Multi-Family Property Investing: 6 Common Pitfalls and Solutions for Them

Multi-family property investing attracts capital no matter the financial weather. Why? It’s a market that continuously shows strong demand, promising stable cash flow and lower risk compared to other commercial real estate assets.

But finding investment opportunities in multi-family real estate isn’t easy in today’s CRE landscape. Even seasoned real estate investors find themselves facing challenges like:

- A capital crunch from lenders setting tight requirements puts many properties out of financial reach

- Property scarcity with institutional investors buying up assets and compressing cap rates

- Operational complexity grows with rising insurance costs, utility expenses, and compliance requirements

Challenging as these obstacles may seem, they’re made harder by the macroeconomic backdrop of high interest rates and recession fear brought on by the new administration.

Yet savvy CRE professionals continue to build a strong multifamily portfolio despite market downturns. You can, too – if you successfully overcome some common challenges and do your due diligence.

From how to value multifamily property to efficiently managing your assets, let’s look at the 6 main challenges of multifamily property investing and how to solve them.

[Duckfund's soft deposit financing helps real estate investors act swiftly on multifamily investment opportunities. Borrow up to $100 million for debt and equity deals across all property types.]

Challenge #1: Rising operational costs

Operational costs are climbing, a recent survey by the National Multifamily Housing Council (NMHC) shows. “The current confluence of high insurance costs, interest rates, and construction and material costs makes the development and operation of rental housing a financial challenge,” said Sharon Wilson Géno, who is President of the NMHC.

“A more stable insurance market will help keep costs in check, which, in turn, will improve housing affordability and potentially lower rental housing costs for residents,” she added.

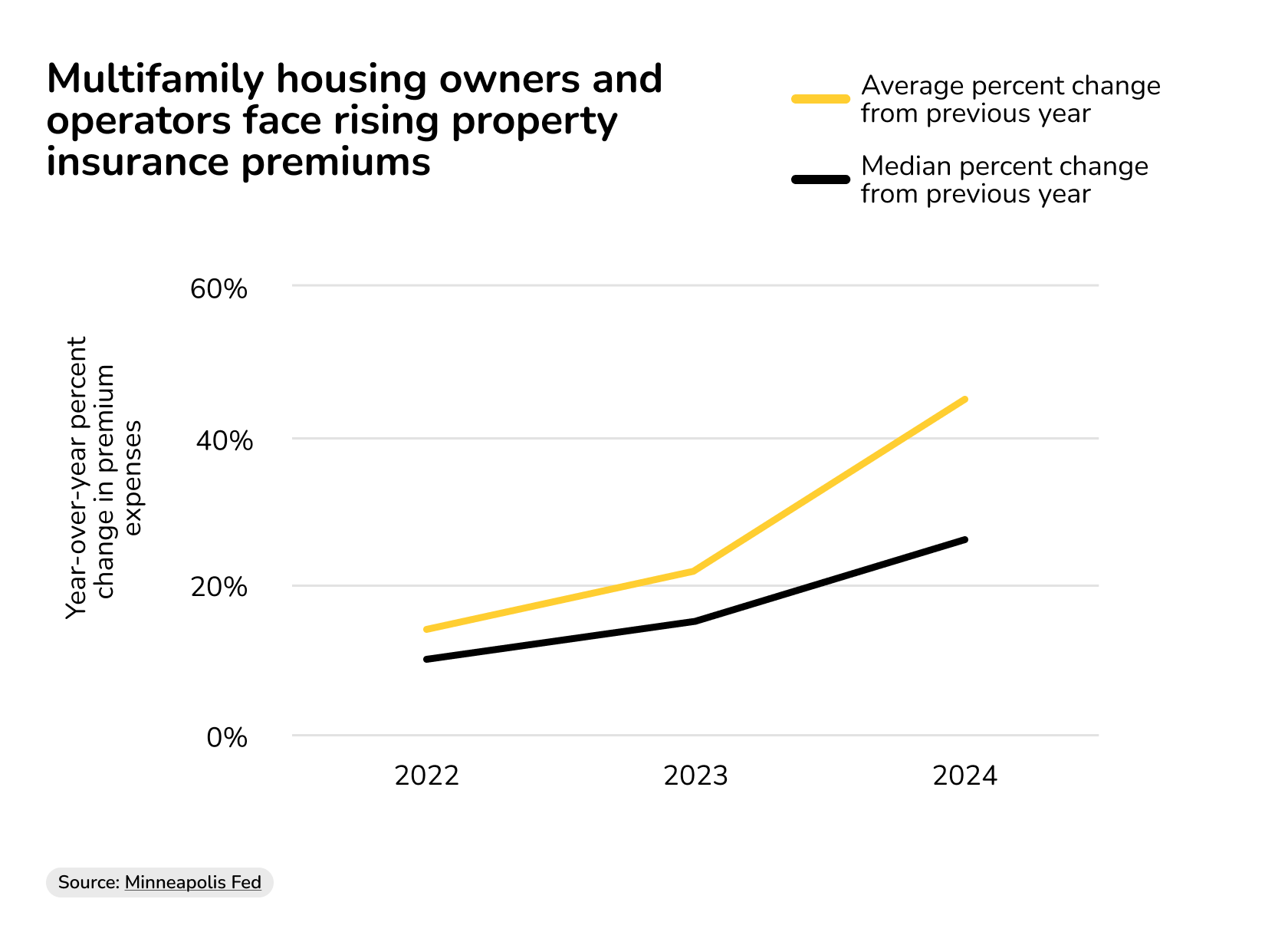

However, data shows the market is headed elsewhere: from 2021 to 2024, property insurance premiums doubled on average, a survey from the Minneapolis Fed revealed, far outpacing inflation.

Source: Minneapolis Fed

The regional reserve bank further found that over 50 percent of the overall operating expense inflation for multifamily housing owners since 2020 is due to increasing property insurance premiums.

These statistics show just why operational costs are such a critical component of how to evaluate a multi-family investment property.

The solution: Increase operational efficiency

In the face of ever-rising operation expenses, what’s an effective multifamily investment strategy that investors can implement? One effective cost saver is property technology, or proptech.

Predictive maintenance tools using AI and IoT sensors have the power to streamline property management. These digital solutions enable proactive issue identification before problems escalate, helping save costs while improving tenant satisfaction.

Installing at least one smart device brings 65% of multifamily properties 10% to 20% in operating expense savings, according to analysts from Parks Associates.

Another smart way to cut costs is centralizing property management. From using cloud-based admin systems to consolidating local offices, centralization streamlines processes, increases productivity, and cuts costs.

Centralization is not just a smart strategy in this asset class – it’s the new norm. 80 percent of third-party multifamily managers are centralizing operations, according to joint research by NMHC and marketer 20for20.

Challenge #2: High Initial Capital Requirements

Breaking into multi-family property investing takes substantial upfront capital, which can be prohibitive for investors without good access to CRE financing options.

Nowadays, 20-25% of a property's purchase price is typical for a down payment when investing in multifamily units, CRE management firm Lotus Property Services reports. The required down payment for an apartment building can even be over 35%, depending on the borrower’s credit score, financial situation, and risks involved.

These high capital requirements are an obstacle, especially for first-time investors or those looking to expand their real estate portfolios. So how to buy a multi-family investment property when you don’t have the cash upfront?

The solution: Change your capital stack

How to raise money for multi-family investing in a tight lending market? One way to overcome capital constraints is to form strategic partnerships. Leverage your network and attend industry events to meet potential investors when raising money for multi-family property investing.

And how to buy multi-family investment property when you can’t rely on partners or need to move on a deal quickly? For those situations, look to innovative financing solutions like Duckfund’s equity and debt financing. It can be used for LP/Co-GP equity, preferred equity, and senior debt so that investors secure deals with reliable capital.

Anna Kogan, Founder and CEO of Duckfund, explains their approach: "We've structured our offering as a service product, not a loan. This means developers can access the capital they need for earnest money deposits without impacting their debt capacity or existing lending relationships."

Duckfund's equity solutions complement their earnest money deposit financing for a comprehensive approach to the capital stack.

Challenge #3: Market Competition from Institutional Buyers

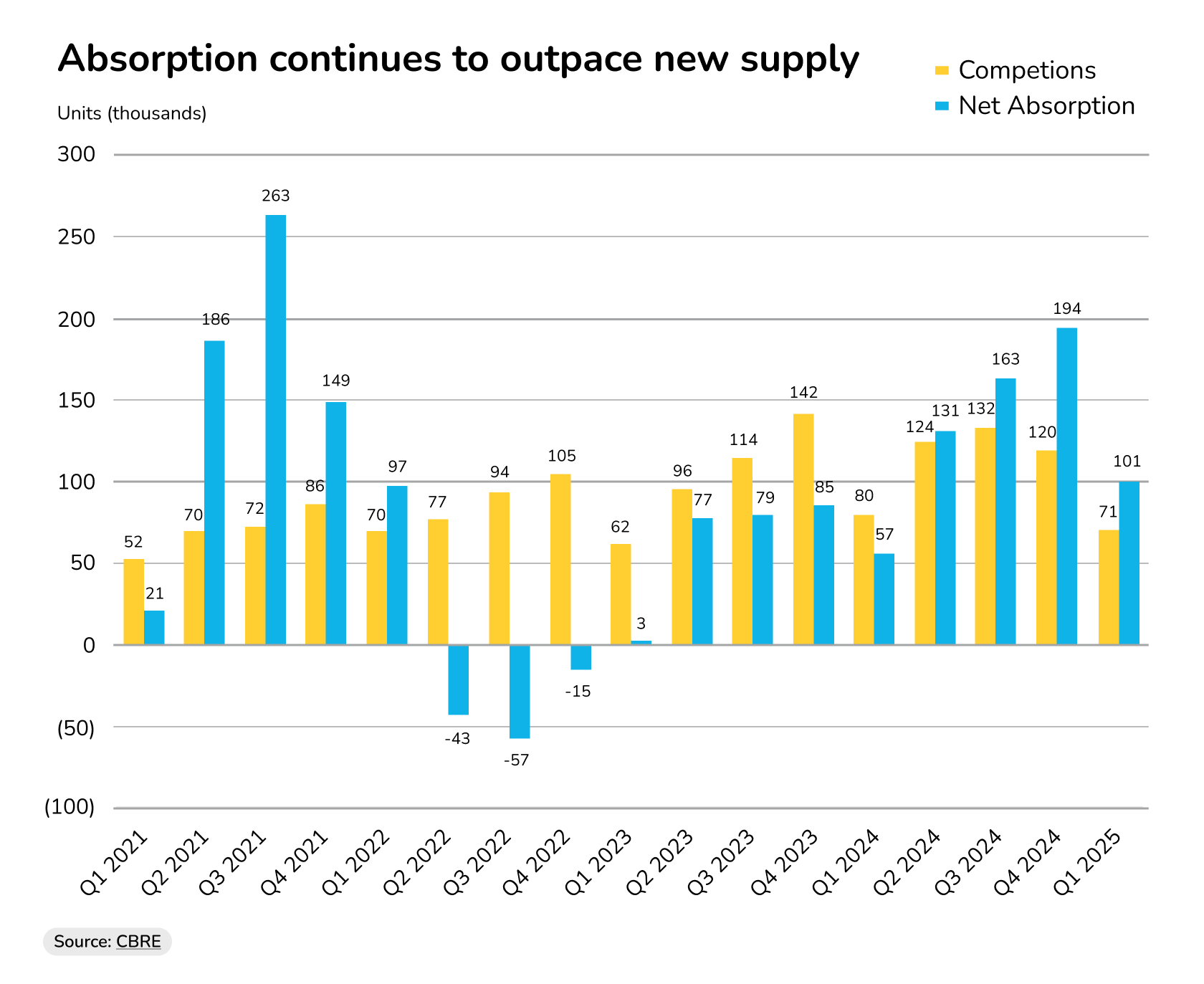

Multifamily assets are in high demand and vacancy rates are dropping, according to data from CBRE, which saw net absorption in Q1 of 2025 increase by 77% year-on-year and to triple the pre-pandemic average.

With the construction pipeline for multi-family homes shrinking in the coming quarters and rental demand strong, competition for existing stock is fierce. It becomes even more difficult as institutional investors return to the market in force.

Absorption continues to outpace new supply

Source: CBRE

“Interest rates are beginning to trend downward, encouraging large institutions and REITs to re-enter the market, Austin Graham comments. The First Vice President & Associate Director of the investment firm Matthews adds, “These entities have amassed significant capital earmarked for multifamily acquisitions, setting the stage for a surge in transaction activity.”

Graham expects that “Once market confidence improves, competition for assets may intensify rapidly, rather than gradually.”

The solution: Invest in overlooked rental property

This shift in buyer dynamics puts individual buyers at a disadvantage – but only in situations where having deep pockets counts.

Large funds looking for a steady return on investment through rental income typically chase apartment complexes with a large number of units. The more units, the more renters, and the steadier the return.

Filling an institutional investment portfolio with single-family properties isn’t just more work but single-family rentals also present higher cash flow risk. Even multi-family units like duplexes and triplexes fly under these funds’ radar.

For smaller investors, these types of investments look much more interesting. Comparing duplex vs triplex investments, more rentable units offer more stable cash flow, though the cost to build a triplex is higher.

In fact, the rental market is full of overlooked properties. Properties in emerging neighborhoods and in need of renovations are another type of investment considered too risky for institutional money. For individual investors, they present a great value-add opportunity.

How to find vacant properties before the institutional competition? Identify areas with strong fundamentals but without the property values that come from institutional competition.

Challenge #4: Refinancing with higher interest rates

Refinancing is a common practice in commercial real estate. But when interest rates shoot up after years of CRE depreciation, this financing strategy can become a problem.

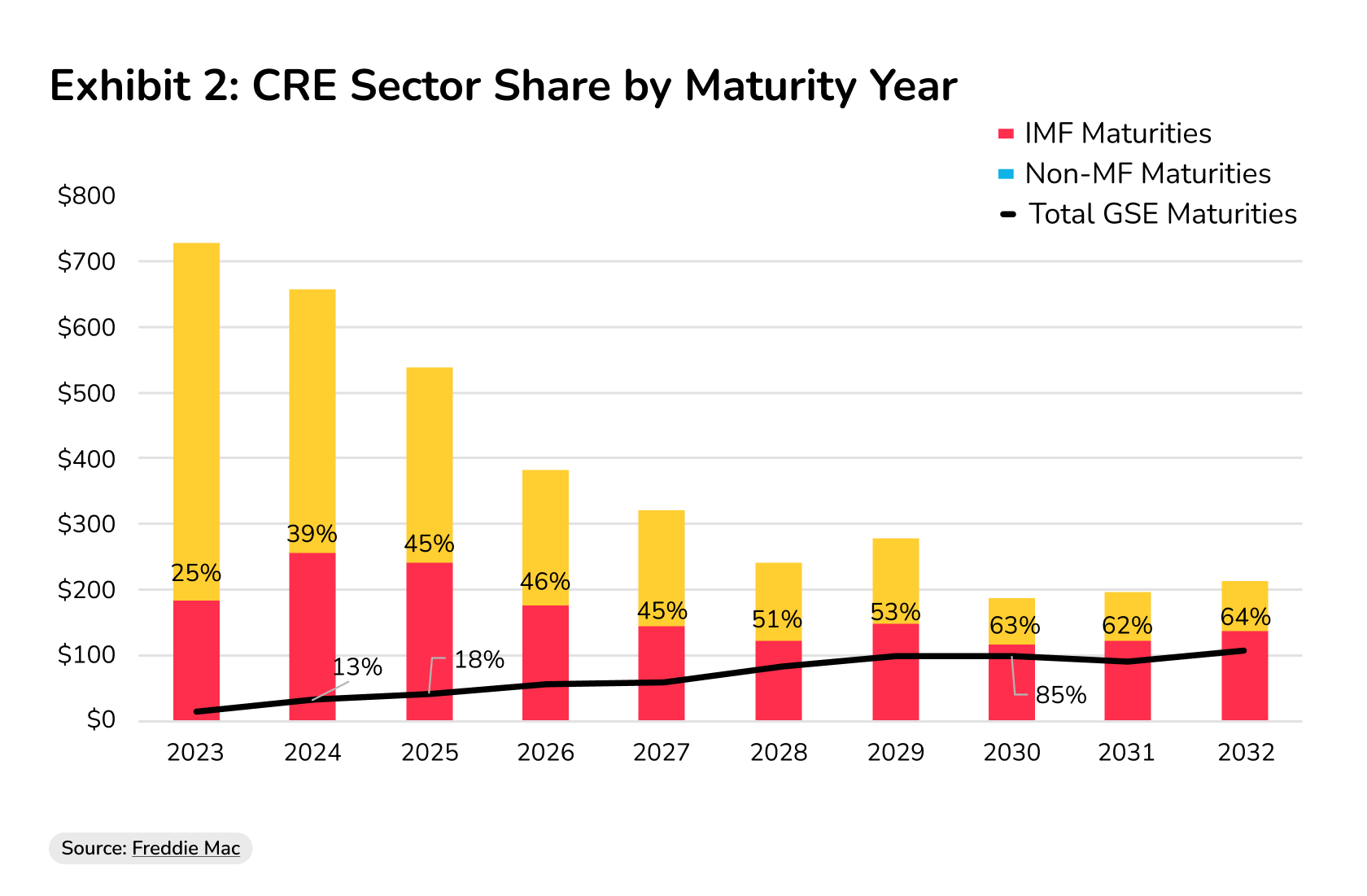

Over $500 billion of outstanding commercial real estate mortgages are set to mature in 2025, according to a Freddie Mac report. Roughly 45% of those maturing loans are backed by multifamily assets. Investors’ hope that interest rates would come down by 2025 has proved futile.

Source: Freddie Mac

“While the Federal Reserve cut its short-term interest rate target by 100 basis points in 2024, longer-term interest rates increased over the same time by an equivalent amount,” the Mortgage Bankers Association’s SVP and Chief Economist, Michael Fratantoni, commented. “Commercial property owners who had sought to take advantage of a drop in rates stemming from Fed cuts were disappointed,” Fratantoni added.

The economist predicts that “Longer-term rates are likely to remain range bound for the foreseeable future, and the path to work through these maturities will remain challenging.”

Yet longer-term multifamily debt might be able to withstand refinancing at higher interest rates, having seen above-average net operating income (NOI) and property value appreciation in the past seven to ten years.

It’s the short-term debt taken on during the trough in the interest rate cycle for which property NOI might not be enough to offset higher debt service payments.

The solution: Improve debt-service coverage ratio

Investors who face refinancing challenges in a high-rate environment often resort to extend-and-pretend arrangements to avoid delinquency territory and find long-term solutions. But waiting for financial markets to improve, only to then bring a distressed asset to the negotiation table, can prove unfavorable for lenders.

A more sustainable way to improve your finances is to find new equity partners or mezzanine financing to help bridge funding gaps.

More sustainable still is adopting a proactive approach to refinancing. Before seeking to refinance, consider making partial mortgage payments to improve your loan-to-value ratio (LTV). Improving operational efficiency and property performance can strengthen the debt-service coverage ratio (DSCR), making refinancing easier.

Capitalizing on the maturity wall: Beware of distress sales

On the other hand, a looming maturity wall might look like an opportune moment to buy distressed assets. “ A wall of debt maturities looms over the sector, driven by extend-and-pretend strategies that pushed refinancing into the future,” Graham Austin observes. “Many investors are positioning themselves to capitalize on anticipated distress sales, hoping to acquire assets at reduced prices.”

But the First Vice President of Matthews warns that “This strategy could backfire, as heightened competition for distressed assets may suppress price discounts.” Austin suggests, “Waiting for a wave of distress could prove less lucrative than acting proactively.”

Challenge #5: Property valuation uncertainties

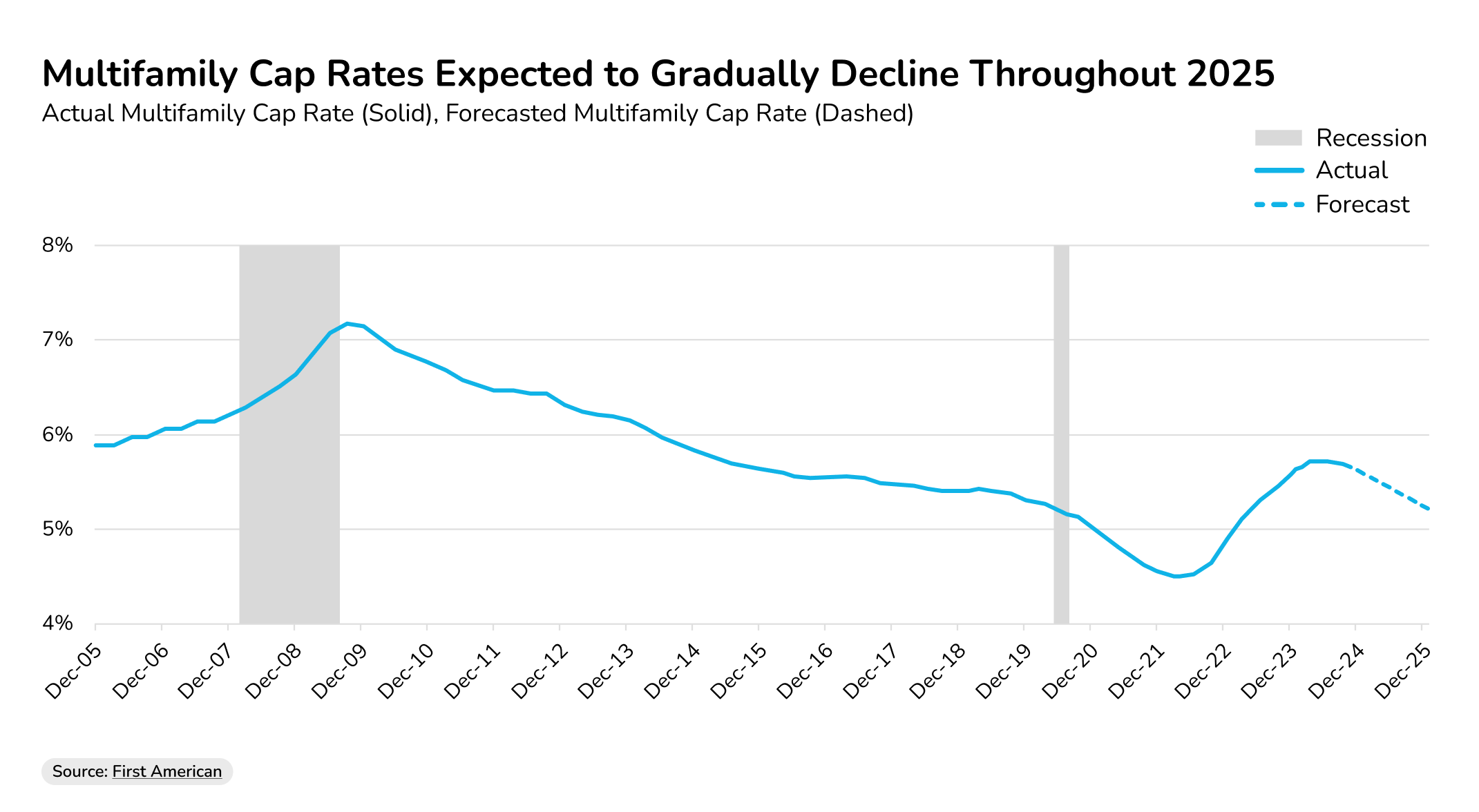

Valuing property accurately is hard in 2025’s turbulent market. Rental rates are forecasted to grow in the next few years, consultancy Callan reports, as is investor demand. Moreover, cap rates are set to decline, First American data suggests.

Source: First American

Not only do shifting cap rates make accurate investment analysis difficult, but they’re also a sign of increasing valuations that are, in turn, a result of strong investor demand. With such market dynamics, it’s easy to overpay for underperforming assets. That’s why accurate property valuation is so important.

The solution: Combining valuation techniques

Understanding the fundamentals of commercial property appraisal is more important than ever – but how to value multifamily property in such a complex market?

Multiple methods of property valuation exist, each with its own strengths and weaknesses. For instance, cost-approach appraisals help price in rising cost constructions, while an income-based valuation can help account for shifting cap rates.

How to evaluate a multi-family investment property? Rather than relying on a single method, you should combine multiple property appraisal methods to find an accurate valuation.

Challenge #6: Tenant quality and retention

Perhaps the hardest challenge when multifamily property investing is managing tenants. Tenant quality is property management companies’ top concern in 2025, according to an industry survey by proptech company Buildium.

That’s understandable when an alarming 93% of property managers and owners reported experiencing rental fraud in 2024, as per an NMHC survey, with falsified proof of income or employment being the most common form.

The problem is aggravated by rising rents outpacing wage growth. "It's a kind of false occupancy – units are being filled by people who can't pay rent in the long term," explains Aaron Victorson, EVP of Sales & Sales Operations at rental broker theGuarantors. "Consumers are maxing out credit cards to rent a place, which could mean operators are sitting on a default bubble."

The solution: better tenant screening and resident experience

Property managers are implementing improved screening procedures to find financially stable residents. "In the past, we could receive a credit report from a bureau, but our teams always had to perform a manual ID verification, paystub verification and employment verification," explains Amy Weissberger, Senior Vice President of Corporate Strategy at Morgan Properties, the nation’s fifth-largest apartment owner. "Many of those pieces are becoming more automated as technology evolves."

By now, the finances of around 30-40% of the screenings that Morgan Properties processes are automatically verified using income verification software.

And while screening can improve incoming tenant quality, it’s equally important to hold on to those tenants. That’s where focusing on the resident experience comes in.

Clear and regular communication is key to both tenant satisfaction and earning their trust. That means keeping tenants informed about maintenance schedules, rent changes, or community updates. It also means engaging with tenants through community events and newsletters that foster a sense of belonging and longer tenancies.

Another retention strategy is to invest in on-site amenities, like a communal lounge, fitness room, or co-work space.

When it comes to multi-family real estate investments, tenant retention not only reduces turnover costs but also creates more predictable cash flow – which is an important factor for a healthy multifamily portfolio.

Why multifamily property investing is a smart move in 2025

Investors who invest in multifamily properties will face some big challenges, but they’re not insurmountable.

Those who successfully navigate hurdles like how to evaluate a multi-family investment property and who can raise money sustainably are looking at a steady return on investment. That’s why multifamily is the most preferred asset class for commercial real estate investors in 2025.

For investors who are ready to take on these challenges and capitalize on multi-family real estate investing, Duckfund offers innovative financing solutions that address the capital constraints that limit many non-institutional investors.

Our earnest money deposit financing enables you to secure properties quickly without tying up your capital, giving you a competitive edge in today's market.

[From bidding on an apartment complex to closing the deal, leverage Duckfund’s equity financing for expertise and liquidity. Get up to $100 million in just five days to help you secure multi-family properties and other CRE assets.]

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next commercial property acquisition — zero upfront capital required.

Start with Duckfund’s EMD financing program.- No capital commitment

- Close faster

- Scale with confidence