Stop Waiting on Banks: 6 Alternative Financing Solutions for CRE Deposits (That Don’t Need Bank Approval)

Today’s commercial real estate deals move at a pace that traditional financing structures can’t match. Sponsors who haven't lined up alternative financing solutions for CRE deposits get outpaced by those who have ready capital.

Even experienced CRE investors hit the same pressure points when deposits are on the line:

- Liquidity timing: Personal equity is often committed elsewhere when a deal surfaces

- Collateral constraints: Traditional lenders ask you to pledge assets on properties you're still deciding whether to buy

- Opportunity cost: Tying up capital in an earnest money deposit freezes the cash you need for the next acquisition

Luckily, there's a full toolkit of alternative financing solutions for CRE deposits without bank approval, credit checks, or collateral requirements. Sponsors already use these funding solutions at the deal level, and it's more accessible than most sponsors realize.

This guide covers six of the most practical lending options, from dedicated EMD lenders and soft deposit financing to seller-negotiated terms and bridge capital, so you can match the right instrument to your timeline and deal structure.

Looking for fast EMD financing to compete on your next CRE acquisition? Contact Duckfund to learn how soft deposit financing can help you capitalize on investment opportunities.

Why traditional bank approval doesn't work at the deposit stage

Traditional bank loans are notoriously hard to access. The Fed’s latest Senior Loan Officer Opinion Survey found that a net share of banks tightened C&I lending standards across firms of all sizes. Smaller institutions reported tighter CRE loan standards on balance, too. And the Fed's 2026 outlook? Standards are expected to remain "basically unchanged" across most loan categories.

But the core issue at the deposit stage isn't even eligibility or higher interest rates. It's in the approval process.

Banks need weeks to months to process a commercial real estate loan from application to approval. Meanwhile, earnest money deposits on commercial transactions are due within days of a signed purchase agreement. Miss that short window, and sellers walk.

Part of why is structural. Bank underwriting requires documentation that doesn't exist at the deposit stage, like appraisals, title work, and environmental clearances. A loan committee can't price risk on an asset that hasn't been evaluated yet. Yet the deposit comes before due diligence concludes, not after.

There's also a lifecycle mismatch. An earnest money deposit runs 30 to 60 days and resolves at closing or when contingencies clear. Bank loans are built for multi-year amortization. These are clearly different instruments built for different problems.

Matt Morgan, a commercial real estate broker with IPA Commercial Real Estate, often points this out when advising his clients in office property acquisitions: "Our consulting often involves guiding clients to explore rapid, short-term financing specifically for earnest money shortfalls. This approach allows sponsors to confidently make offers, securing properties ahead of slower, traditional financing approvals."

So banks are the wrong instrument for this stage of a CRE acquisition. What then are alternative financing solutions for cre deposits without bank approval?

6 Alternative financing options for CRE deposits (without bank approval)

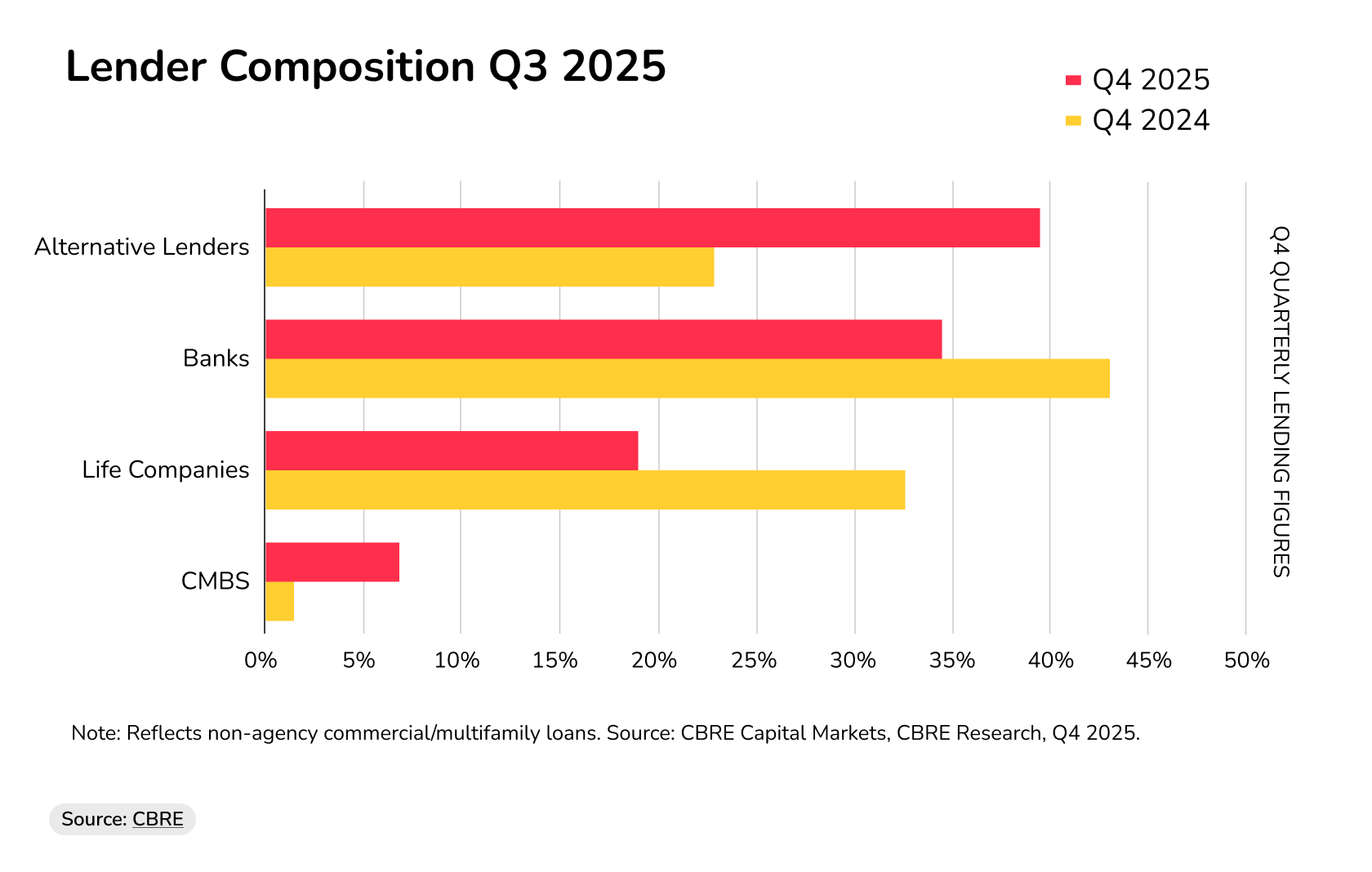

The momentum of non-bank alternative funding options has never been stronger. Alternative lenders held 40% of non-agency CRE loan closings in Q4 2025, up from 23% a year earlier, according to CBRE's Q4 2025 lending momentum report. Debt funds were the biggest driver, jumping 112% year-over-year.

Alternative Lending is Growing While Banks See Less Lending Activity

Source: CBRE

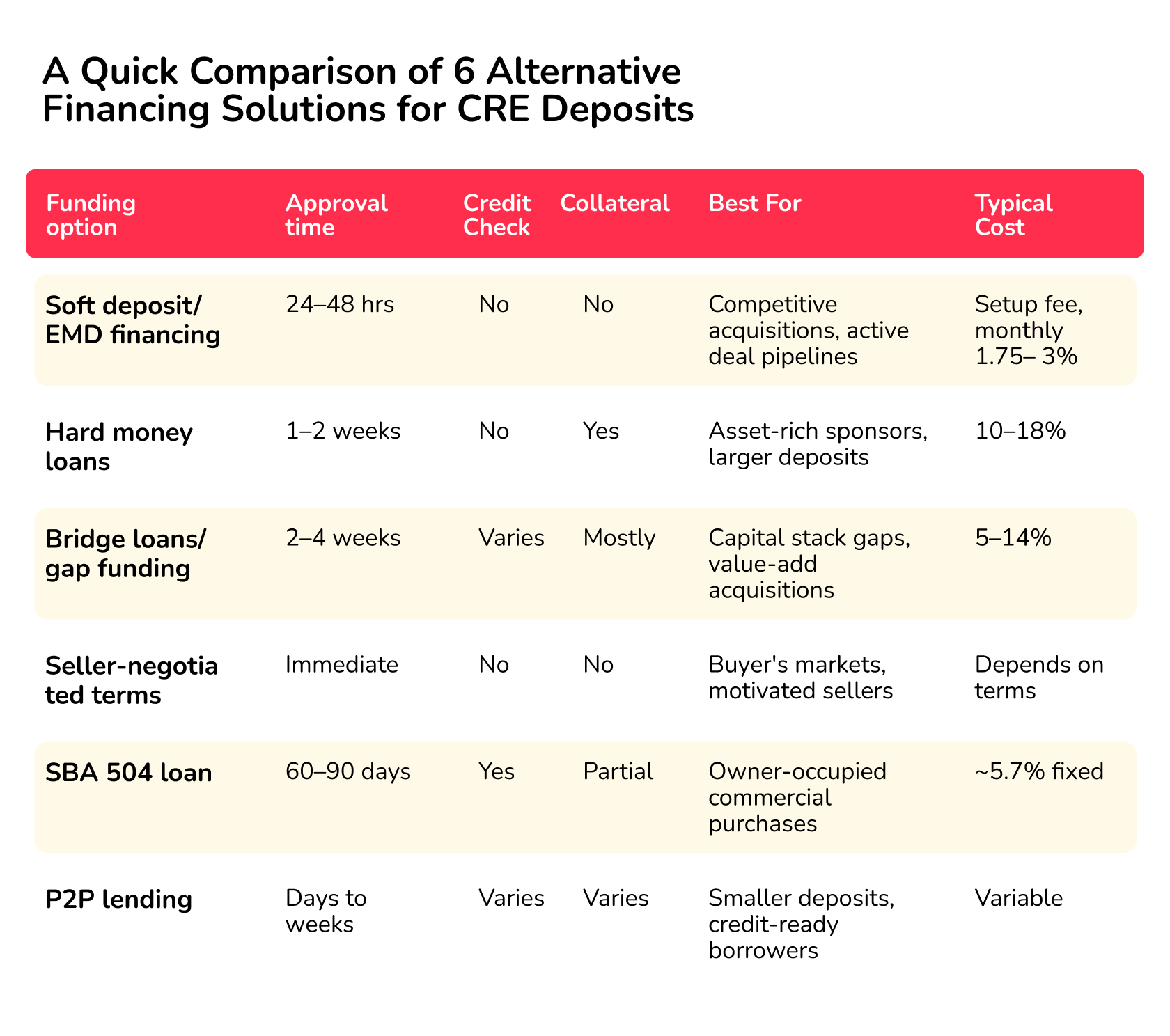

Six of those alternative funding options work specifically at the deposit stage. Before going into each one, here's how they compare in relation to the CRE deposit stage.

Which of these alternative financing solutions for CRE deposits without bank approval suit your deal? That often depends on how fast the deposit needs to move.

Soft deposit financing and seller-negotiated terms are the only realistic options if the window is under a week. Collateral availability matters too: hard money and bridge lenders require it, while soft deposit financing and P2P platforms don't.

Time sensitivity and collateral aside, how to raise capital for CRE depends on your capital allocation. Sponsors who are cash-rich can absorb an earnest money deposit before financing a down payment. Everyone else is better off finding a financing structure that keeps their capital free.

Preston Guyton, founder of real estate platform EZ Home Search, agrees that “The strategic edge of short-term EMD debt is capital allocation discipline.” Guyton sees investors who preserve their capital consistently outperform those who don’t because “they’re capitalizing on momentum”

Each of the six CRE financing options below carries a different cost to your capital stack. Some preserve liquidity entirely, while others ask for a pledge you may not want to make at this stage of a deal.

1. Soft deposit / EMD financing

Soft deposit financing is the one instrument on this list designed for the pre-close deposit stage. A specialist EMD lender funds your earnest money deposit directly to escrow while your equity stays liquid.

Duckfund is one of the few US lenders purpose-built for CRE soft deposit financing. Over 4,000 CRE investors have secured over $1.5 billion in deals through the platform.

How does Duckfund provide EMD funding? Borrowers apply online in under five minutes. Approval arrives in 24 hours and requires no credit check or collateral pledge. Duckfund then wires funds to escrow within 48 hours of approval.

Duckfund only charges a setup fee and a monthly call option premium ranging from 1.75% to 3% of the EMD amount.

Speed and fee structure aren’t the only advantages here. Duckfund allows active sponsors to finance multiple acquisitions simultaneously. That means you can have two or three deals in diligence at the same time without touching your own capital.

2. Hard money loans

Hard money loans are asset-backed, short-term loans funded by private lenders rather than banks. The underwriting centers on the property's value rather than the borrower's strong credit history. That’s why hard money is attractive to investors that don’t meet traditional qualification criteria.

And because it’s private money, approval can come in as little as a week. But faster approvals and flexibility come at a higher cost than traditional funding. Hard money lenders charge interest rates of 10–18%, plus points, legal fees, and appraisals that eat into your margins fast.

Hard money loans are best suited for sponsors looking at a large CRE deposit and who don’t have the creditworthiness traditional financial institutions demand. For soft deposit needs, dedicated EMD lenders like Duckfund offer far better repayment terms.

3. Bridge loans / gap funding

Bridge loans cover a cash flow gap or provide working capital until finances stabilize. For commercial real estate bridge loans, that means funding a portion of the acquisition cost while longer-term financing gets put in place.

Most bridge loan providers require collateral. Rates sit between 5% and 14%, with approval timelines of two to four weeks.

But that’s too slow for most commercial deposit deadlines. Bridge loans are more useful as a complementary instrument: covering the capital stack gap during the acquisition itself while a separate deposit instrument handles the pre-close window. Treat them as phase two, not phase one.

4. Seller-negotiated terms

Not every deposit problem requires a line of credit. Some of the most effective examples of creative financing and real estate entrepreneurship happen before any third-party capital is involved. They happen at the negotiating table.

A motivated seller may agree to a reduced deposit amount, a phased deposit structure, or a delayed deposit date. Any one of these can solve a cash timing problem without a lender, a fee, or a credit process.

Market conditions make this work: you need leverage. Seller-negotiated terms are most available in a buyer’s market when inventory is elevated, when a seller is under time pressure, or when you're dealing directly without a broker as a gatekeeper on negotiation terms.

For investors building a practice around seller financing in commercial real estate, structuring deposits as part of a broader financing arrangement is worth developing. But in a competitive multiple-offer situation, asking for a reduced deposit may just cost you the deal.

5. SBA 504 loan

The SBA 504 is one of the cheaper long-term financing options available. Current rates run 5.62%–5.99% depending on term length. That's a compelling cost of capital.

But there’s a catch: these SBA loans finance owner-occupied commercial properties only.

The SBA 504 funds the acquisition, typically financing 50% of the project cost with a conventional mortgage structure, an SBA debenture covering 40%, and 10% personal equity. The application process takes 60–90 days minimum and requires a full credit review, partial collateral, and detailed financial documentation.

The SBA 504 belongs in the acquisition financing conversation. It’s not a soft deposit tool. If you want to post a deal-winning EMD, use a dedicated soft deposit instrument while the SBA process runs in parallel.

6. Peer-to-peer lending

Peer-to-peer (P2P) connects borrowers directly with individual investors or capital pools through fintech platforms, bypassing traditional bank intermediaries. Originally built for consumer, startups, and small business loans, P2P lending platforms are now shaking up the CRE capital market — giving sponsors an additional path to capital outside the conventional lending stack.

Peer-to-peer lending works best when you have time and a strong business plan. Approval speed varies considerably by platform and project, from a few days to weeks or even months. That’s why it's not the right tool for a deposit deadline.

Rates vary by platform and depend on credit scores. For sponsors running smaller acquisitions with healthy credit profiles, though, it can offer a lower-cost path to financing.

The bottom line on alternative financing for CRE deposits

CRE professionals no longer operate under a bank-or-nothing model. With the alternative lending infrastructure growing, the alternative funding options on this list are what active sponsors are using to keep their pipelines moving.

The right alternative financing solution for CRE deposits without bank approval comes down to how fast the deposit needs to move, whether you have collateral to pledge, and what locking up that capital for 60 days costs your pipeline. For active sponsors competing on multiple deals at once, soft deposit financing answers all three.

Your next deal won’t wait. Apply for EMD financing with Duckfund and get your deposit with 48-hour approval, zero upfront capital, and discounted rates starting month four.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence