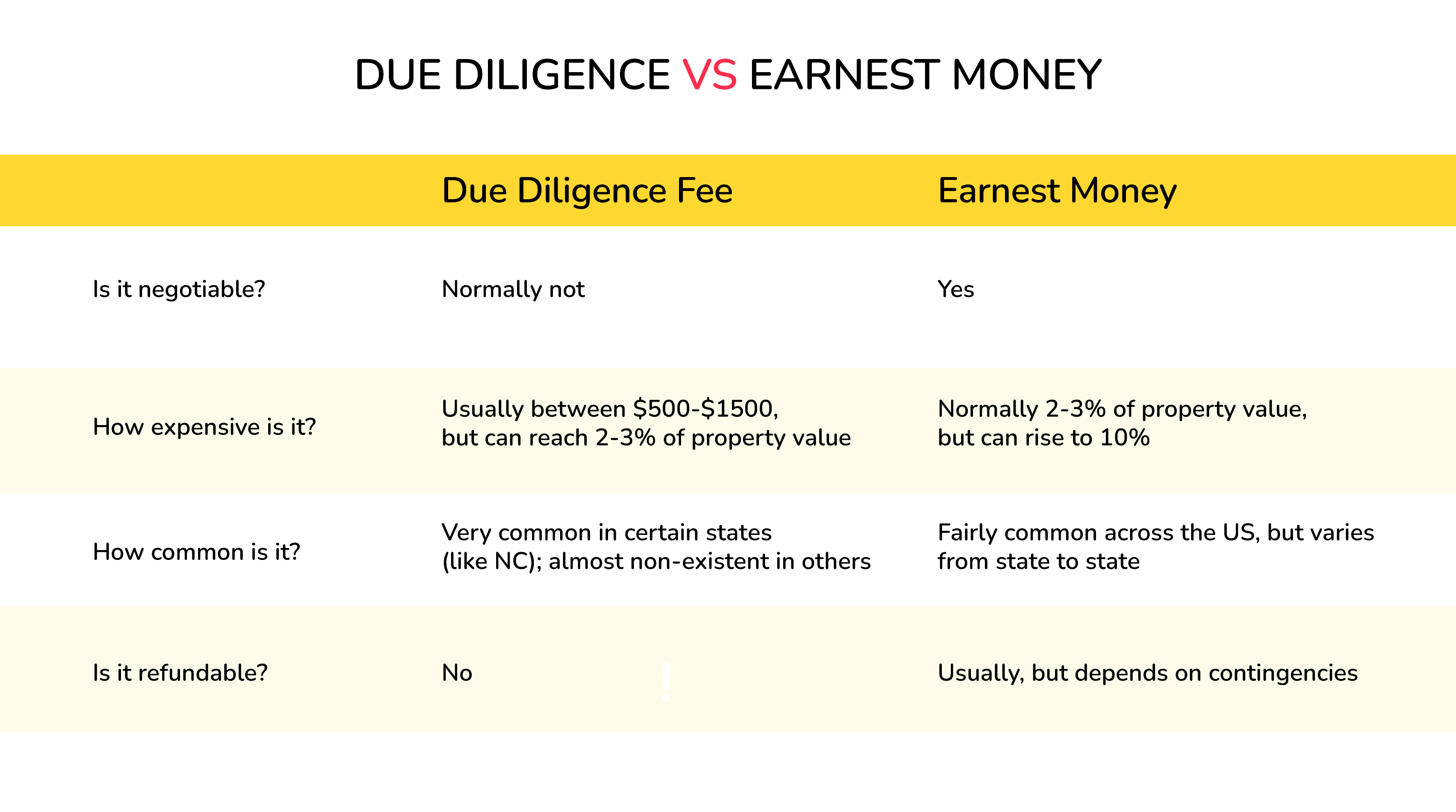

Due diligence money is most common in states like North Carolina, where the fee has been popular for over a decade. Although not compulsory, its use has started to grow in many other states, allowing buyers an opportunity to inspect large purchases before closing.

The size of the due diligence fee can vary greatly depending on numerous factors. Christina Howard of NC agency ESP Realtors pointed out via LinkedIn that “there is no standard due diligence in North Carolina. Instead the fee fluctuates according to the property price and marketing demand”.

Other online sources back this up, citing amounts of a few hundred dollars to a few percent of the purchase price of the home or commercial building across several states, making it difficult for investors to budget for.

If you’re not familiar with the term ‘earnest money’, then it may be because you’ve seen it classed as a ‘good faith deposit’ or ‘soft deposit’.

Either way, they amount to the same thing: a down payment that the buyer makes to show their commitment to buying a property.

Earnest money is normally calculated as a percentage of the purchase price and the buyer typically pays it upfront once they have agreed sale terms with the seller and signed the purchase agreement.

A real estate agent usually acts as the intermediary by holding the funds in an escrow account until the deal is finalized. If the deal falls through due to the buyer – and the reason isn’t among the contingencies listed in the contract – then the seller may receive the earnest money deposit as compensation.

If the deal completes, then the funds are simply applied to the investor’s down payment or closing costs.

Just as the United States is a diverse collection of semi-sovereign states, so the amount of earnest money varies between each one.

A region’s laws and regulations, culture, and local market trends all play a key role, to the point that the amount of earnest money in Texas is often completely different to that of, say, the North Carolina real estate market.

As a general rule of thumb, research by Investopedia states earnest money to be around 1 or 2% of the purchase price, but it can be as much as 10% in competitive markets.

Using an earnest money calculator is a useful way of getting an idea of how much an escrow agent could demand on behalf of a seller.

Both earnest money and due diligence fees can both be crucial components of real estate transactions, understanding the differences between the two will help an investor negotiate estate deals more effectively.

Here are the key distinctions between the two terms when we come to talk about due diligence vs earnest money.

As mentioned, a buyer will get their earnest money back should they back out of a deal for a reason highlighted in the purchase contract’s contingencies, or if the seller pulls out. That said, knowing how to claim back earnest money prior to closing is still important, in case the seller doesn’t play ball.

Due diligence money is normally not refundable even if the buyer decides not to proceed. This is because the seller is still undertaking an opportunity cost by taking their property off the market.

Go to buy a commercial property in any US state and you can expect to pay an earnest money deposit thanks to high demand across the nation.

Due diligence fees, on the other hand, are more common in some states than others. North Carolina, California, and Ohio have stringent DD requirements, but most don’t.

Due diligence fees tend to be much less of an issue for an investor because they may only be a few hundred dollars, with the typical amount being between $500 and $2,000.

This isn’t the case with earnest money, which may run into the hundreds of thousands for homebuyers, let alone commercial real estate.

It makes finding the relevant funds to smooth the wheels of a CRE property transaction a common pain point for investors.

Finding the earnest money or due diligence funds to declare a solid interest in a property can be an uphill struggle. A first-time home buyer, for example, may not have enough savings or lending options to get on the property ladder.

For commercial investors, the challenge can be even greater than buying a home, with capital locked up in other assets often being the main obstacle.

However, there are certain possibilities that investors might explore in order to meet these requirements.

Often high earnest money deposits are the work of realtors who want to make their own lives easier: the seller behind them may be open to negotiation.

Reasons for this might be that the buyer is willing to operate quicker in line with the seller’s demands, the buyer agrees to fewer contract contingencies, or if they agree to a higher purchase price.

Any of these situations would lead to a separate agreement between the two parties outlining the terms of the reduction.

Lenders of earnest money form a subsector of the property financing industry that provides short-term loans to investors short on funds.

Yet, they often charge high interest rates as they take advantage of the investor’s willingness to land their target property. PwC even lists interest rates and cost of capital as the top issue facing investors in 2023, with some deals reaching highs of almost 15%.

Source: PwC

While paying a premium might help push the deal over the line in some cases, many investors are put off by the potential interest accrued along a lengthy buying process.

Tough lending conditions have led to a new segment of the property financing market which involves forming a Limited Liability Company to make competitive CRE transactions like buying an office property in a popular downtown area possible.

LLC lending doesn’t require the credit checks or collateral demanded by traditional lenders because the LLC acts as a legal entity in the transaction, reducing the personal liability of the borrower, as well as the need for liens documentation. In fact, it doesn’t require any of the buyer’s capital, making it a useful way to buy commercial property without making a down payment.

The method focuses on speed, often getting funds ready within 48 hours after approval and the signing of a call option agreement. The LLC-driven lender then manages the escrow deposit and purchase agreement, allowing the investor to either walk away or complete the purchase.

For property investors getting to grips with CRE dilemmas like due diligence vs earnest money, LLC-driven soft deposit lending enables the quickest possible access to funds that buyers need to secure properties in competitive markets.

Need earnest money to lock in a commercial property deal right now? Duckfund’s easy application process takes just a few minutes and will help you secure funding in hours and get to that property before your rivals do.