EMD Finance: Your Capital Is Too Valuable to Sit in Escrow (The CRE Investor's Guide)

Here’s a scenario every active CRE investor recognizes in some way. You've done the underwriting: the asset pencils. Your broker is telling you there are two other Letters of Intent on the table and the seller wants deposits by Thursday.

You have the equity – but it’s tied up in a renovation draw, a reserve account, a parallel acquisition you're still in diligence on. So you either move slowly or you move thin. Most of the time, you move thin. And sometimes that costs you more than the deal.

Even experienced investors struggle with the following when it comes to EMD:

- Liquidity timing. Personal equity is often committed elsewhere when the right deal surfaces.

- PSA contingency language. Misunderstood non-refundability triggers in commercial purchase agreements are how deposits get lost.

- Opportunity cost. Tying up $150K–$400K is money that can’t be put towards TI, the leasing commissions, or the next deal.

EMD finance addresses all three. Yet it’s an underused tool in the CRE capital toolkit.

This guide is written for operators who might know what an earnest money deposit is but who want to unlock its full potential in CRE deals.

What you may not have fully mapped out is how EMD financing fits into your capital stack, how the contractual mechanics around deposit hardening actually work in commercial PSAs, and where the real risk of deposit forfeiture lives — which is seldom where investors expect it.

What follows is a practical breakdown of how EMD finance works and the strategies experienced operators use to turn deposit financing into a real competitive edge.

Looking for fast EMD financing to compete on your next CRE acquisition? Contact Duckfund to learn how soft deposit financing can fit your capital strategy.

What is EMD in real estate? Earnest money deposits explained

An earnest money deposit — referred to throughout the industry as an EMD — is a good-faith payment wired by the buyer into a neutral escrow account upon execution of a purchase and sale agreement (PSA).

An EMD is not a down payment; it doesn't go directly to the seller. Instead, it sits in third-party escrow while the buyer conducts due diligence, secures financing, and works toward closing. Only then does it get applied toward the purchase price.

The distinction between an EMD and a down payment sometimes confuses operators who come to CRE from a residential background. Why? Because where a down payment is a closing-day instrument, earnest money in commercial real estate is a pre-closing commitment device. Its entire function is to signal to the seller: the buyer is serious, underwritten, and prepared to perform.

Pull out of the deal without a qualifying contingency, and in most cases, that deposit doesn't come back.

Research by Duckfund into EMD norms across the US found that the national average sits between 1% and 5% of the purchase price, with competitive or high-value assets regularly requiring 10% or even higher.

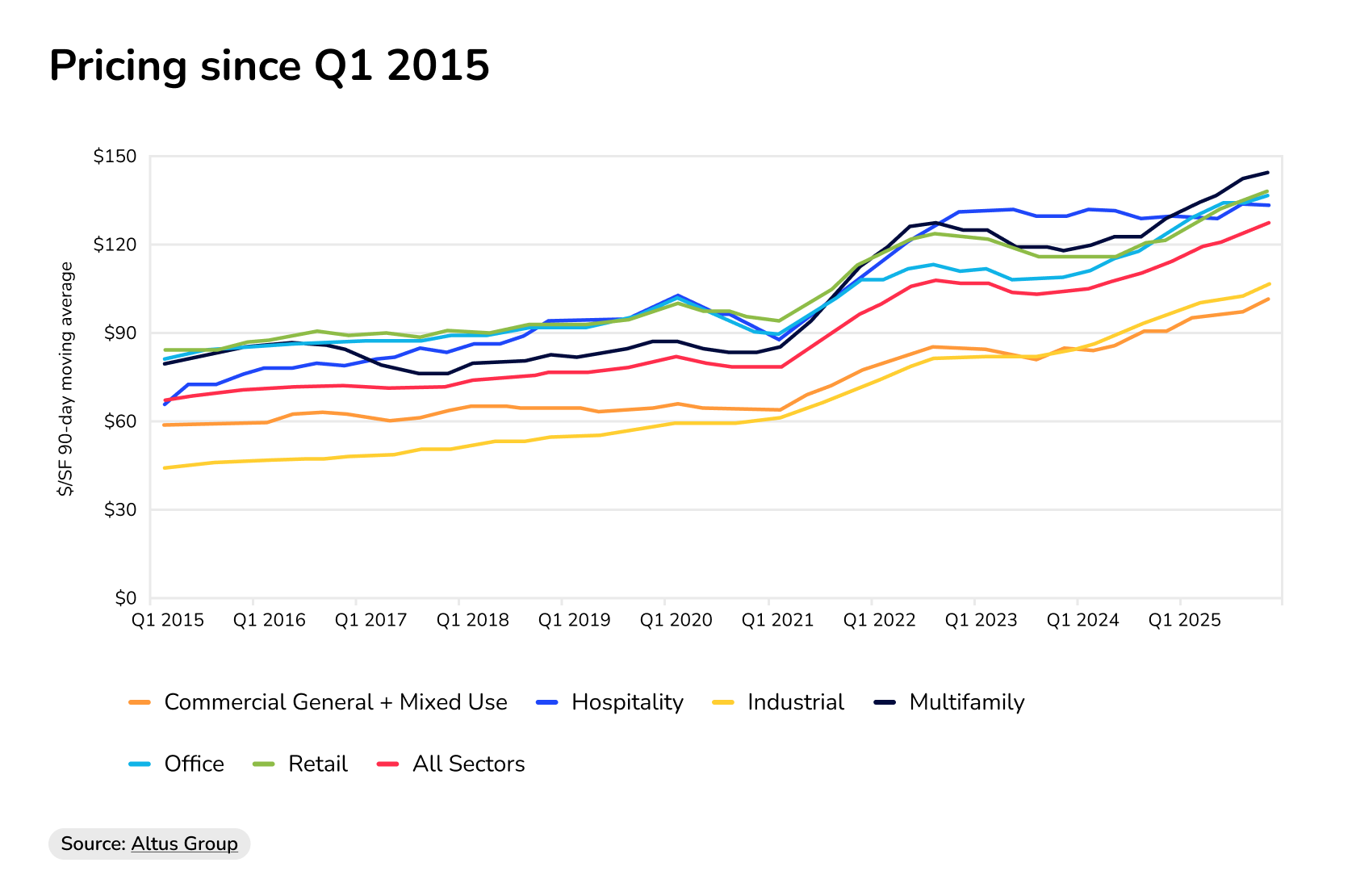

That range is widening as deal competition heats back up. U.S. commercial property sales reached 560.23 billion USD in 2025 – a 14.4% year-over-year increase – and the first rise in transaction count since 2021, according to data from CRE intelligence provider Altus Group.

Median pricing has been steadily rising too, increasing 12.1% Y-o-Y across all property types – putting further pressure on capital investors’ capital requirements.

Median pricing per square foot across CRE asset classes in the US market since 2015

Source: Altus Group

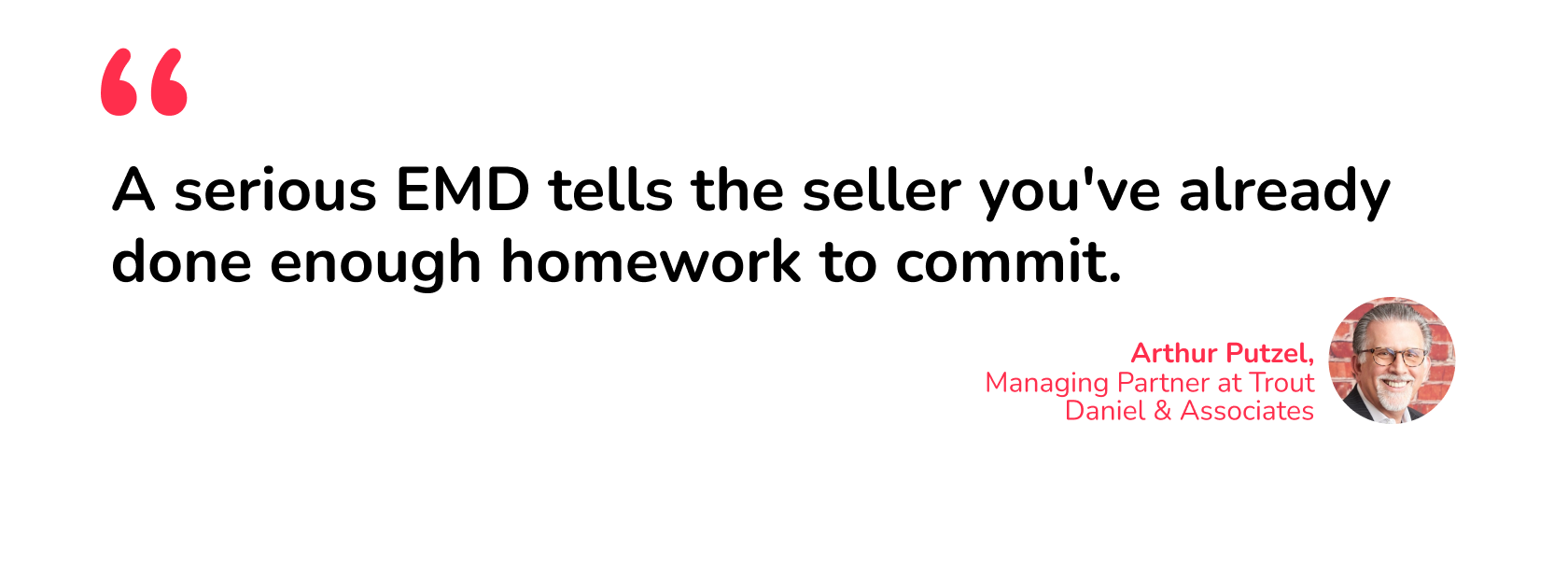

More capital chasing quality assets at higher prices means sellers can afford to be selective — not just on price, but on the quality of the deposit itself. Arthur Putzel, Managing Partner at Trout Daniel & Associates and a licensed CRE broker, has seen this pattern repeatedly at the negotiating table: "EMD financing fundamentally shifts how sellers read your offer. In competitive acquisitions, I've watched sellers choose a buyer posting a larger, faster deposit over a higher headline price — because the deposit signals conviction.”

Putzel further elaborates that “A serious EMD tells the seller you've already done enough homework to commit, which compresses negotiation friction on both sides."

That's the strategic dimension of earnest money. What EMD means in real estate at the transactional level signals goes beyond good faith. Locking capital in escrow under clear terms signals certainty of closure in a market where sellers increasingly treat deposit size and speed as a proxy for buyer quality.

But here’s what it also means: if your EMD capacity is limited by available liquidity, you're already at a structural disadvantage before the first bid is submitted. That's the core problem EMD finance is designed to fix as a financial service.

Now that you know what an EMD is, the more operationally useful question is: how does EMD financing work? And importantly, what happens when your equity is doing something else when you need it?

How does EMD finance work?

EMD finance is a short-term capital instrument where a specialist lender funds your earnest money deposit directly into escrow on your behalf, while your own equity stays liquid.

Earnest money deposit sits entirely outside your permanent financing structure, resolves before senior debt is even drawn, and carries no LTV implication on the acquisition itself.

The mechanics of this type of financing are straightforward. With Duckfund, the process runs as follows: the investor submits an application (a two-minute digital process); approval comes within 24 hours; the deposit is wired directly to the title company or closing attorney's escrow account within 48 hours.

Duckfund then registers an LLC that signs the PSA on the investor's behalf. This in itself is a structure that adds a layer of contractual protection for both parties. The deposit sits in escrow through due diligence. At closing, the investor repays Duckfund from proceeds. If the deal exits within the contingency period, the deposit is refunded and the LLC is dissolved.

Duckfund's minimum deposit is $25,000, with no maximum and no collateral required.

The cost structure is worth understanding precisely, because it's where EMD debt differs from most short-term CRE financing with high interest rates (and high credit risk).

Duckfund charges a monthly fee calculated on the EMD amount, not on the valuation or purchase price. Duckfund's fees are structured as LP soft costs, passed through at closing — with competitive rates that decrease for larger deposits.

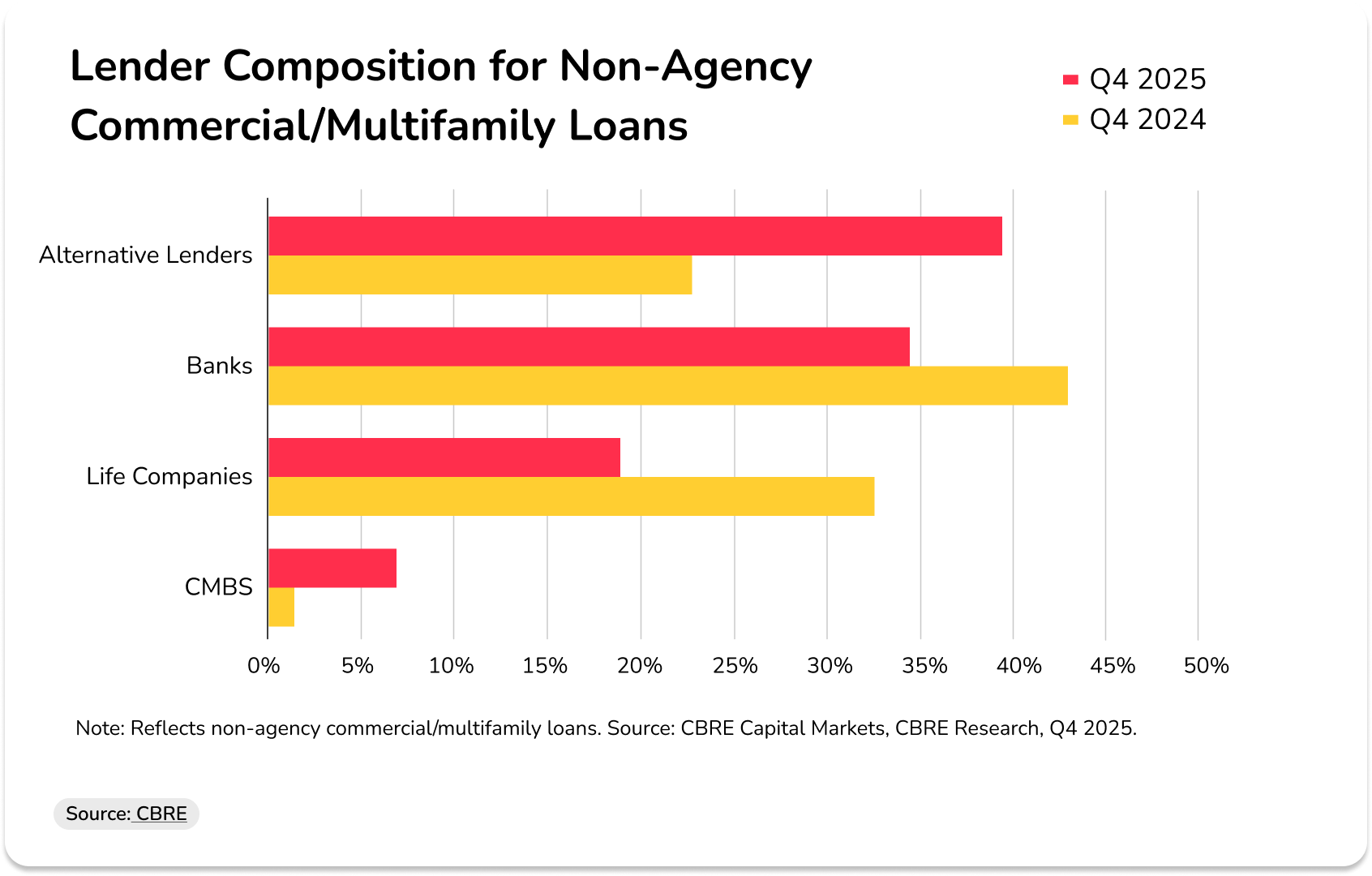

Duckfund's pricing model is structured to reflect the actual capital at risk. That structural clarity also extends to the broader capital market context. By Q4 2025, alternative lenders – including debt funds and mortgage REITs — claimed 40% of non-agency CRE loan volume, up from 23% the prior year, according to CBRE data.

Debt fund volumes alone rose 112% year-over-year. The market is pricing speed and flexibility at a premium, and EMD lenders occupy a specific, high-utility corner of that shift.

Change in lender composition for CRE loans in the US between Q4 2024-2025

Source: CBRE

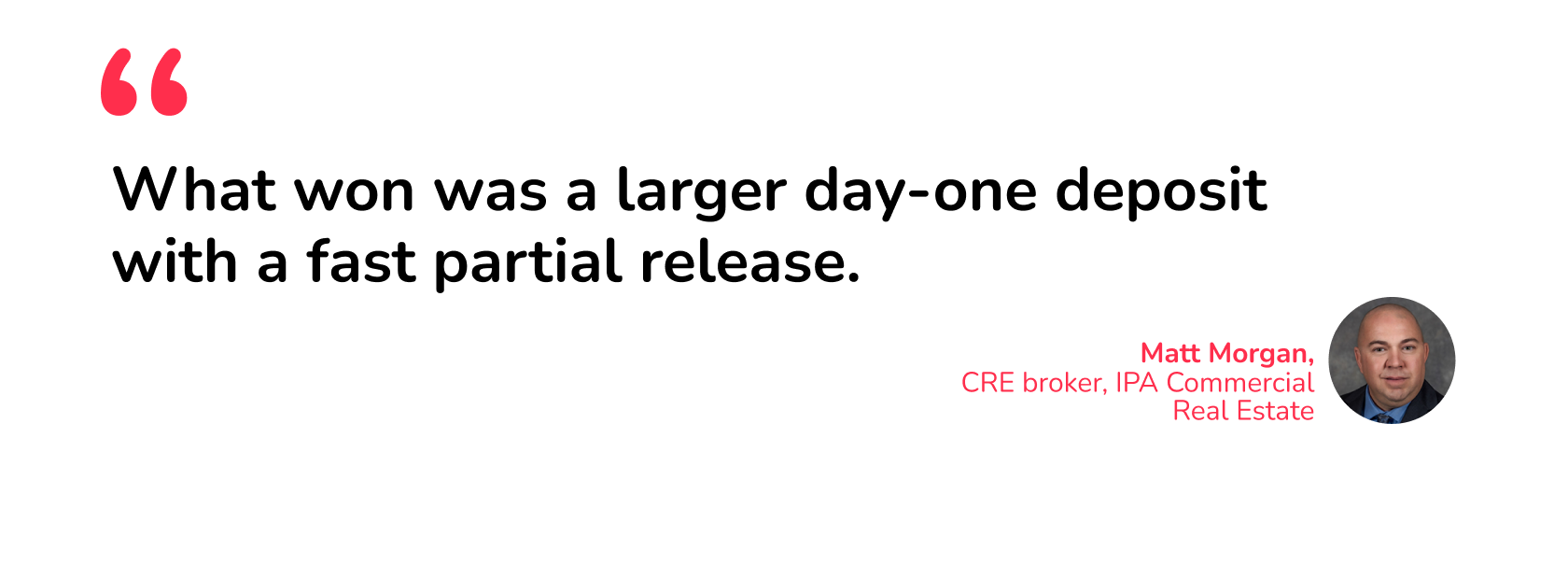

Matt Morgan, a commercial real estate broker at IPA Commercial Real Estate with nearly two decades of active transaction experience, has seen the practical edge this creates play out at the deal level: "EMD financing lets a buyer write a cleaner offer without draining operating cash, and sellers notice the release schedule more than the headline deposit.”

Morgan illustrates his point: “In one Inland Empire retail deal, the winning buyer wasn't the highest price — what won was a larger day-one deposit with a fast partial release at the end of due diligence, because it signaled certainty of close while keeping their equity available for TI/CapEx and leasing moves immediately after close."

That last point matters more than it might seem. The equity preserved by EMD financing is execution capital. Tenant improvement allowances, leasing commissions, early capex – these are the costs that hit between contract execution and stabilization, and they're exactly what gets squeezed when an investor has over-deployed equity into deposits.

The investors who treat EMD debt as a last resort are solving for the wrong constraint. The constraint isn't the deposit fee. It's the equity that's unavailable for value creation after the key is turned.

What is EMD debt?

EMD debt is the short-term liability created when an investor borrows capital to fund an earnest money deposit. That might sound self-evident (and we’ve already discussed this briefly) but it’s worth dissecting the implications for how it sits within your capital structure..

Start with where EMD debt sits in the capital stack. It's pre-senior. It exists before your acquisition financing is drawn, before any LTV or DSCR covenant attaches, and before the permanent capital structure of the deal is even set. By the time your senior lender wires proceeds at closing, EMD debt has already been repaid.

That means it doesn't compete with your senior loan, doesn't affect your leverage ratios, and doesn't trigger any existing covenant restrictions on new debt. In that sense, it's genuinely outside the conventional stack. EMD finance thus becomes a capital timing tool, not a structural financing layer.

This is where EMD debt differs most sharply from the instruments investors typically reach for under liquidity pressure.

A bridge loan carries LTV constraints, title requirements, and appraisal timelines. Mezzanine financing attaches covenants that limit your operational flexibility post-close. Hard money comes with origination fees, higher rates, and often personal guarantees.

EMD debt carries none of these structural burdens because it resolves before any of them become relevant. It's self-liquidating: at closing, proceeds repay the lender; on a clean exit during the contingency window, the deposit refund retires the obligation. The deal either closes or it doesn't — either way, the EMD lender is out.

One important clarification for investors running alternative CRE financing structures: EMD debt's treatment as a pre-close obligation means it typically doesn't appear on balance sheet in the same way long-term leverage does — but it does represent a real contingent liability until the deal closes or exits.

Structure it cleanly, document the escrow arrangement properly, and make sure your senior lender is aware of it. Surprises at closing are how otherwise clean transactions get complicated.

Is earnest money refundable?

Short answer: yes — but only under conditions that are entirely a function of what was negotiated before you signed the PSA. Get those conditions wrong, and the answer flips.

This is one area where CRE diverges sharply from residential real estate, and where investors who haven't run many commercial transactions get hurt. In residential deals, buyer-protective contingencies are often standardized, sometimes even statutory.

In CRE, almost nothing is standardized. Refundability is a drafting question, not a default right, and every contingency that protects your deposit has to be explicitly written into the purchase and sale agreement before you execute it.

The core mechanics work like this. Your EMD is refundable during the due diligence period — sometimes called the inspection period or feasibility window — which is typically negotiated between 30 and 60 days in commercial transactions, though this varies significantly by asset type and deal size. The deposit is generally refundable throughout this window. After it closes, the deposit "goes hard" — converting to non-refundable — unless specific contingencies are still outstanding.

Those contingencies are where the real work is. The main categories in a well-drafted commercial PSA are:

- Inspection and due diligence: Buyer right to terminate for any reason (or for specified reasons) within the DD period

- Financing contingency: Refund right if financing cannot be secured — less standard in CRE than residential, and often negotiated out in competitive situations

- Title review: Right to terminate on unresolvable title defects or missing endorsements

- Third-party deliverables: Receipt of tenant estoppels, SNDAs, environmental clearances, and municipal sign-offs — each of which can take longer than the DD window allows

That last category is where experienced investors most often get caught. A 30-day due diligence window is rarely enough for Phase II environmental reviews, detailed tenant credit analysis, and structural engineering assessments on assets above $5M.

Yet many commercial PSAs default to that window precisely because it's what sellers push for in competitive markets.

The result is a time trap. The buyer's deposit goes hard on a calendar date, but the documents that would justify walking away — a clean Phase I or Phase II, full estoppel package, title endorsements — haven't arrived yet.

Michael Weiss, a partner at law firm Lerner & Weiss APC in Los Angeles who has handled CRE transactions and litigation since 1983, has seen this sequence play out more than once on the deals that end up in arbitration: "The contract language around what triggers non-refundability is where most buyers get exposed. Vague milestones, poorly defined contingency periods, and boilerplate 'as-is' clauses can silently accelerate your hard-money date.”

Weiss’s investment advice is “Getting a transactional attorney involved before you sign, not after you're already in escrow, is the difference between a negotiable position and a check you can't get back."

Negotiating on clear terms before the PSA is executed is an easily overlooked step, as buyers are too focused on winning the deal to push back on the terms.

Yet getting the terms right is crucial, because when a lender funds your deposit and that deposit goes non-refundable due to PSA language you didn't negotiate carefully, you lose the EMD payment plus the EMD financing fee on top of it.

That’s why you shouldn’t just use EMD debt to paper over a due diligence gap. Only borrow for deposits on deals where you've built adequate contingency protection into the PSA first.

4 smart EMD finance strategies for CRE operators

Four EMD finance strategies are worth walking through in detail. Each addresses a specific operational constraint that active investors run into repeatedly in the current market.

- Capital stack preservation

As discussed, capital stack preservation is EMD finance’s core use case. Deploying equity into the deposit means the asset is under contract, but you're already behind on execution capital before diligence even starts.

EMD debt solves the timing mismatch cleanly. The deposit is funded, the deal is controlled, and your equity stays available for what happens after closing.

Jack Donahue, SIOR, founder and president of Donahue Real Estate Advisors with over 30 years on the CRE transactional side, has watched this play out across market cycles and warns that "Your equity is a finite competitive weapon.”

Donahue watched well-capitalized buyers unnecessarily tie up capital in deposits across two simultaneous acquisitions, leaving nothing for TI negotiations or closing costs. He argues that “Debt preserves optionality — and in CRE, optionality wins deals."

- Competitive bid positioning

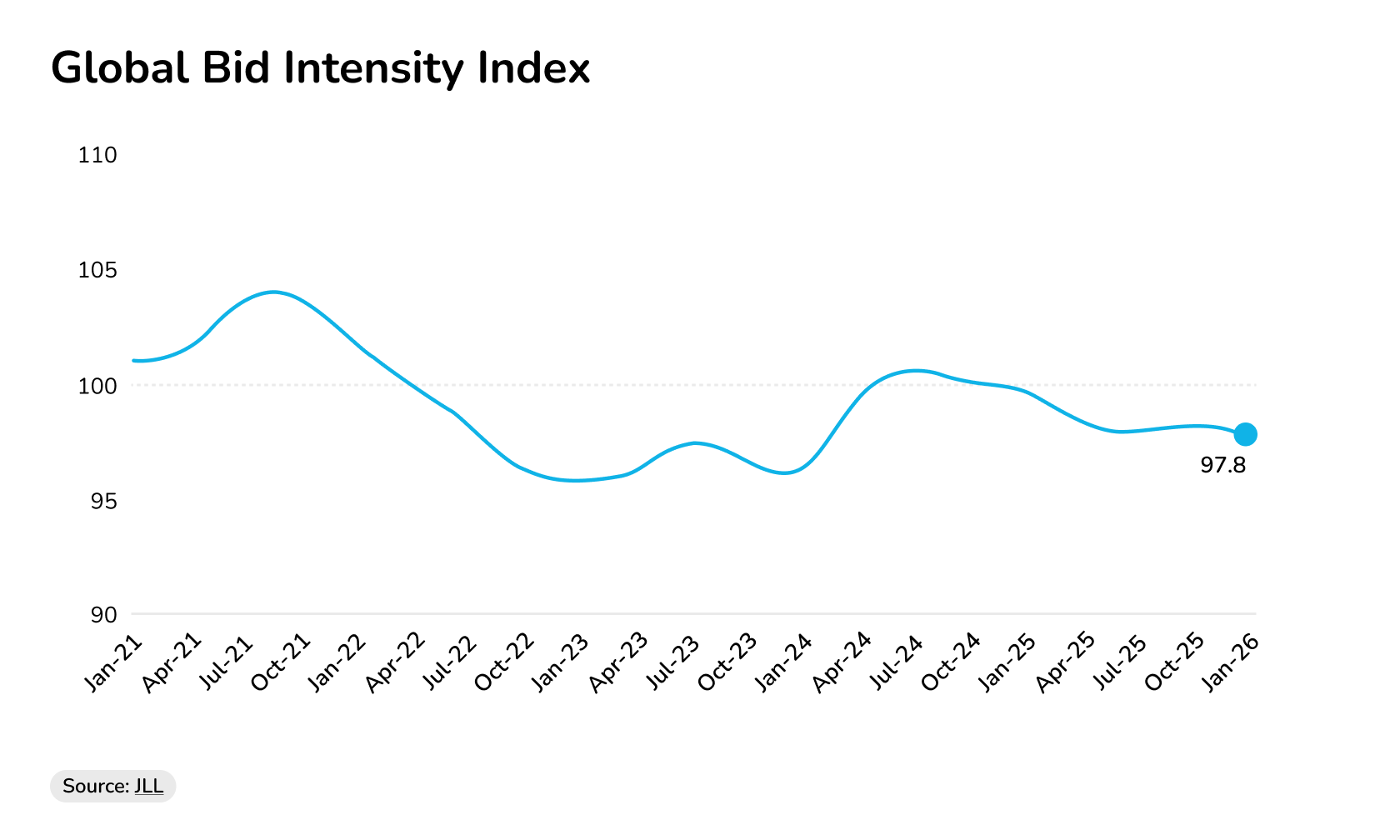

JLL's proprietary Global Bid Intensity Index — which tracks bidder competitiveness across private CRE markets globally — showed consistent improvement through the second half of 2025 across industrial, retail, and office sectors, driven by returning institutional capital and growing bidder pools.

As of March 2026, JLL's index shows bidding competitiveness across the four main property sectors at its narrowest spread in over three years. More competing offers per asset is now the baseline, not the exception.

Investment bidding intensity is consistent even as CRE transaction volume continues to rise

Source: JLL

In such an investment environment, how you show up at the offer stage matters as much as what you offer.

A funded EMD – wired quickly, structured with a clear release schedule – communicates to sellers something a higher number on a page doesn't: certainty of close. Donahue has seen larger deposits win over higher bid prices on exactly this basis: "That larger deposit signals serious intent to a seller and has directly moved my clients to the front of the pack when multiple offers land simultaneously."

- Portfolio scaling

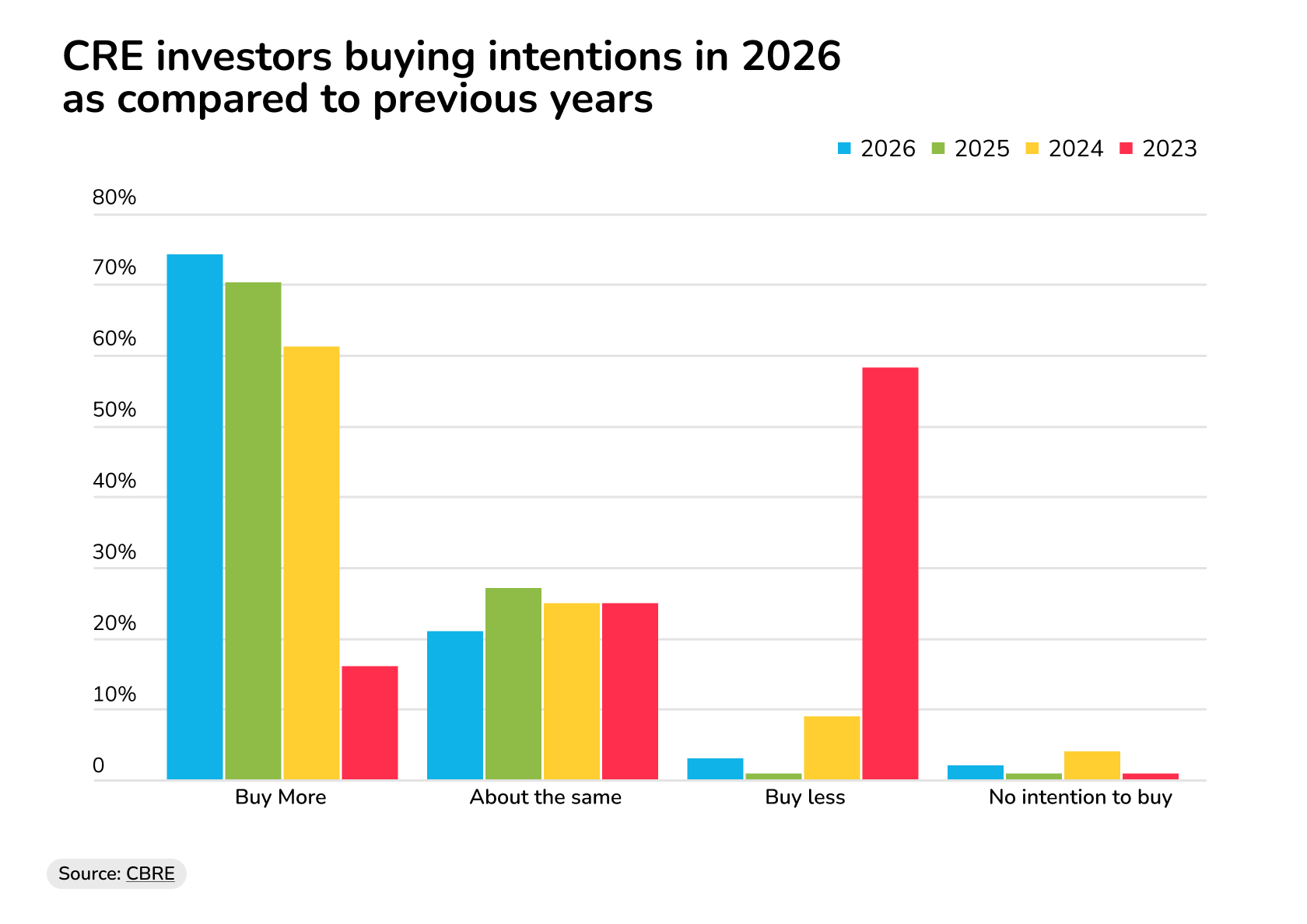

With stabilizing interest rates and a potential decrease in debt costs, around 74% of CR investors are planning to increase acquisitions in 2026, a survey from CBRE found. The constraint for most of them isn't deal flow or underwriting capacity. It's capital availability at the front end of multiple simultaneous transactions.

CRE investors buying intentions in 2026 as compared to previous years

Source: CBRE

When you fund deposits from personal equity, each deposit you wire reduces the capital available for the next acquisition. Two active deals at $200K EMD each means $400K sitting in escrow, unavailable for anything else. EMD financing breaks that zero-sum constraint.

The deposit is funded by the lender, your equity remains liquid, and you can pursue parallel acquisitions on their own underwriting merits rather than on whether your liquidity happens to be free that week.

As Duckfund's platform is built around exactly this use case, our "Sign Now, Pay Later" model allows investors to make multiple offers simultaneously – a structural advantage that compounds quickly on high deal-volume strategies.

- 1031 exchange acceleration

A standard 1031 exchange operates on two hard, non-negotiable timelines: a 45-day identification window and a 180-day close deadline from the date the relinquished property sells, per IRS §1031 requirements. Miss either date and the tax deferral collapses, meaning all capital gains from the sale become immediately taxable in that fiscal year.

The identification period is where EMD financing earns its keep in this context. A 1031 buyer already has a capital gains clock running. Tying up personal equity in escrow on a target acquisition while still in the 45-day identification window is a compounding problem.

Arthur Putzel of Trout Daniel & Associates has advised clients through exactly this situation. Because 1031 buyers already have a “capital gains gun to their heid”, Putzel advises his clients to ”Plan for the cash need before it's an emergency, not after.”

For these buyers specifically, EMD financing lets you put multiple replacement properties under contract simultaneously during the identification period — covering your 45-day deadline across more than one option — without deploying personal equity into each. One or more deals will close; the others exit on contingency and the deposits return. The cost is a defined, short-duration fee.

The EMD is where the deal starts

CRE operators who use EMD finance well know it's one of the most important moments in the entire transaction cycle. How fast you can move, how much you can commit, and how cleanly your PSA is structured determine whether you win the deal, protect your capital, or lose both.

The strategies covered here separate investors running one acquisition at a time from those building portfolio momentum in a market where deal competition is strong, and capital efficiency is the real differentiator.

That's exactly what Duckfund is built for. Fast deposit funding — approved in 24 hours, wired in 48 — that keeps your equity working on execution rather than sitting in escrow.

Your next deal won't wait. Neither should you. Join 4,000+ CRE investors who've secured over $1.5 billion in deals with Duckfund's Sign Now, Pay Later model. Get 48-hour approval, zero upfront capital, and discounted rates starting month four.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence