Is Mezzanine Financing Worth It for Commercial Real Estate Investors?

Nothing can be more frustrating for a commercial real estate (CRE) investor than a project stalling due to funding gaps.

However, with traditional lenders still cautious due to regulatory pressures, balance sheet constraints, and the looming debt wall of maturities, such funding gaps threaten to persist.

In such situations, mezzanine financing of CRE can plug funding gaps left by senior debt while helping investors benefit from higher leverage and flexible deal structures. It has especially become an integral part of commercial property development finance.

But is mezzanine debt in CRE the best approach when you encounter funding gaps as an investor or developer?

We will answer this question by considering the following:

- The current state of mezzanine financing in commercial real estate

- Pros of mezzanine debt in commercial real estate

- Cons of mezzanine financing in real estate

- Factors to consider before using mezzanine financing in commercial real estate

- Securing the funding you need with Duckfund

Do you want a CRE financing partner that will support you as you build a profitable CRE portfolio? Sign up today for Duckfund to get the funding you need.

1. The current state of mezzanine financing in commercial real estate

Mezzanine financing stands in the capital stack between senior debt and equity financing.

It helps investors and developers fill funding gaps left by senior debt financing before resorting to equity financing.

In the current market, senior debt loans (first mortgage, asset-backed loans, senior corporate loans, etc.) often come to a 60-70% loan-to-value (LTV) or loan-to-cost (LTC) ratio, leaving borrowers with a shortfall of between 30-40% of the purchase price.

Mezzanine financing can bridge this gap, taking the LTV or LTC ratio to between 80-90% and reducing the equity portion of the capital stack. In other words, it can cover about 10-30% of the total cost.

Renewed interest in mezzanine financing

As said above, the cautiousness of traditional lenders continues to contribute to the interest in mezzanine financing as a way to reduce equity dilution.

But interest in these securities also comes from the supply side. In other words, while CRE developers and investors are pursuing them, investors are also willing to buy into them.

“Mezzanine debt financing in Europe has attracted a diverse group of investors, including specialized mezzanine funds, insurance companies, and pension funds,” according to Asset Physics, a real estate and infrastructure investment analysis blog.

There are two factors behind this interest. First, as we will see below, mezzanine financing pays higher interest rates than senior loans and other debt instruments. Second, the position of mezzanine debt in the capital structure aligns with the risk-return profile of many buy-and-hold equity-focused investors.

But this is not a mere European phenomenon.

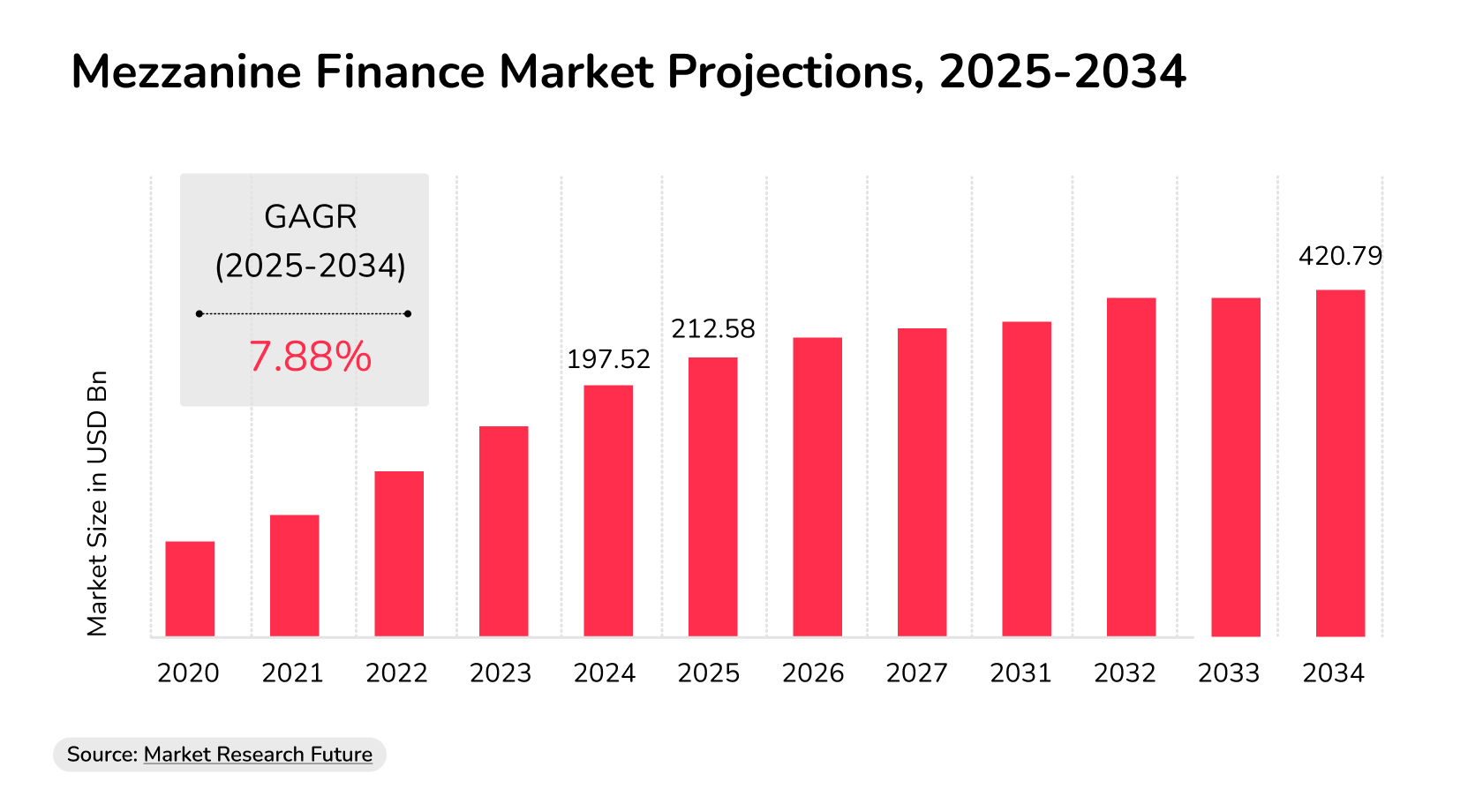

The global mezzanine finance market is projected to grow from $212.58 billion in 2025 to $420.79 billion by 2034 at a compound annual growth rate (CAGR) of 7.88%, according to Market Research Future, a market research firm.

Source: Market Research Future

Also, they expect real estate to continue to be the primary user of mezzanine debt, even as North America leads the pack due to strong private equity activity and well-established financial institutions.

How mezzanine financing works

How does mezzanine financing work?

In terms of usage, they are typically employed for larger acquisition deals and development projects. Many lenders will require a minimum loan amount of up to $2 million before they can finance a mezzanine deal.

Mezzanine lenders have preference over equity holders, while they are subordinated to senior debt lenders. Thus, the cost of capital is higher than that of senior debt and lower than that of equity.

In the current US market, the cost of capital of mezzanine financing is between 12% and 20%, according to The Fractional Analyst, a real estate intelligence platform.

The higher cost of capital when compared to senior debt also reflects the fact that mezzanine debt is unsecured by the property itself. Rather, mezzanine lenders receive a pledge of equity in the entity that owns the property. This means mezzanine lenders can attempt to take control of the entity in the case of a default.

Mezzanine financing deals can be structured in three different ways:

- Subordinated debt: A mezzanine debt is like a typical CRE loan with pre-agreed interest rates.

However, since mezzanine debt is subordinated to senior debt, lenders will only receive coupons after senior debt holders have been settled.

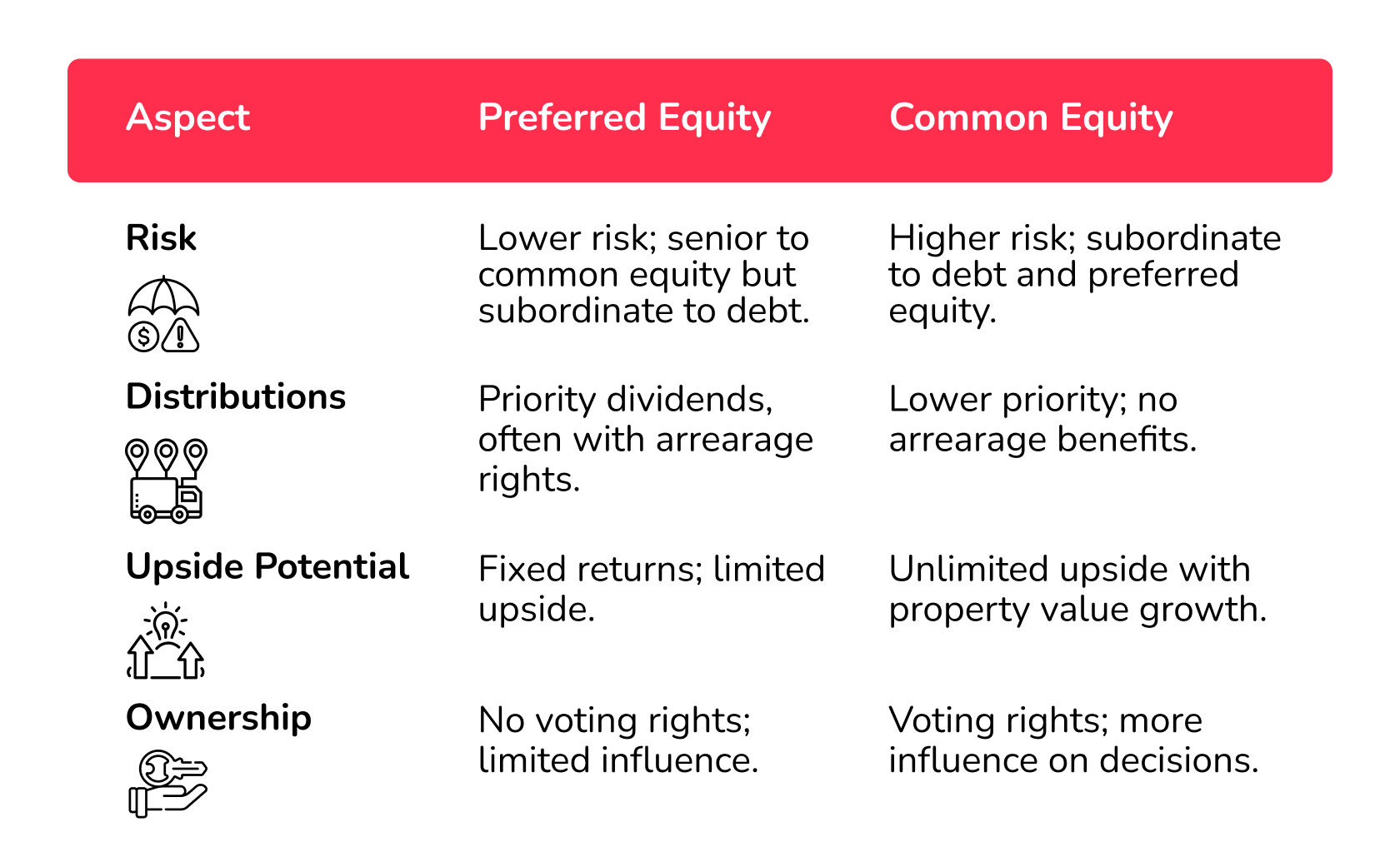

- Preferred equity: A mezzanine debt can also be structured as a preferred equity deal, which is an equity investment. In this case, the preferred equity holder has a form of ownership in the property that does not come with voting rights (unlike common equity).

Preferred equity holders earn a fixed or target rate of return (which makes preferred equity similar to debt), and they are paid before common equity holders.

Preferred equity vs common equity real estate

- Convertible instrument: A mezzanine financing deal can also be in the form of a convertible debt instrument. In other words, the deal may have an equity kicker – an option to convert the debt into equity along the line.

Irrespective of the structure, mezzanine debt boils down to one thing: it is the middle of the road between senior debt and common equity.

Also, it usually has a loan term between one and five years.

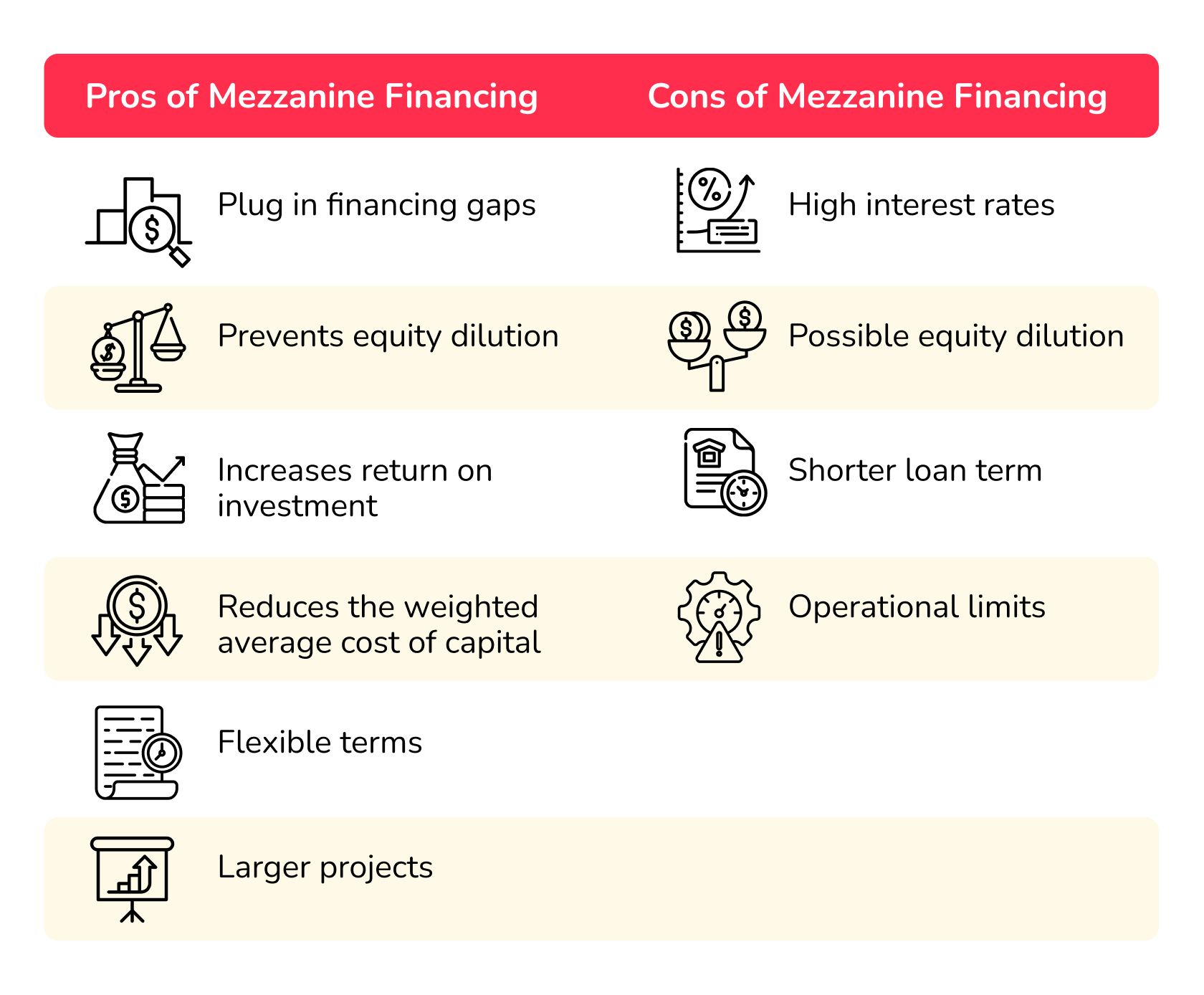

2. Pros of mezzanine debt in commercial real estate

On the demand side, mezzanine financing has become popular because it provides important advantages to CRE developers and investors. Below are some of the most crucial ones:

- Plug funding gaps: As we have seen, mezzanine financing is one of the common ways CRE developers and investors deal with the funding gaps created by senior debt.

- Prevents equity dilution: For a senior debt of 70% LTV or LTC, the borrower would have to rely on equity contribution for 30% of the project cost. However, with mezzanine financing, the borrower could get an additional 20% of debt financing, leaving only a 10% shortfall for equity contribution.

- Higher return on investment (ROI): But why is 10% equity contribution better than 30%? In one word: leverage. The more of other people’s money you use to finance your CRE projects, the more return you can get from your real estate investment.

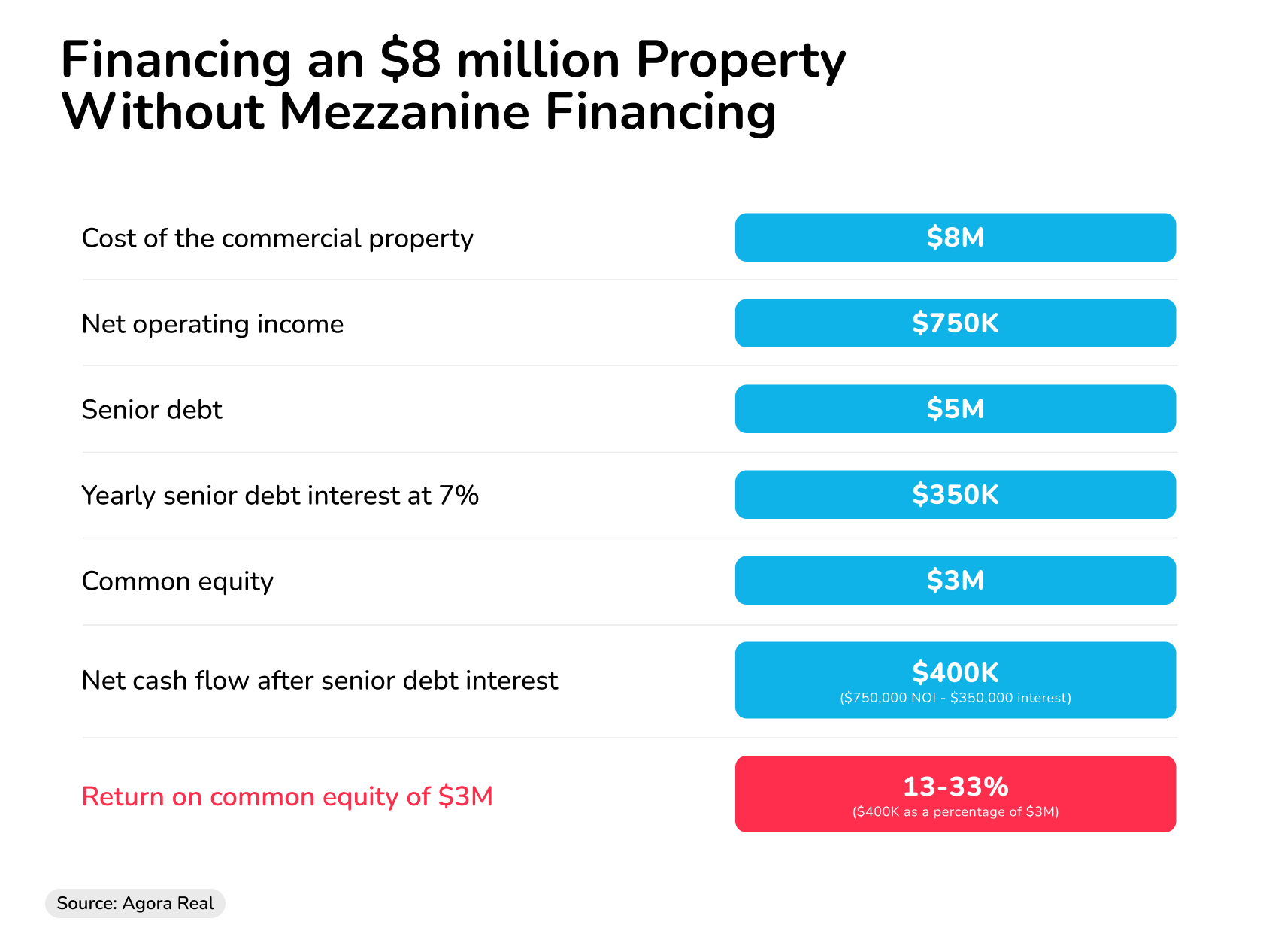

Consider this example from Agoral Real, a real estate software solution.

Suppose a commercial property costs $8 million and has a net operating income (NOI) of $750,000. The senior debt is $5 million at an interest rate of 7% per year (yearly interest payment of $350,000). This leaves a $3 million funding gap. If you don’t use mezzanine financing, you need an equity contribution of $3 million.

The net cash flow of this deal (after interest payment) is $400,000. Given that the equity contribution is $3 million, your ROI is 13.33%.

Source: Agora Real

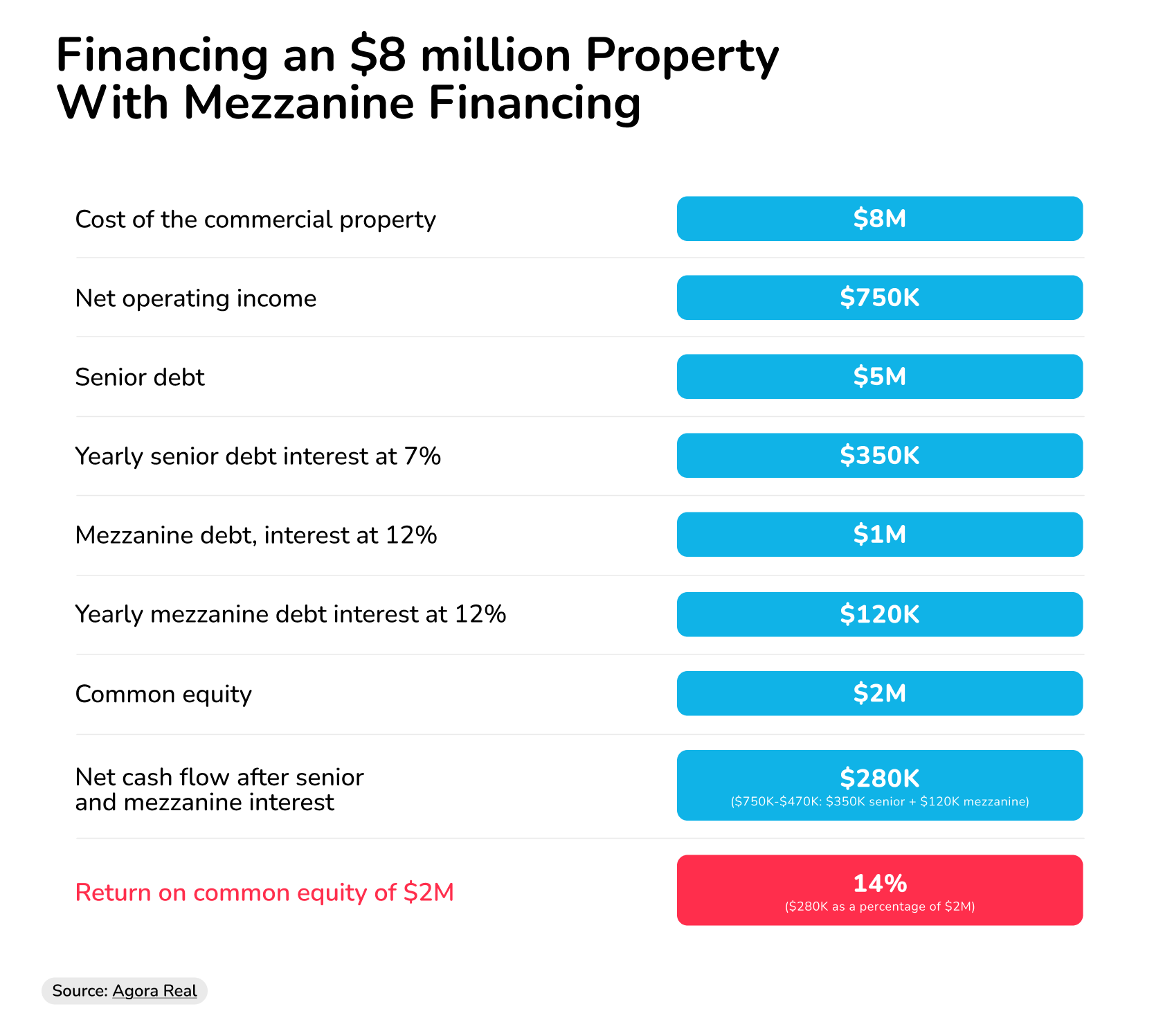

What changes if you introduce a mezzanine loan for CRE? Let’s see.

Suppose you take a mezzanine loan of $1 million at 12% interest rate (for a yearly interest payment of $120,000). Now, the equity component is only $2 million.

The net cash flow after senior and mezzanine debt is now $280,000. However, with an equity component of $2 million, that gives us an ROI of 14%.

Source: Agora Real

Put simply, by reducing the amount of equity contribution needed, mezzanine financing can increase your ROI.

- Lower weighted average cost of capital (WACC): Debt is generally cheaper than equity. Also, interest payments are tax-deductible, which creates a tax shield that further reduces the cost of capital.

Thus, by reducing the equity contribution needed, mezzanine financing reduces the WACC for a CRE project.

- Flexible terms: Mezzanine financing also introduces some flexibility that you can’t find with senior debt.

First, you can defer interest payments at the early stage of the construction project until you have started generating revenue.

Second, you can explore payment-in-kind (PIK) interest, which involves capitalizing interest (adding it to the loan balance to be repaid at the end of the loan term). This is useful if you depend on seasonal cash flows or experience cash flow delays.

- Larger projects: By filling up funding gaps left by senior debt, mezzanine financing makes it easier to finance large acquisitions and construction projects without too much equity dilution.

3. Cons of mezzanine financing in real estate

Yet, certain disadvantages remain with mezzanine financing. Below are some of the most important ones:

- High interest rates: Mezzanine financing rates are more expensive than those of senior debt. While the former tend to range between 5-8%, the latter is usually between 12 and 20%.

- Possible equity dilution: If a mezzanine deal is structured to be convertible to equity, then equity dilution can occur down the line if the lender exercises the equity kicker. As we have seen, such dilution can reduce ROI and increase WACC.

- Shorter loan term: While senior debt can have terms between five and 30 years, mezzanine debt has a shorter loan term (between one and five years).

- Operational limits: Mezzanine loan agreements include financial and operational covenants designed for the protection of lenders.

The former includes maintaining a minimum debt service coverage ratio (DSCR), having a maximum LTV, seeking lenders’ approval for new debt, and using excess cash flow to pay mezzanine lenders.

The latter includes restricting dividend payments to equity holders and seeking lenders’ approval for large capital expenditure, major property decisions, and ownership changes.

Pros and Cons of Mezzanine Financing in Commercial Real Estate

4. Factors to consider before using mezzanine financing in commercial real estate

Given that there are pros and cons of using mezzanine debt in commercial real estate, how should you approach it as a CRE investor or developer?

To answer this question, let’s highlight some factors to consider before deciding if mezzanine financing is right for you or not.

Can you qualify for mezzanine financing?

Since mezzanine debt is unsecured, lenders will pay attention to your creditworthiness and financial stability.

“Lenders will scrutinize your track record, experience, and overall financial stability,” according to The Fractional Analyst. “Additionally, the quality of the asset and the strength of the local market play a significant role in determining approval and pricing.”

Thus, before seeking out mezzanine debt, ensure you can even qualify for it in the first instance.

Can you manage the additional risk that comes with higher leverage?

Though higher leverage can increase ROI and reduce WACC, it also means higher risk. Senior debt holders can foreclose on the collateral if the borrower defaults. Also, mezzanine debt holders can foreclose on the equity interest and push for asset sales in the event of default.

Before taking on more leverage, you need to be sure that cash flows are stable enough to avoid possible defaults and foreclosure. Though interest payments can be deferred with subordinate financing, such deferrals are not indefinite, and the chickens will come home to roost.

Does the difference in ROI and WACC justify the higher interest rate?

In the example above, we saw how mezzanine debt can increase ROI from 13.33% to 14%.

However, with all the financial and operational limitations that come with mezzanine debt, you need to ask if this difference in ROI is worth it.

The same thing applies to WACC. Yes, mezzanine debt can reduce WACC, but for every deal, you need to question if the difference in WACC is worth the burden of the financial and operational limits.

Is there a viable path to refinance, sell, or recapitalize before maturity?

Since mezzanine debt has a short term (1-5 years), you must have a plan for the capital repayment at maturity.

This can involve refinancing the loan with permanent debt (a mortgage loan, for example), selling the asset, setting aside cash reserves, recapitalizing (bringing in new equity investors), or exploring CRE bridge loans until more permanent financing is available.

You need to be sure that any of these other forms of financing is viable before deciding to use mezzanine debt.

Do market conditions require mezzanine debt?

With current market conditions (60-70% LTV and LTC ratios), mezzanine debt makes sense.

However, we have experienced market conditions with higher LTV and LTC ratios (up to 90%). Even today, many government-backed loan programs can provide up to 90% LTV and LTC ratios.

Before embracing the higher interest rates of mezzanine debt, you should be sure there are no better options in the market. If there are opportunities to get much higher LTV ratios with senior debt, mezzanine debt may be unnecessary.

5. Securing the funding you need with Duckfund

Duckfund provides senior debt financing of up to $500 million for development, pre-development, value-add, and redevelopment projects in multifamily, build-to-rent, industrial, hospitality, and other CRE sectors. These loans have up to 75% LTC and 70% LTV.

You can supplement this with preferred equity, taking your LTC to 85%, and leaving only 15% equity contribution.

In addition, you can secure earnest money deposit (EMD) financing of up to $5 million. You can complete an EMD application in two minutes and get the needed cash within 48 hours.

Duckfund also provides EMD financing for multiple deals at once, allowing you to pursue as many projects as you want, even when you have liquidity challenges.

With Duckfund, you have an all-in-one CRE financing partner that can provide you with the funds you require at each stage of your CRE investment and development journey.

Are you ready to build a CRE portfolio in the Sunbelt and major US markets? Sign up today for Duckfund for timely EMD deposit, senior debt, and mezzanine debt financing.

Takeaways

- Mezzanine financing fills the gap left by cautious senior lenders, pushing total leverage from 60–70% LTV up to 80–90%.

- Higher leverage can boost ROI and lower WACC, but it comes at the cost of higher interest rates, shorter maturities, and tighter covenants.

- Mezzanine financing sits between senior debt and equity, offering flexible structures such as subordinated debt, preferred equity, or convertible instruments.

- Mezzanine lending only works with a clear exit plan, including refinancing, sale, or recapitalization before its 1–5 year maturity.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence