5 Smart Strategies to Raise Soft Deposit Financing for Your Next CRE Deal

In today’s competitive commercial real estate market, property deals are moving faster than ever. Earnest money requirements continue to strain investor capital. Here's how smart CRE professionals raise soft deposit financing to stay competitive.

While property values are stabilizing and opportunities are popping up across markets, one CRE challenge keeps many deals from closing: the up to 10% earnest money deposit to secure commercial properties.

With increasingly large deposits needed to grease prime CRE deals, many investors struggle with:

- Capital limitations that prevent investors from pursuing multiple opportunities simultaneously

- Speed requirements eliminate traditional financing options that take weeks for approval

- Market competition from institutional buyers who can close deals faster

With capital tied up in soft deposits, even the most experienced developers struggle to generate a healthy return in today’s landscape of elevated interest rates and tight lending standards.

Investors with multiple financing options can more efficiently raise soft deposit financing and keep a competitive edge. From traditional lending to innovative fintech solutions, five proven methods enable CRE professionals to secure earnest money deposits without depleting their working capital.

Read on to discover the financing strategies that separate successful CRE investors from those who miss opportunities.

[Secure more CRE deals without tying up your capital. Duckfund provides fast and easy earnest money financing.]

5 ways to raise soft deposit financing

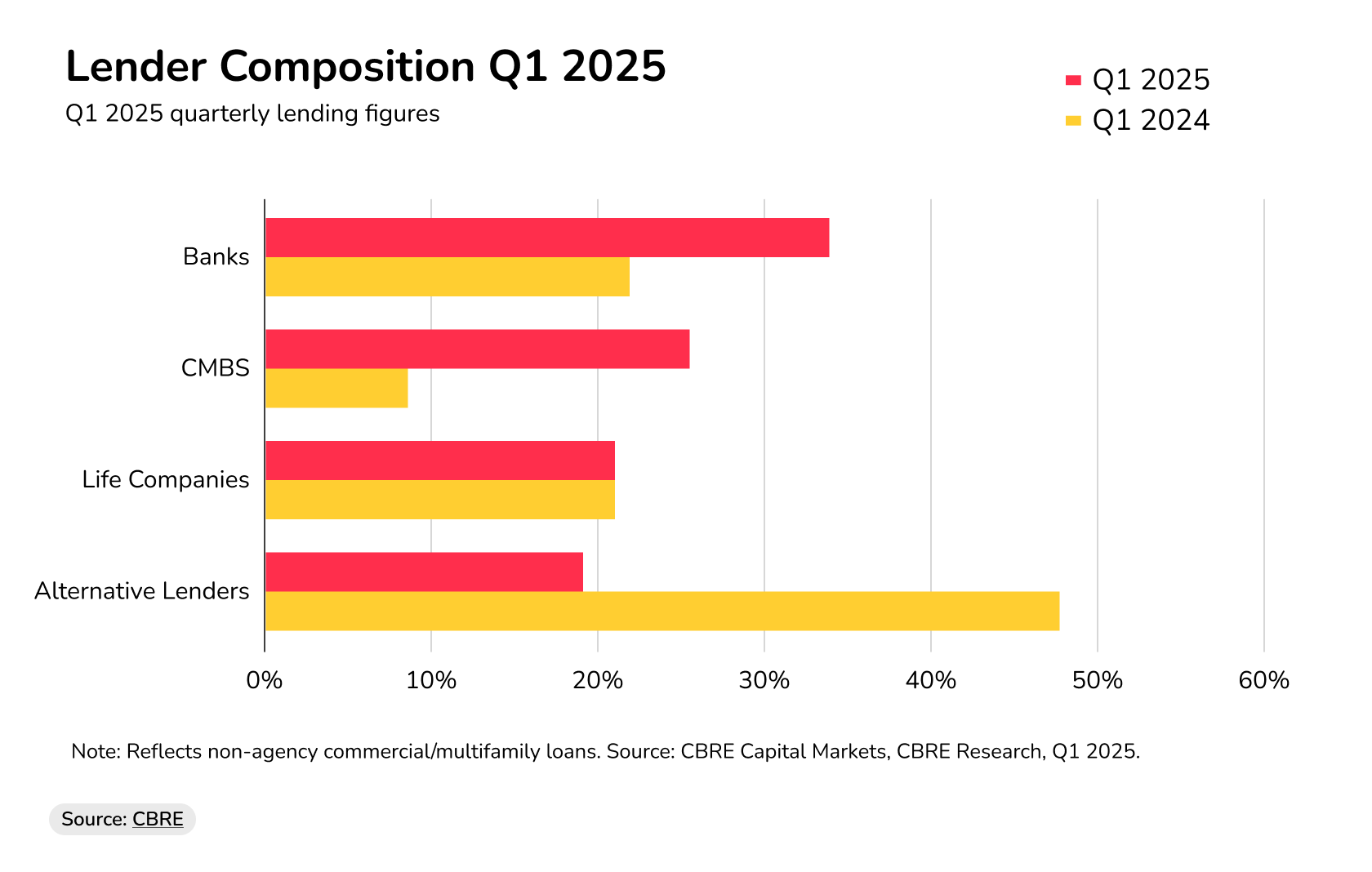

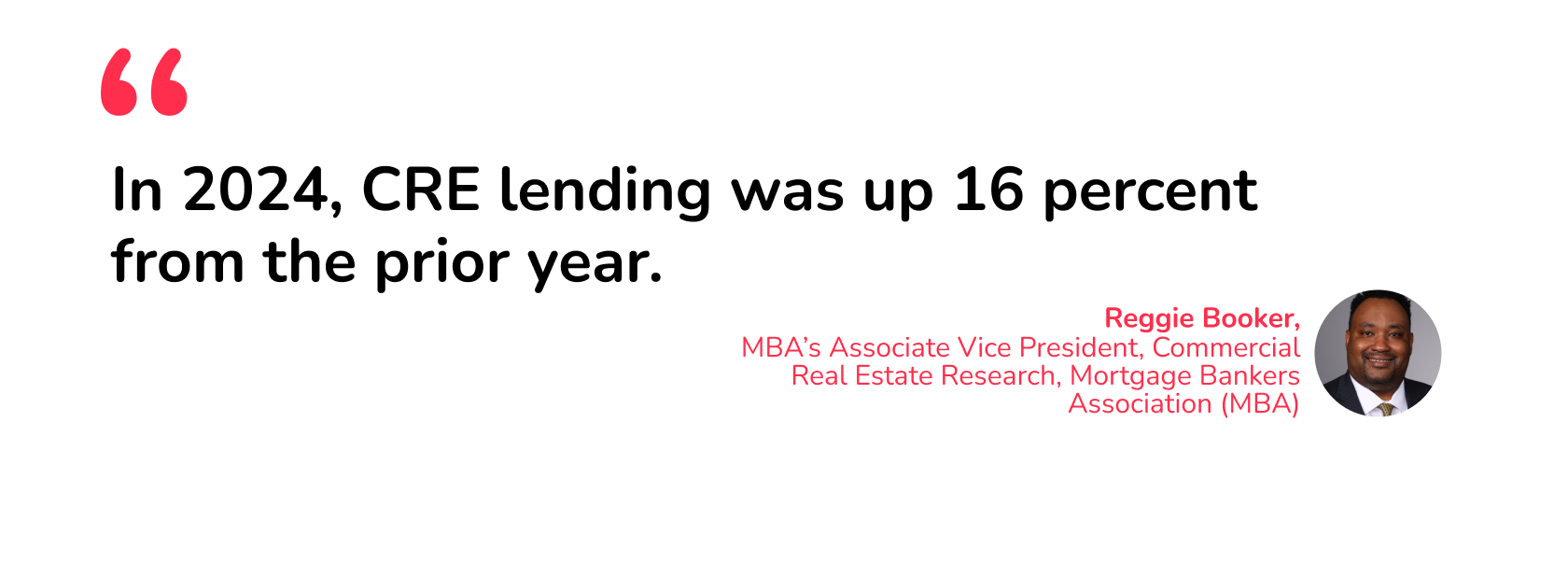

Total commercial real estate (CRE) mortgage borrowing and lending is estimated to be nearly half a trillion dollars in CRE lending during 2024, representing a 16% increase from the previous year.

Much of that lending is done by traditional financial institutions. And as the market turns more positive and banks offer better rates, these legacy institutions regain share of the total lending market, data from the CBRE shows.

Source: CBRE

“Commercial real estate lending rebounded to $498 billion in 2024, up 16 percent from the prior year and driven largely by multifamily activity and continued strength from dedicated mortgage banking firms, which closed $411 billion in loans,” said Reggie Booker, MBA’s Associate Vice President of Commercial Real Estate Research at the Mortgage Bankers Association.

Yet traditional loans provided by dedicated mortgage banking firms aren’t necessarily your only option. They’re certainly not always accessible to small-to-medium CRE investors

If you’re looking for good terms to fund your earnest deposit, consider these five options for investors to raise soft deposit financing:

1. Traditional commercial real estate loans

Interest rates might have remained higher than hoped, but the overall economic outlook has taken a positive turn. As a result, bank loans are becoming more affordable to commercial real estate investors.

Commercial mortgage spreads have shown improvement, averaging 183 basis points in Q1 2025 according to CBRE data, down 29 basis points year-over-year. This tightening indicates renewed lender confidence.

Pros and cons of using traditional bank loans to raise soft deposit financing

- Accessing funding through traditional financial institutions offers established lenders access to capital through proven banking relationships.

- Improved spreads make traditional commercial real estate loans more affordable and increase the loan amount borrowers can apply for with banks.

- The biggest drawback of traditional CRE financing for the goal of funding soft deposits remains processing speed. Bank approvals easily take weeks, making them unsuitable for competitive bidding situations where earnest money deposits must be submitted within 24-48 hours.

- Application processes with banks often require extensive financial documentation, including tax returns, financial statements, and detailed property and cash flow analysis.

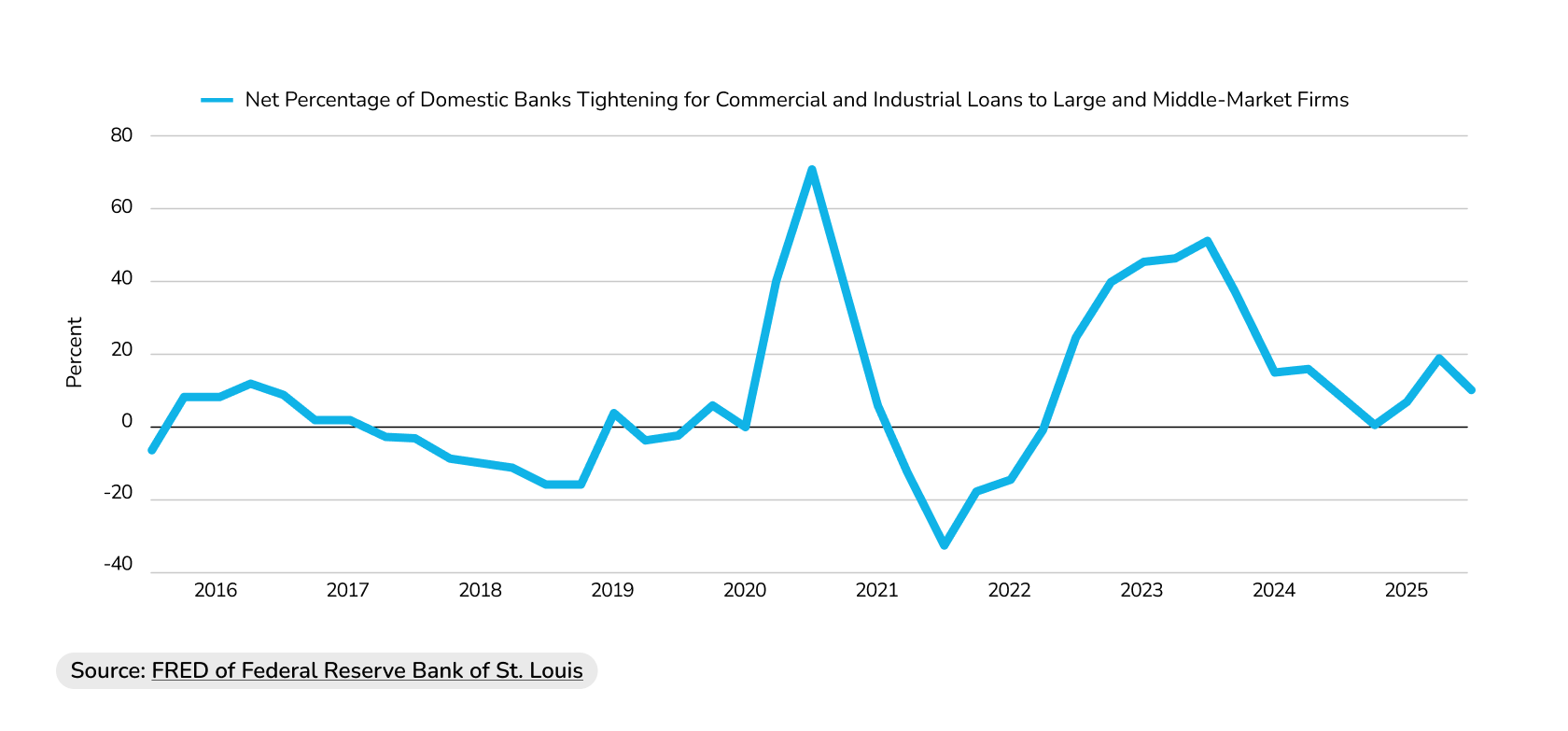

- Despite improved lender confidence, 9.0% of banks were tightening lending standards as of July 2025, according to data from the Federal Reserve of St. Louis. This shows that existing tight terms aren’t improving.

Source: FRED of Federal Reserve Bank of St. Louis

2. SBA loan programs

Government-backed business loans have gained appeal as traditional bank requirements remain tight. The Small Business Administration processed over $27.5 billion in 7(a) loans during fiscal year 2024, with a big portion supporting commercial real estate transactions.

Small business financing through SBA programs offers two primary paths for soft deposit funding: the 7(a) program for versatile real estate financing and the 504 program specifically designed for owner-occupied properties.

Pros and cons of using SBA loans to raise soft deposit financing

- Both programs provide government backing that reduces lender risk and improves approval odds for qualifying businesses.

- Extended repayment terms up to 25 years for commercial property financing help preserve cash flow while building equity in the underlying asset.

- Lower down payment requirements — as little as 10% for SBA 504 loans — free up capital for additional investments or operational needs.

- Approval rates remain challenging, with only 52% of SBA applicants receiving approval according to industry data, making qualification far from guaranteed.

- Long processing timelines due to extensive bureaucracy, like documentation requirements and multi-party coordination between lenders, CDCs, and the SBA.

- Strict eligibility criteria, like demonstrating job creation potential and owner-occupancy plans, limit accessibility for many CRE investors.

3. Hard money and bridge loans

When speed and flexibility outweigh cost, CRE investors turn to hard money loans and bridge financing for short-term capital solutions that help raise soft deposit financing quickly.

These asset-based loans rely primarily on property value and equity rather than borrower credit score, allowing for fast upfront funding to secure competitive deals.

Pros and cons of hard money and bridge loans to raise soft deposit financing

- Hard money loans offer some of the fastest closing times in the market, ideal when deposits must be wired to an escrow account within days to secure competitive deals.

- These lines of credit provide limited borrower qualifications and tailored terms, appealing to investors with complex financial situations.

- Bridge loans extend to other short-term real estate financing needs, like property renovations, bridging cash flow gaps, or securing good-faith deposits ahead of long-term loans.

- The costs of hard money and bridge loans are much higher, with interest rates typically ranging from 10% to 15% or more, plus additional origination and closing fees that can total several points of the loan amount.

- Loan terms are short and usually with balloon payments, meaning borrowers need a clear exit or refinance strategy to avoid financial distress.

- High fees and short durations make these loans less suitable for long-term investment strategies and require careful consideration of cash flow and market timing.

4. Private capital and investment networks

Private and alternative lenders have quickly filled the void left by traditional banks pulling back, providing vital liquidity to a diverse set of real estate assets, as bank JP Morgan notes.

Private lenders, including high-net-worth individuals, family offices, and real estate investment groups (REIGs), bring agility and customized solutions to the table that banks often cannot match.

Pros and cons of private capital and investment networks for soft deposit financing

- Private investors focus on value and potential of the underlying asset more than anything else, allowing for flexible underwriting.

- REIGs and syndications pool resources from multiple investors, expanding capital capacity for larger or niche commercial real estate deals, including industrial, multifamily, and mixed-use properties.

- Interest rates and fees vary widely depending on deal complexity and investor risk tolerance.

- Accessing private capital takes a strong network and/or credible track record. For newcomers or those with limited CRE history, this can be particularly challenging.

- Regulatory oversight is less when using private capital. Transaction transparency and due diligence are critical to avoid risky arrangements.

5. Digital soft deposit financing platforms

In 2025’s paced CRE market, alternative lenders are a powerful partner for CRE investors looking to gain an edge over the competition. Digital soft deposit financing platforms stand out among these new players. These fintech-driven solutions streamline earnest money financing with automated underwriting and funding in as little as 48 hours.

Anna Kogan, CEO of Duckfund — a leading digital soft deposit financing platform — explains, “We’ve structured our service to prioritize speed and capital efficiency, empowering CRE investors to act fast without impacting their debt capacity or existing lending relationships”.

Pros and cons of using digital platforms to raise soft deposit financing

- Digital platforms use innovative tech instead of cumbersome paperwork and manual credit reviews, accelerating approvals from weeks to days.

- These platforms offer competitive prices, mostly charging flat, transparent fees and low interest rates, allowing investors to better forecast financing costs.

- Digital providers support multiple simultaneous deals, enabling investors to scale their portfolios without liquidity bottlenecks.

- Digital platforms typically focus on one or a few financial products but lack broader CRE loan products that some investors require.

- Some platforms also focus on specific markets or property types, requiring investors to verify compatibility before application.

The evolution of financing options to raise soft deposit financing reflects the complexity and speed demanded by today’s CRE market. Traditional loans and SBA programs are still strong tools to have to your disposal, but can be slow and restrictive for the purpose of soft deposit financing. Hard money, bridge loans, and private capital might provide the agility needed but at higher costs and shorter terms.

In contrast, digital soft deposit financing platforms like Duckfund are specialized, tech-powered solutions that combine speed, transparency, and capital efficiency. If you want to move quickly without locking up up valuable capital in escrow, partnering with an innovative soft deposit funder can offer a decisive edge.

[Duckfund's soft deposit financing solutions empower investors to act swiftly on commercial property opportunities. Schedule a call with Duckfund now to discuss your transaction and get started with the top earnest money deposit provider in the market.]

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence