5 Alternatives to Commercial Real Estate Hard Money Lenders

It starts with a phone call and ends with a rate that makes you wince.

If you’ve ever dealt with commercial real estate hard money lenders, you know the pitch: “We can fund this by Friday.”

What they often don’t mention is the high interest, the upfront fees, and the pressure to flip or refinance before the ink is even dry.

CRE investors keep going back to hard money lenders for one reason: speed. Yet that speed often comes with serious trade-offs, including:

- Interest rates of 10–18% – plus points, legal fees, and appraisals that eat into your margins fast.

- A short fuse – most hard money commercial real estate loans come with 6–12 month terms, which is great if your exit plan is flawless, risky if it isn’t.

- Little flexibility – you might be experienced, but if the asset isn’t perfect, your lender’s terms won’t be either.

Thankfully, there’s a market of funding sources designed to steer you away from these problems and make your next commercial property deal a success.

This guide lays out five solid alternatives to commercial real estate hard money lenders, without handing over leverage to a lender who only sees the property, not the plan.

Table of contents:

- Why CRE investors use hard money lending

- The downsides of hard money loans for commercial real estate

- The top 5 alternatives to commercial real estate hard money loans

- A smarter way to fund your CRE deals

Looking for an alternative to hard money lending? Contact Duckfund to find out how we can help you land your deal before your rivals.

Why CRE investors use hard money lending

Anyone who’s worked in commercial real estate knows that speed matters.

Traditional bank loans move too slowly for deals where timing makes or breaks the opportunity. That’s where commercial real estate hard money lenders come in.

Their main selling point? Fast funding with fewer hoops.

If you need to close in five days, then a hard money loan for commercial real estate can make that happen. Hard money lenders primarily underwrite them on asset value, not the borrower’s credit score or business history, so they become attractive to investors with complex financials or past credit hiccups. That kind of leniency isn’t something you’ll find with traditional financing.

Bridge loans are another big driver. For investors flipping a mixed-use or multifamily CRE property – or waiting on a cash-out refinance to clear – hard money offers a temporary solution when conventional lenders say no.

There’s also flexibility. Need to finance a niche property type or a deal with a low loan-to-vale (LTV)? Private lenders often have more room to maneuver than banks, especially when it comes to non-owner-occupied properties.

But all that flexibility comes with several downsides, which is where many CRE investors start to feel the squeeze.

The downsides of hard money loans for commercial real estate

For all their speed and flexibility, hard money commercial real estate loans often create just as many problems as they solve, especially for long-term investors or those trying to scale.

“Though hard money loans work well for some borrowers, they’re also called “loans of last resort” for a reason – they tend to be risky”, says Robin Rothstein, senior staff writer at Forbes Advisor.

Let’s take a closer look at some of these risk issues.

- High interest rates

Many commercial hard money loans come with double-digit rates: often 10% to 20% or more. Then add origination fees, appraisals, and upfront costs that can total 3 to 5% of the loan amount.

These aren’t structured like your average bank loans: they’re priced like a stopgap, not a sustainable strategy.

- Liquidity

Hard money lenders don’t cover earnest money or deposits, so even before funding kicks in, you’re forced to front tens or hundreds of thousands in cash just to hold the deal.

That can block you from pursuing other investment opportunities, or worse, leave you scrambling if a better asset hits the market days later.

- Loan terms

Most commercial hard money lenders expect repayment in 6 to 18 months, which puts pressure on your project’s timeline and leaves little room for delays in renovations, refinancing, or finding a buyer.

Miss the window, and you’re staring down foreclosure or forced liquidation.

Scalability

As your real estate investment portfolio grows, stacking short-term, high-cost property loans becomes harder to manage. You end up working on just one deal at a time because your repayment costs are too high, and this puts the brakes on portfolio growth.

The key is to find better financing options out there that are flexible and affordable enough for you to spin several plates at once.

Bottom line: Commercial real estate hard money lenders might solve a short-term problem, but they can easily become a long-term liability.

The top 5 alternatives to commercial real estate hard money loans

The current alternative lending market is flush with useful options that provide a solid alternative to hard money loans.

Here’s a look at five of the most popular right now.

1. Soft deposit lending

Soft deposit lending helps real estate investors secure deals without draining liquidity.

Rather than tying up large sums in a down payment, soft deposit funding provides just enough capital to lock in your contract and move fast, especially useful for competitive bids or off-market deals.

Unlike hard money loans, these don’t saddle you with high interest rates or interest-only payments. Instead, you’re getting short-term funding purely for deposits, so your capital is kept free for loan programs on other deals.

Duckfund, for example, is a digital lending platform that offers affordable soft deposit financing within 48 hours, without the need for a perfect credit history, so you can bid on multiple investment properties without tying up your working capital.

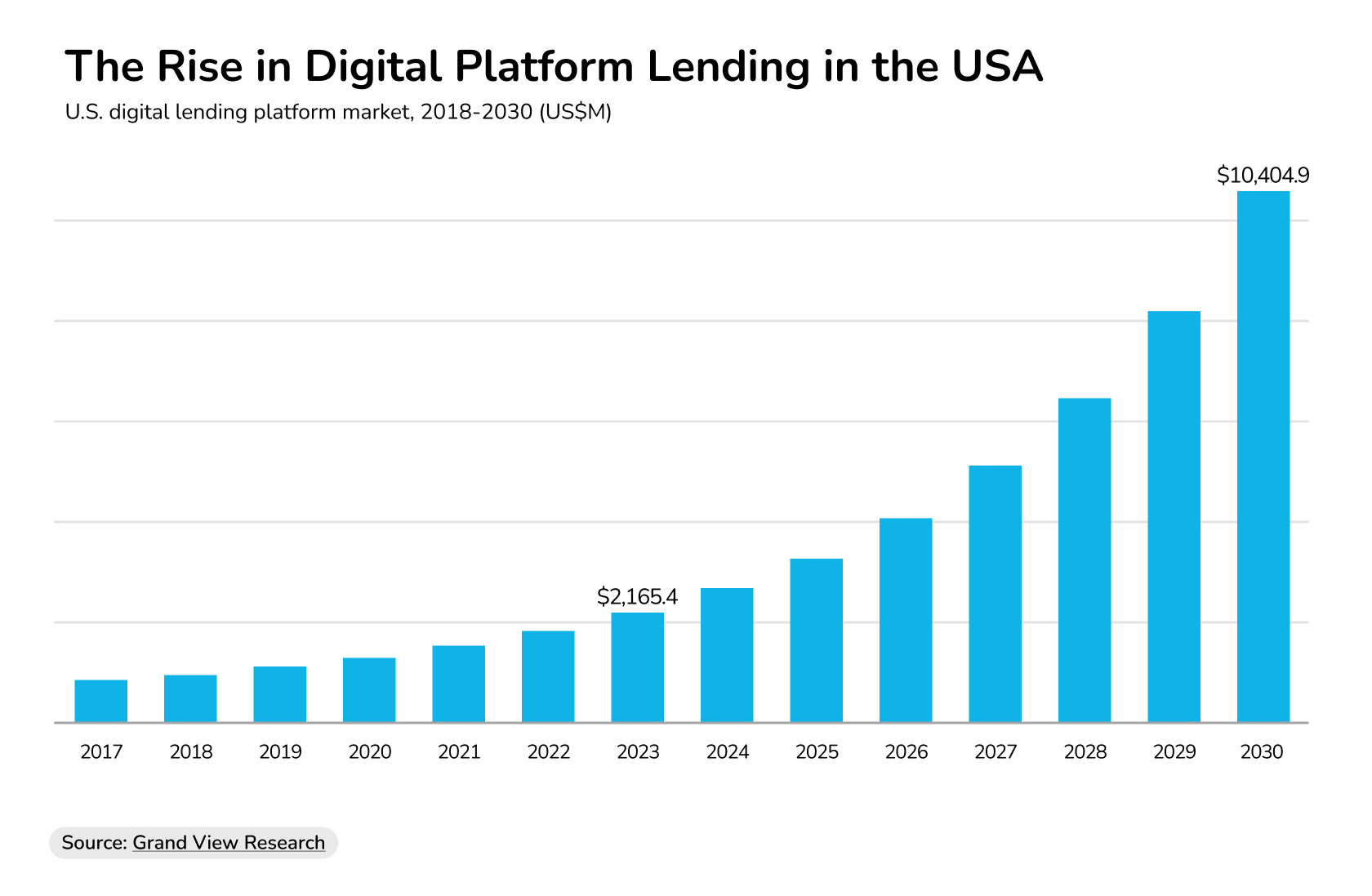

This type of lending is becoming more popular with borrowers seeking a secure alternative to traditional finance. A recent research report has digital platform lending increasing by almost 500% between 2023 and 2030.

The Rise in Digital Platform Lending in the USA

Source: Grand View Research

For borrowers in fast-moving markets, this is a more agile tool than traditional loans and a great alternative to relying solely on private money loans or risky bridge loans.

2. Transactional funding (double closings)

Transactional funding supports real estate investors fixing and flipping CRE or wholesale deals.

It’s typically used for double closings, when you briefly take ownership before reselling — all within 24 hours. This type of loan is short-term, low-risk, and requires no down payment or credit check.

Transactional funding only charges a flat fee or small percentage of the loan amount, and there’s no long-term liability. This is in stark contrast to hard money lending, which often includes high upfront fees and double-digit interest rates.

Yet timing is everything: you must have an end buyer lined up and paperwork ready.

Lenders like EMD Transactional Funding and Get Funds 4 Real Estate specialize in these quick-flip loans.

These all offer same-day funding, minimal underwriting, and support with assignment contracts – perfect for experienced wholesalers looking to close fast and keep cash flow moving.

For rental property or owner-occupied strategies, transactional funding won’t work. But if you’re flipping contracts with strong buyer demand, it beats the cost and friction of a full private money loan.

3. Earnest Money Deposit (EMD) Funders

Many traditional lenders won’t cover earnest money, leaving investors scrambling to secure funds just to hold a deal. That’s where earnest money deposit providers step in. These lenders provide capital specifically for your contract deposit, typically 1% to 3% of the value of the property.

For real estate investors handling multiple deals, tying up capital in EMDs kills momentum. EMD funding helps you stay liquid without tapping a cash-out refinance, bridge loan, or risky short-term loan.

Plus, the underwriting is deal-based and is not dependent on your credit score or the borrower’s credit.

Top providers include Duckfund, with its coverage of all CRE sectors, as well as EMDDC and Y2 Lending.

These all offer flexible terms and fast closings, especially in competitive markets where delays can mean losing a deal.

EMD funding can help you stay nimble without sacrificing deal flow or risking foreclosure from missed deposits.

4. Gator lending and contract-based underwriting

Gator lending uses your contract (not your credit history) to qualify you for funding.

These short-term loans are ideal for fix and flip deals or wholesale contracts where you’ve got a buyer lined up but need capital to secure the deal.

Gator loans are underwritten based on deal structure, the value of the property, and the exit strategy, instead of relying on the borrower’s credit.

You’ll often get proof of funds, support with underwriting, and quick-turn capital that’s easier to manage than a private money loan or long-term refinance risk.

Gator lenders like Axelrad Capital, Mum City Properties, and Gator Lending Portal offer funding with minimal red tape.

Compared to private money lenders charging high interest-only payments and rigid terms, Gator loans offer speed and flexibility, especially for small businesses or new investors who can’t yet qualify for a conventional loan.

5. Joint Venture (JV) capital, equity partners, and tax-advantaged strategies

If you’re scaling or working on large mixed-use or multifamily projects, JV capital and equity partnerships might offer more long-term flexibility than short-term debt.

Here you share equity with a capital partner and align your incentives for long-term growth – a much better option than paying high interest rates to a private lender.

This model is especially valuable for investors managing multiple rental properties or owner-occupied commercial projects. It removes the pressure of short-term loans and sidesteps the trap of serial cash-out refinances or stacking bridge loans.

JV structures and equity partnerships can also facilitate 1031 exchanges, a powerful tax-deferral strategy for real estate investors.

Investors can defer capital gains taxes when swapping like-kind properties by using 1031 exchanges in combination with JV capital. This is a recognized tactic toward more strategic portfolio growth without losing liquidity to tax payments.

Joint Venture Loans and Maharaja Enterprises are two groups offering equity-based capital, usually for investors with proven track records. Others, like Truss, help structure deals and bring partners to the table.

Yes, you’ll give up some upside, but you’ll also avoid the rigidity, fees, and refinancing risks that come with traditional debt.

For the right deals, JV funding combined with smart tax strategies (like 1031) can be a better long-term play than relying on stacked hard money loans.

A smarter way to fund your CRE deals

Hard money loans may get you funding fast, but their high rates, tight timelines, and rigid terms can quickly eat into your profits and stall your growth.

The good news? There are better options out there.

From soft deposit lending that frees up your cash, to transactional funding for quick flips, and earnest money deposit funders that cover upfront costs – these alternatives help you move fast without the usual headaches.

At Duckfund, we focus on EMD financing to keep your cash flowing and help you lock in deals without draining your reserves.

Ready to ditch the hard money trap and fund smarter? Connect with us to see how simple securing your deals can be.

Want to make your next deal move faster? Sign up for Duckfund, and we’ll help you grow your portfolio faster.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence