Mobile Home Park Financing: 6 Ways to Finance Your Project

It’s a red-hot industry, but to get started, you must know where your money is coming from.

Just five years ago, the phrase “mobile home financing" probably wouldn't have sparked much interest in the commercial real estate (CRE) world.

Yet it’s now become a hot topic as investors looking to enter one of the industry’s high-growth CRE asset classes are facing big hurdles, including:

- Freeing up funds tied up in other deals

- Navigating tighter lending conditions, especially from traditional lenders

- Understanding the nuances of financing for specialized investments like mobile homes.

If you’re one of them, you're not alone. Many CRE developers are now recognizing the potential of this sector, but are seeking clarity on how to finance new deals.

Read on to find out where to look for the right mobile home financing for your project, including innovative lenders and new funding options.

Don’t miss out on hot mobile home financing projects, or any other type of CRE investment. Contact Duckfund to find out how we can help you make your next project a success.

Why invest in mobile home park land right now?

Mobile home park land is a compelling investment for investors in uncertain times because it offers that all-important quality: stability.

Often referred to as "manufactured housing" within the industry, or more colloquially as "trailers," these communities represent the nation's largest source of unsubsidized low-income housing. They provide shelter for 21 million Americans in 2025, according to Business Insider.

Modular homes, too, are factory-built housing, but they differ from mobile homes in that they adhere to local building codes and are typically placed on permanent foundations. They’re also more expensive to construct.

A mobile home purchase is an attractive option for many homebuyers priced out of traditional site-built homes as the housing crisis intensifies. Between 2014 and 2024, the number of manufactured homes shipped nationwide surged by over 60%.

Unlike many other real estate sectors, manufactured home park land demonstrates remarkable resilience, thanks to several crucial factors.

High occupancy rates and rent growth in mobile homes

Anyone building mobile homes on a plot of land will need to be confident that they can fill them once complete.

Mobile homes are performing exceptionally well in this regard. In the US, the national occupancy rate held steady at 94.8% for the third quarter of 2024, according to mortgage loan providers Northmarq, reflecting the rate for the whole year. Rents grew by 7.2% for the year, as part of a 20% spike since 2021.

“Demand (for manufactured homes) is through the roof, supply is barely catching up, rents are accelerating, and occupancy is as high as it’s ever been”, reported Multi-Housing News at the end of 2024.

All point to mobile home park land becoming one of the best-performing CRE markets over the next few years.

High return on investment (ROI)

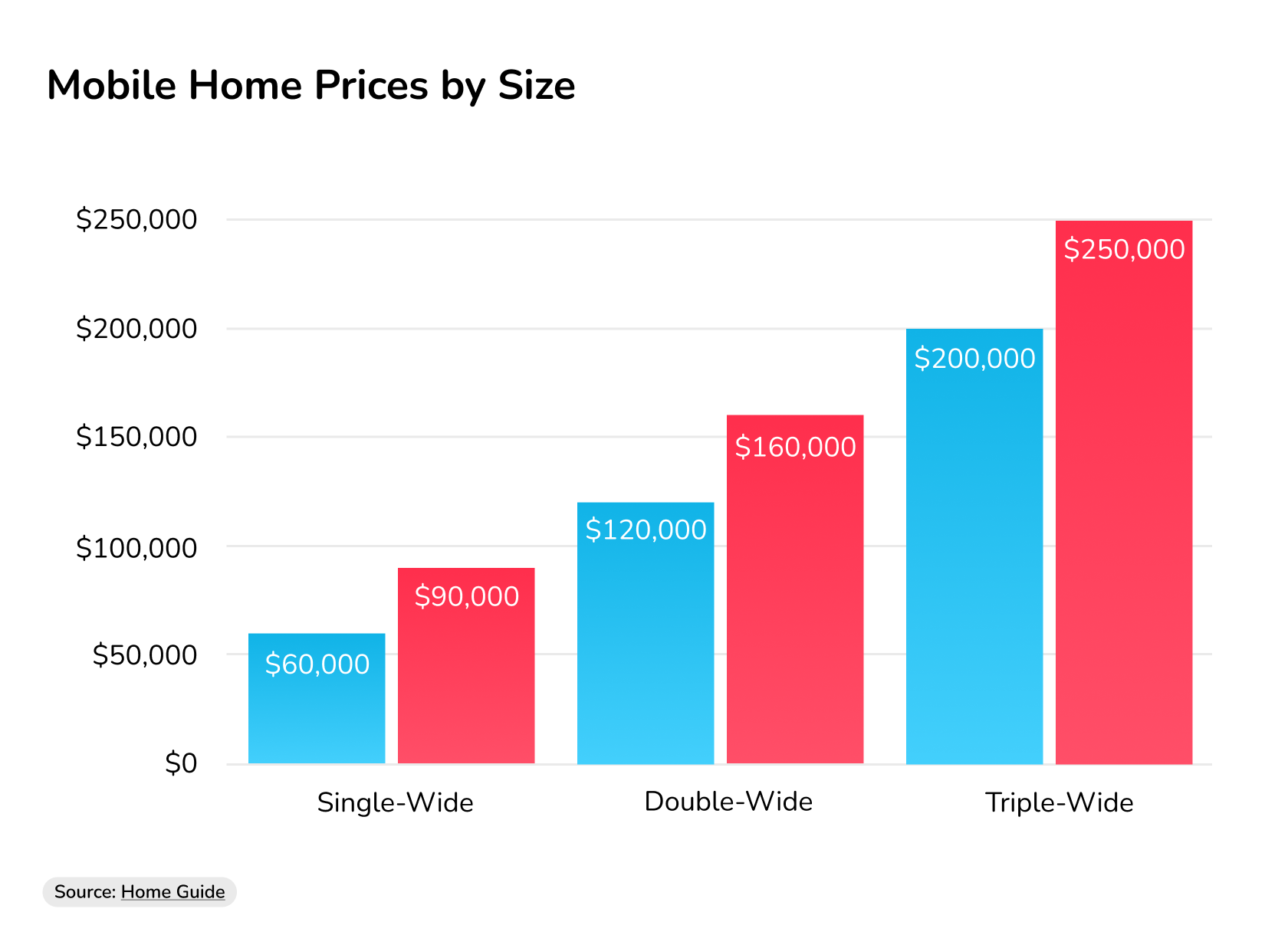

Should an investor choose to build and sell, then they are likely to make a sizeable return. The average cost of a new home on mobile park land is $124,300, with triple-wide units often hitting the $250,000 mark.

Source: Home Guide

With the cost of building mobile homes costing as little as $50,000-$150,000, depending on the size, there’s scope to make money for a savvy developer.

If they build and rent, then, as well as impressive rental rates, they will benefit from lower operational overheads compared to, say, apartment complexes or retail spaces. Tenants generally maintain their homes, which reduces the landlord's expenses.

Finally, the land beneath these communities holds strong potential for value appreciation. The increasing demand for affordable housing options and the reliable income generated from lot rents means mobile home park land is fast emerging as an excellent opportunity for high ROI.

“Our belief is that the best place to weather the potential storm is as a homeowner or investor, and my experience in the 1990s indicates that the retention or acquisition of MHC/MHP/TP is the best choice for 2025,” says Douglas Danny, President at Lost and Found Properties Inc.

How to get financing for a mobile home development

The first major step in turning an investment intention into a real property deal is to scope out financing.

Knowing who finances mobile homes and what kind of products they offer is a key move – even if you’re not successful this time around, the knowledge you acquire will stand you in good stead for next time.

1. Traditional commercial mortgage

Banks and other traditional financial institutions are a trusted mobile home financing source, and they typically offer long-term loans, or mortgages, ranging from five to 20 years. These can follow a variable or fixed rate, depending on the deal.

Loan-to-value (LTV) ratios generally fall between 70% and 80%, so buyers must have the rest ready as liquid capital to make up the down payment.

These mortgages are well-suited for stable, existing mobile home parks with a strong operating history.

If, as an applicant, you don’t have this, or if you have a patchy credit score, then their stringent underwriting process may mean your eligibility is hit, and the application is rejected.

Some banks may insist on recourse provisions, such as a personal guarantee, which will mean that you are personally liable for the loan amount instead of your business.

2. CMBS Loans

Commercial Mortgage-Backed Securities (CMBS) are a type of non-recourse loan, meaning you are generally not personally liable for the debt.

These loans can be attractive for larger deals and can also be pooled together and sold as bonds to investors.

CMBS loans can, however, be more complex and often include a "defeasance" clause, which outlines a potentially costly loan process to sell or refinance the property before the loan term ends.

3. Agency Financing ( via Fannie Mae & Freddie Mac)

Fannie Mae and Freddie Mac have specific programs designed for financing manufactured housing communities.

These loan programs often offer competitive interest rates and longer terms compared to conventional mobile home mortgages, yet they also require the property to meet certain standards.

Let’s say, for example, that you can’t demonstrate a consistent history of high occupancy rates and stable rent collection. An agency financing provider may see this as grounds for rejecting your manufactured home loan bid.

Investors focused on well-managed parks that meet the provider’s criteria will probably find this a useful funding avenue with favorable terms and a quicker application process.

Many types of investors, however, will find that they are blocked out by tough management demands.

4. Seller financing

In this scenario, the seller of the mobile home park land acts as the lender, providing financing to the buyer.

The terms of seller financing are negotiated directly between the buyer and seller and can be more flexible than traditional financing. Buyers who don’t qualify for conventional loans or who are looking for creative financing solutions often find this attractive.

However, the terms (interest rate, monthly payment schedule) can vary widely and may not always be as favorable as market rates. There has also been some pushback from traditional lenders, who may view properties with seller financing as riskier and something that impacts future refinancing options.

5. Private Lenders

Private lenders, such as private equity firms or individual investors, offer another avenue for financing.

They can be more flexible in their underwriting criteria and may be willing to fund projects that traditional lenders might not.

Yet, interest rates from private lenders are typically higher, and loan terms may be shorter. This option can be useful for borrowers who need quick funding or have unique circumstances, but it’s always smart to approach these with careful consideration of the cost involved.

6. Construction loans

Construction loans are short-term financing specifically designed for the development of new mobile home parks.

Developers use the funds to cover the costs of building infrastructure and setting up the community. Once the construction is complete and the park is stabilized, borrowers will usually refinance into a longer-term permanent loan.

For developers looking to build new mobile home parks, construction loans are a necessary first step in bringing their vision to life. These projects often require significant upfront capital, and managing the earnest money deposit can be a key early hurdle.

Duckfund's equity product is designed to smooth this initial phase, providing investors with the necessary funds for the earnest money deposit, allowing them to secure the land while they arrange their longer-term mobile home financing.

This can be particularly beneficial in competitive markets, giving investors the agility to act quickly and secure promising development opportunities.

What are the steps to financing mobile home park land?

In a competitive market, securing mobile home financing for land involves a structured approach, so follow this step-by-step guide to getting the best funding possible.

1. Define your vision (and numbers)

Clearly outline the scale and financial parameters of your mobile home park land project. What are your acquisition or development goals, and what's your budget? Having a good idea of how much commercial land is worth is essential here.

2. Explore financing avenues

Investigate the various commercial real estate financing options. Resources like Duckfund’s recent CRE market report can point you toward the right commercial lenders and mobile home loan structures for this niche.

3. Organize your financials

Compile all necessary financial documents, including balance sheets, income statements, and project pro formas.

4. Connect with capital sources

Engage with lenders who have experience in commercial real estate, specifically those familiar with mobile home financing.

5. Apply and negotiate

Submit your application and be prepared to discuss and refine the loan terms to suit your project’s needs.

6. Secure the deal with earnest money

Be ready to put down earnest money to demonstrate your commitment and secure the land during the financing process.

Remember: the more you can put down, the more likely you are to secure the deal! Earnest money financing can help you dramatically up your bid here.

7. Finalize and close

Conduct thorough due diligence and meet the closing costs to secure your financing and the land.

Can you finance mobile home real estate ahead of rivals? Find out how with Duckfund

Imagine this scenario: you’ve found the ideal piece of land for your next mobile home park development.

Yet another keen investor is also eyeing it, and they're ready to lay down their earnest money deposit and make an offer.

You want to act fast and beat them to it, but find that you don’t have access to the capital to do it. By the time you've liquidated assets or navigated traditional, slower financing options, it's too late. Your rival has snapped up the land.

If you want to make your mark in one of the US’s fastest-growing investment markets, then speed and agility are critical. This is where Duckfund makes the difference.

Our Earnest Money Deposit (EMD) financing empowers you to move swiftly and secure prime opportunities ahead of the competition.

We provide rapid approval, often within 24 hours, and can wire the EMD to escrow quickly, ensuring you don't lose out to slower-moving buyers.

Our flexible terms, including reduced interest rates starting from the fourth month, are specifically designed to support developers like you.

With Duckfund, you can leverage our financing to place stronger offers, negotiate better terms, and secure that sought-after mobile home park land before others can.

We've helped facilitate over $1.5 billion in property acquisitions – let us help you secure your next deal.

Don’t want to miss out on prime mobile home real estate? Sign up for Duckfund and find out how we can make sure you have the funding to make it happen right now.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence