From LOI to Close in CRE: How to Purchase Commercial Real Estate With Zero Upfront Cash

Buying commercial real estate is a costly endeavor in today’s competitive market.

Bidding is fierce, and sellers routinely ask for six-figure earnest money deposits before due diligence or talks with lenders start.

If you’re a buyer who’d rather not lock up that kind of cash to win a deal, then you’ll want to know how to purchase commercial real estate without committing capital up front.

Putting money down before and during a deal creates real problems when:

- Your capital is frozen in escrow in other deals while due diligence drags on for weeks

- A better deal surfaces, and you can't move on it because your cash isn't free

- Lenders want to see underwriting, but the seller wants to see money now

That’s the reality of commercial real estate for beginners, but it's not theirs alone. The same squeeze hits experienced sponsors juggling several deals at once

The difference is that they know how to sequence capital exposure so that cash is rarely the thing holding a deal up.

If you’re interested in finding out how to purchase commercial real estate with no money down, then you can find out in this guide. We’ll tell you how to protect liquidity at every stage, from the first deposit through to close, and how to minimize upfront capital across the deal lifecycle.

Looking for fast EMD financing to compete on your next CRE acquisition? Contact Duckfund to learn how soft deposit financing can help you capitalize on investment opportunities.

Is it easy to buy a commercial property in today’s CRE market?

CRE professionals are purchasing commercial real estate at a pace after years of caution.

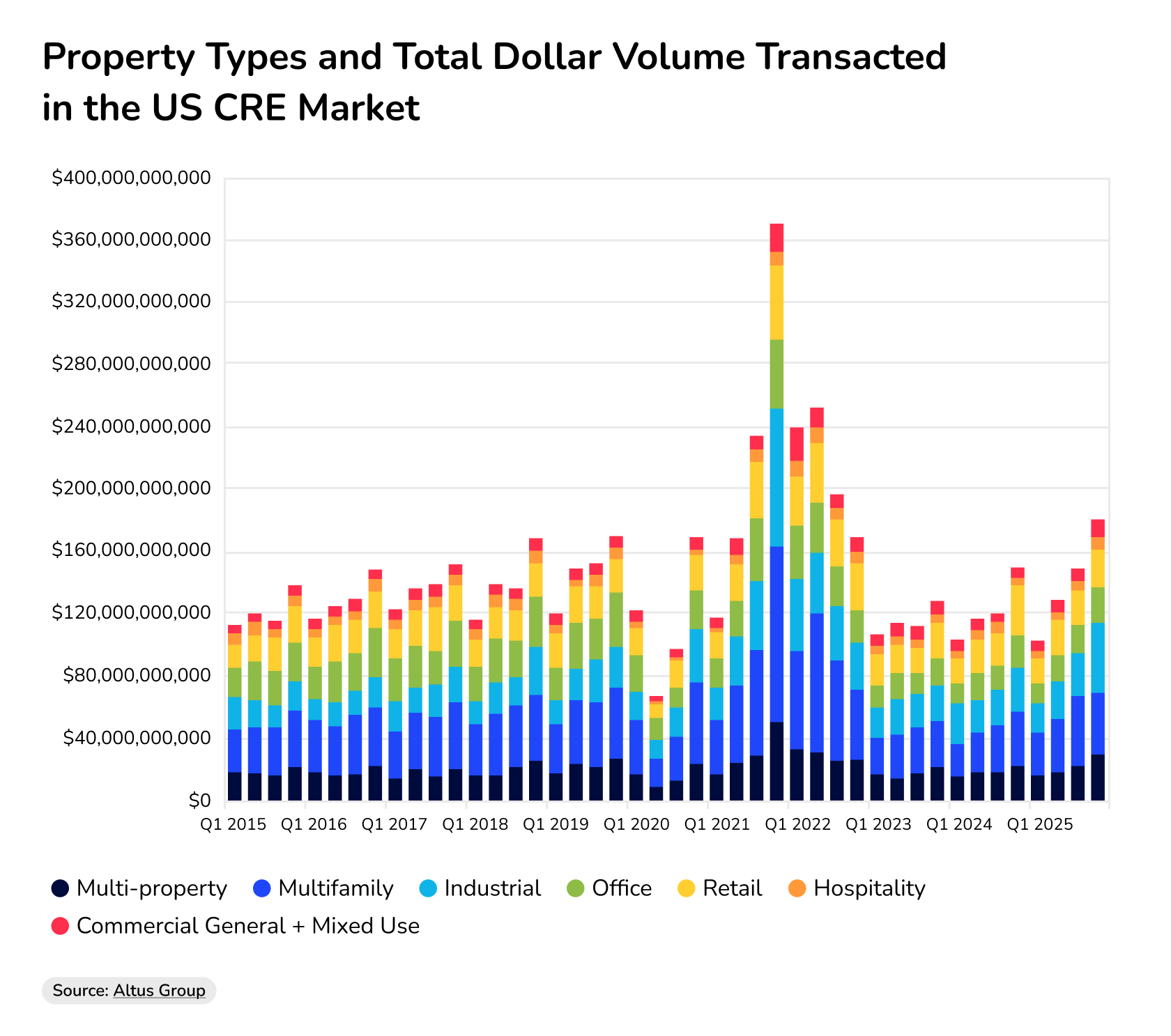

The US commercial real estate market recorded nearly $180 billion in transaction volume in Q4 2025 alone, according to CRE analyst Altus Group, with industrial (up 54.4% year over year) leading the way alongside strong activity in multifamily and multi-property assets.

Source: Altus Group

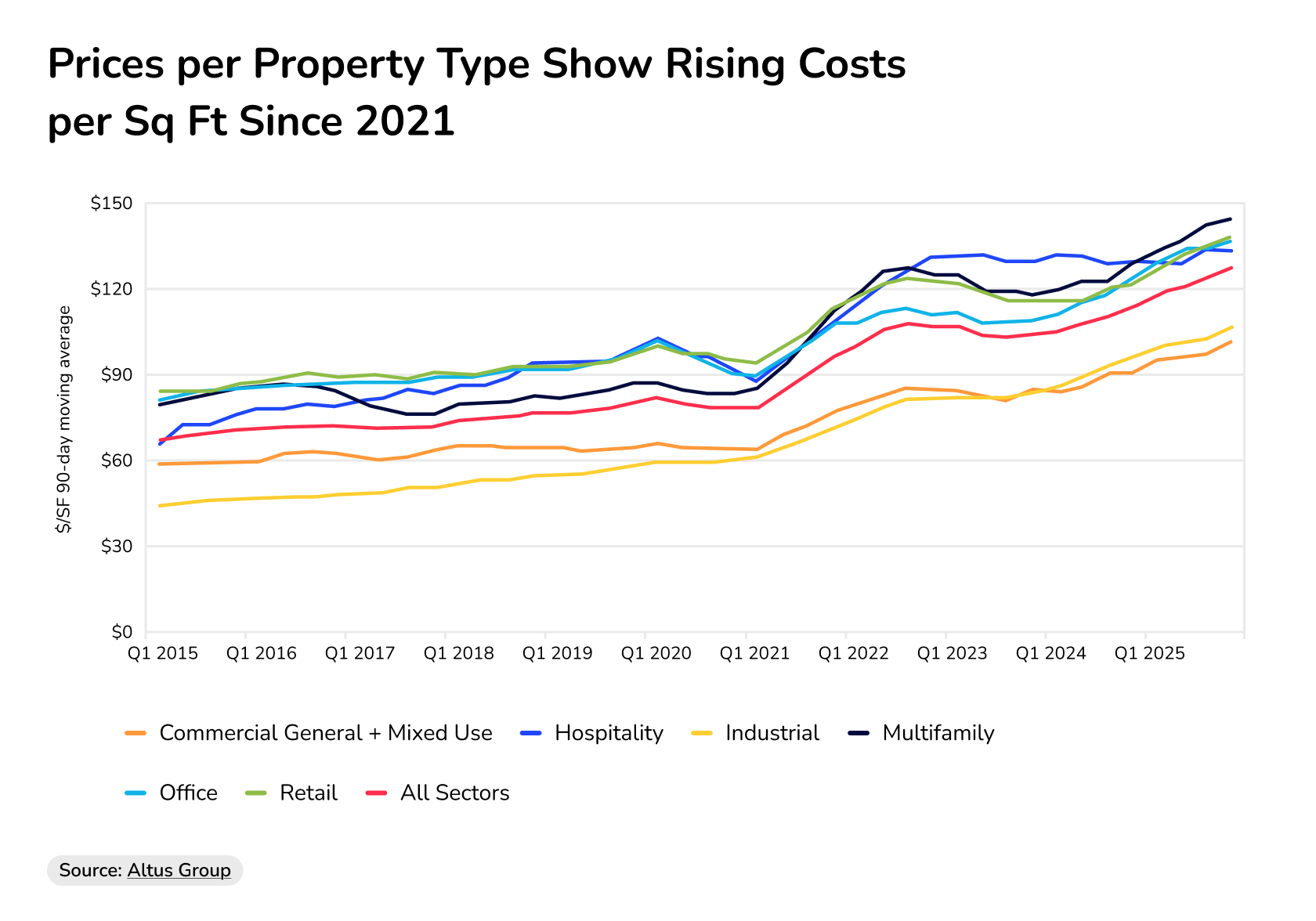

But a strong finish to 2025 doesn't mean deals are easy to find or cheap to enter. While transaction velocity is up, prices across commercial property types have been rising since the pandemic. Even office buildings, which saw a sharp dip in pricing during the pandemic, are staging a quiet recovery.

Source: Altus Group

In short, it’s a good time for selling commercial property. But what do these market conditions mean for buying business investment property? Transactions and prices rising simultaneously indicate increased buying pressure.

Competition from institutional buyers, private equity, and well-capitalized sponsors means that good assets move fast and underprepared buyers get priced out. Long-term success comes down to finding the right property for your portfolio and getting your finances in order.

But how do you find the right property in the first place?

What to look for when buying commercial property

Finding the right property starts with clearly defining your investment goals. Your target asset class, market, and expected revenue all follow from there.

From that foundation, the best practices in commercial property acquisition come down to one discipline: knowing exactly what you’re buying before you commit a dollar. This means doing thorough due diligence on four fronts.

Location and zoning: Is the property zoned for your intended use? Are there easements or restrictions that limit development or occupancy? Get this wrong and the asset may never perform the way your model assumes.

Financial performance: Review the financial statements, rent rolls, operating costs, and vacancy rates, then calculate the cap rate and net operating income. If the seller can’t produce clean financials, then it’s a big red flag.

Physical condition: HVAC, roof, structural integrity, and environmental status. A property condition report is the foundation of any property valuation.

Legal standing: Title, liens, pending litigation, lease terms. A real estate attorney should review all of this before you release your deposit.

Here's a quick purchasing commercial property checklist to run before you submit a Letter of Intent (LOI):

Purchasing commercial property checklist

- Zoning confirmed for intended use

- Environmental site assessment ordered

- Rent rolls and lease abstracts reviewed

- Financial statements (two to three years) obtained and analyzed

- Property condition report completed

- Title search initiated, liens identified

- Cap rate and NOI calculated against purchase price

- Real estate attorney engaged

- LOI drafted for submission

- EMD ready to be submitted to escrow or financed, so your own cash stays free.

Once you have all of the above checked off, you’ll know whether the deal pencils out. From there on, it’s all about moving fast, which is where your capital strategy comes in.

How much is the down payment for a commercial property?

Money moves fast and large in commercial real estate. When buying commercial property, small businesses, and first-time investors break out in a cold sweat when they’re asked to put down ten to 35 percent of the property value as a down payment. And that isn't even the first hit your capital takes.

Before serious negotiation starts, sponsors write a letter of intent and post an earnest money deposit (EMD) along with it. EMDs are as common these days in commercial real estate properties as they are for residential properties. But since CRE deals are bigger and often involve professional investors, the EMD carries more weight on both sides of the table. (Read more about earnest money deposits vs down payments here).

How much is earnest money and closing costs?

EMDs typically range from 1% to 3% in residential real estate. Earnest money for commercial property is much higher, between 1% to 5%, and as high as 10% or more for some types of commercial real estate.

Putting down 5% over a $5 million acquisition, you have $250,000 sitting in escrow before you’re even raising money towards the closing costs on commercial real estate.

These costs stack on top of the EMD. Buyer-side closing costs — everything above excluding the EMD and down payment — typically total 3% to 6% of the purchase price.

The EMD is wired first, then comes due diligence and associated costs. The down payment is put down at closing.

Unlike the down payment, which you can plan over months during the due diligence period, the earnest money deposit is immediate. It’s posted before your lender has even seen the deal.

That timing often poses cash flow problems for sponsors with operating costs or who are looking at multiple deals. And what happens if a buyer doesn't deposit earnest money? They lose the deal to a competitor with cash in hand.

Even if they do have the money available, they lock it up in escrow and lose the ability to move on to other CRE opportunities.

How to minimize upfront capital across the deal lifecycle

Having large cash reserves isn’t the only way to solve the liquidity problem. Experienced sponsors keep liquidity by deploying less of their own at each stage.

The deal lifecycle has three pressure points — acquisition, financing, and closing. There's a capital protection strategy for each one.

1. Acquisition stage: How to best finance the deposit

The first and most immediate move is the EMD. When a seller asks for a six-figure earnest money deposit, most beginners assume that you wire it from your own account. But traditional commercial real estate loans aren’t your only financing option.

Soft deposit financing (sometimes called EMD financing) lets sponsors borrow the deposit rather than post it from cash reserves. The mechanics are simple: a third-party lender funds the EMD directly into escrow, and the sponsor repays after closing.

There is a seller perception risk that comes with having your deposit posted for you, though. “Sellers prefer clean offers, so borrowing your deposit might signal financial weakness, “ says Matt Vukovich, real estate investor and commercial buyer at Matt Buys Indiana Houses. “Structure this financing quietly behind the scenes so the funds arrive instantly without adding extra contract conditions.”

Duckfund specializes in exactly this: financing a clean, fast offer that’s indistinguishable from a cash deposit in the eyes of the seller.

Duckfund’s soft deposit financing is available within 24 hours, with funding available from $25,000 upward and no collateral required. Its fees are structured as LP soft costs and passed through at closing, with rates that decrease for larger deposits.

If you're competing on a deal and don't want to freeze six figures in escrow, this is how you get to the negotiation table.

2. Financing stage: Read the market before you structure your debt

With the deposit secured and due diligence moving forward, the next capital pressure point is the financing itself, and how to finance a commercial real estate purchase depends heavily on the market you're borrowing into.

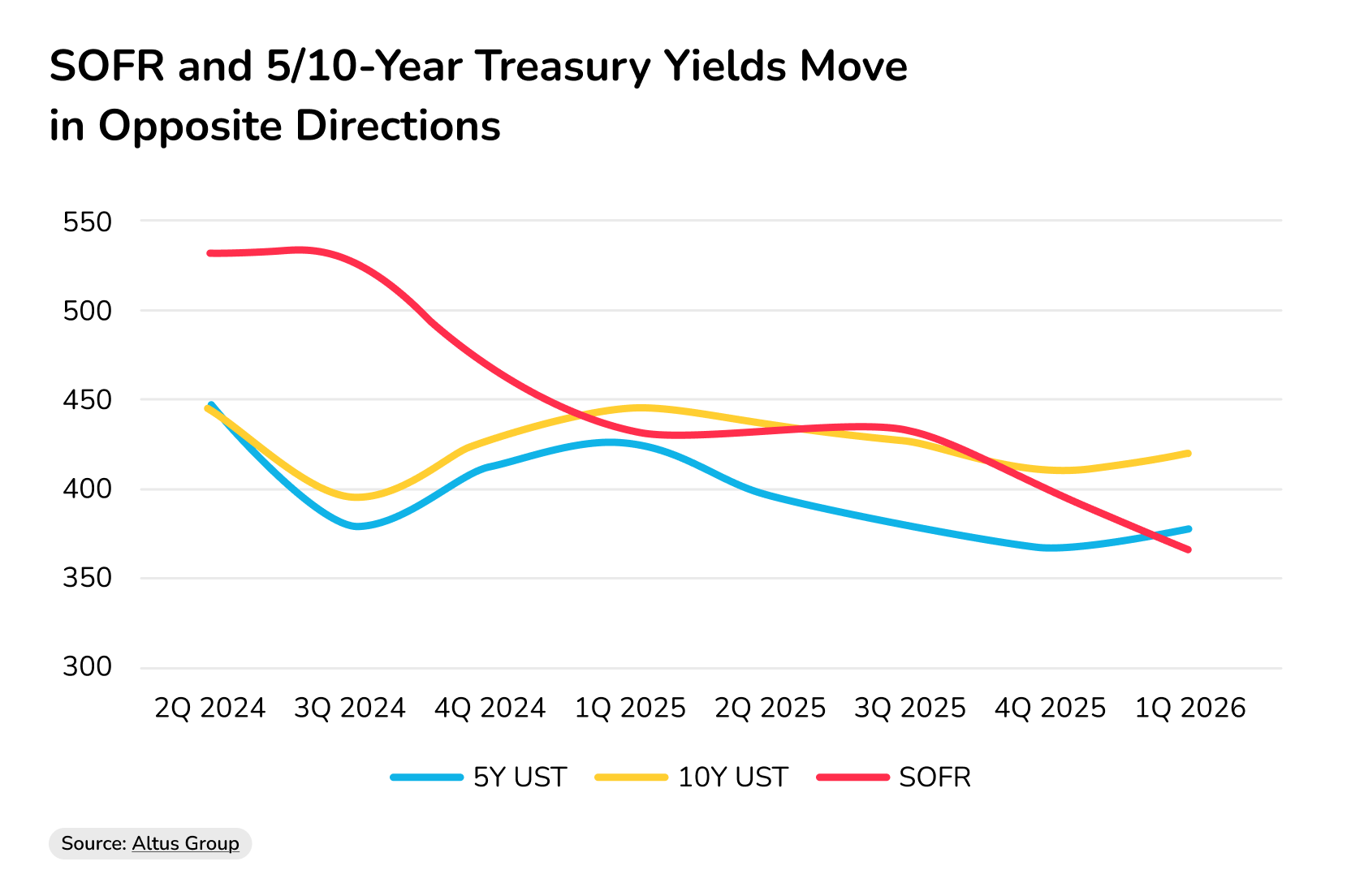

The CRE debt market is split, according to Altus Group's Q1 2026 US Debt Capital Markets Survey, with borrowing conditions favorable or costly depending on your loan structure.

Secured Overnight Financing Rate (SOFR) dropped to a quarterly average of 366 bps, lowering floating-rate costs. Meanwhile, 5- and 10-Year Treasury yields rose 10 bps, pushing fixed-rate costs higher.

Source: Altus Group

For buyers relying on conventional fixed-rate debt, that means higher interest rates, tighter margins, and harder underwriting. The smarter move is to match your financing structure to current market conditions rather than default to whatever commercial mortgage your nearest bank offers.

Below are five financing structures that simplify how to purchase commercial real estate, without overcommitting capital:

- Seller financing: The seller carries a portion of the purchase price at negotiated terms, bypassing institutional underwriting. Sellers also often benefit from tax advantages.

- SBA 7(a) loans: For owner-occupied commercial properties, SBA 7(a) loans offer up to a 90% loan-to-value ratio, making them well-suited for small business owners buying their own premises.

- Master lease options: Control the property with a fraction of the capital a purchase requires. The buyer leases with an option to buy, preserving cash during the hold period.

- Phased deposits: Negotiate a structure where capital goes hard in tranches as you clear due diligence milestones. This keeps your exposure proportional to your confidence in the deal.

- Equity partnerships: The sponsor brings the deal and operational expertise; capital partners bring the equity. Carried-interest structures let the sponsor share in the upside without matching the partner's cash contribution.

Equity partnerships effectively solve how to buy distressed commercial property without upfront capital. These assets are often underpriced precisely because they require immediate capital that individual buyers can't deploy fast enough – a capital partner supplies the speed, while the sponsor handles sourcing and execution.

Together, these five strategies help buyers move through the acquisition and financing stages without committing all their capital upfront.

That leaves one final pressure point: protecting your position at closing.

3. Closing stage: Protect leverage until the deal is done

Buyers sometimes go too hard and too fast during the acquisition stage – and lose the one thing that protects them if a deal deteriorates: the ability to walk away.

Eddie Martini, Strategic Real Estate Investment Advisor at Real Estate Bees, recommends “leveraging earnest money structures where deposits become non-refundable in phases instead of all at once — so that you can keep your EMD partially protected until you are 100% confident in closing the deal.”

That phased commitment is central to this guide. Finance the EMD, so the initial outlay isn't yours. Negotiate milestones before capital goes hard. Keep the door open to exit cleanly if the fundamentals shift.

Committing capital in tranches avoids the sunk-cost trap. Once a large deposit is locked in, Martini explains, buyers “can feel pressured to continue pursuing a deal even when new issues arise — such as tenant instability, deferred maintenance, or financing challenges.”

At that point, the money already spent starts driving the decision, rather than the merits of the deal.

Buyers who consistently find the best commercial property investments for passive income are the ones who stay competitive and put down money in tranches without surrendering optionality.

Finance your next CRE deal without freezing your capital

Now you know how to purchase commercial real estate with minimal upfront costs, and that committing capital in phases is about far more than getting by when you’re short on cash.

Experienced sponsors commit in tranches to stay liquid enough to keep moving, both on the deal in front of them and the next one they haven’t found yet.

Finance the deposit, structure the debt to match market conditions, and keep capital going hard in tranches as conviction builds. Do that, and you’re never forced to choose between closing a deal and chasing a better one.

Duckfund is built for exactly that kind of optionality. Your deposit is funded straight into escrow within 24 hours (with no collateral), with fees structured as LP soft costs that pass through at closing. So your offer looks clean to the seller, while your own capital stays free for you to do what you do best: find the next opportunity.

Fund your next deposit without worrying about your cash flow. Apply for EMD financing with Duckfund and get funded within 24 hours.

Frequently Asked Questions (FAQs)

Still have questions about how to purchase commercial real estate? Below are answers to the ones that come up the most.

What is a soft deposit in commercial real estate?

A soft deposit — also called an earnest money deposit (EMD) — is a cash payment made by the buyer to demonstrate serious intent to purchase. It’s held in escrow from the time the letter of intent is signed until the deal closes or falls through.

How many units are considered commercial property?

A residential property with five or more units is generally classified as commercial real estate for lending and regulatory purposes. Properties with one to four units, including single-family homes and small multifamily, are treated as residential.

What is the difference between corporate real estate and commercial real estate?

Commercial real estate refers to income-producing properties that are bought, developed, and managed as investments. Corporate real estate refers to property occupied and used by a company for its own operations, such as headquarters, warehouses, or branch office space.

What is the 2% rule in commercial real estate?

The 2% rule states that a property's monthly rental income should equal at least 2% of its purchase price to generate positive cash flow. The rule is more commonly applied to small multifamily assets than to other commercial real estate, where cap rates and net operating income are better benchmarks.

How do you find commercial real estate investors?

The most direct way to find commercial real estate investors is through CRE networks, syndication platforms, and family office databases. Industry events, broker relationships, and direct outreach via LinkedIn are also standard sourcing channels.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence