Confused by Transactional Funding and Soft Deposit Lending? How to Choose the Best One for Your Next Deal

Join any commercial real estate (CRE) conversation, and you might hear transactional funding and soft deposit financing get mixed up.

Yet these two key funding devices serve different buyers at different stages of the deal.

If you're a CRE investor, confusing one for the other can cause an expensive delay, especially when:

- Your capital is tied up in other deals, and you need the right funding to move on a hot new deal

- Your lender is running slow, and your deposit is at risk

- Your soft deposit goes hard before you have answers, and you find yourself negotiating from a losing position.

This guide breaks down how each product works, who each is built for, and why what most CRE investors need to do is to raise soft deposit financing.

We’ll cover:

- What is transactional funding in real estate, and how does it work?

- How much does transactional funding cost?

- When transactional funding makes sense (and when it doesn’t)

- What is soft deposit financing, and how is it different?

- How much does soft deposit or earnest money lending cost?

- Close your next deal in 48 hours with Duckfund

Need your soft deposit financing in under 48 hours? Contact us to find out how we can help you land your property ahead of rivals.

What is transactional funding, and how does it work?

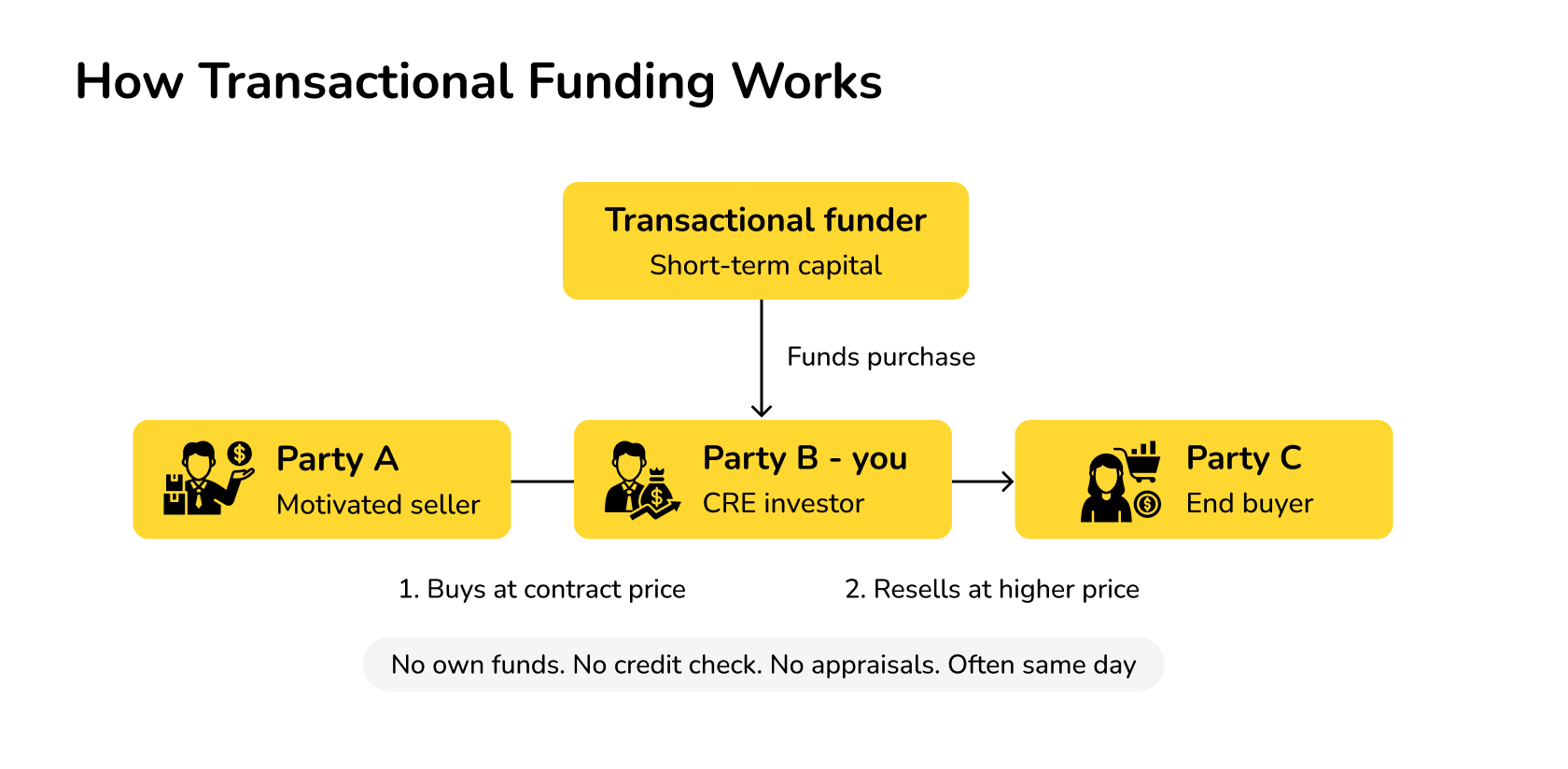

Transactional funding is a short-term loan that lets you buy a property that you’ll flip to another investor, often within a few hours. This same-day transactional funding is for something called a simultaneous or double closing.

We can view this as involving parties A, B, and C.

Party A is a motivated seller who wants to move the property on at a low price.

Party B is you, a real estate investor or wholesaler who will buy the property from them and has the deal under contract.

Party C is your end buyer, whom you’ve already agreed to sell to at a higher price.

A transactional funding loan makes the first part of the deal happen, so you can immediately sell on to C. It’s popular with investors because you get to buy a property upfront with none of your own funds, and its speed means there are no interest rate charges built in.

There are no appraisals involved, and very rarely any credit checks. Instead, the lender is underwriting the speed of the transaction, rather than your creditworthiness.

For the deal to work, you’ll need a title company and closing agent working closely together to coordinate the closings in sequence. They must also make sure the purchase contract on each side is airtight.

Transactional funding lenders will also need to see your proof of funds, as well as evidence that your buyer is ready to close, before they release capital.

Alternative terms

You may have come across the terms flash funding and same-day funding in this field. These are short-term financing options that perform the same function: they put up capital for just enough time to complete the transfer.

In any of these cases, the loan amounts vary from $10,000 to several million, according to the type of deal and transactional funding lender involved.

How much does transactional funding cost?

As you can see above, transactional financing in real estate doesn’t work like a traditional loan, which means it also prices differently.

To make it work, you usually pay a transaction fee, which might be a flat fee or a percentage of the loan amount. The latter is typically between 1% and 3%, which would come in at between $5,000 to $15,000, plus closing costs, for a $500,000 loan.

Some borrowers might view this as expensive for money that’s only in your hands for a few hours. Yet while it can put thin wholesale deals at risk, a healthy profit margin will often make it worth it.

When transactional funding makes sense (and when it doesn’t)

Transactional funding works best for real estate deals that have the following pillars in place:

- A confirmed end buyer (Party C)

- A clean and clear A-B-C chain with no contract gaps or title issues

- Synced timelines for the two deals – within hours, not days or weeks.

“When the buyer has a clear path through closing but needs short-duration capital to execute the acquisition structure cleanly, transactional funding makes sense,” says Matt Morgan, CRE Agent at Inland Pacific Advisors, a California-based CRE agency. “This includes certain back-to-back or assignment-sensitive scenarios.”

On these occasions, the best transactional funding options are much quicker and smoother than traditional financing. It also means you get to keep your own funds out of the deal.

Yet, such a carefully built deal can also be a precarious one. If one link of the chain fails, then the whole structure is at risk of collapse.

When transactional funding becomes the wrong tool

Many real estate investing pros make the mistake of reaching for transactional funds when it’s not the right time or place.

A very common scenario is when the investor is still working out whether an opportunistic deal is financeable through the purchase contract. At this stage, they haven’t completed due diligence and are waiting on third-party reports. They also probably haven’t fully secured a capital stack.

“(Transactional funding) becomes the wrong tool when the investor's business plan includes any significant value-add, development, or longer-term hold strategies that require more traditional, patient capital and due diligence,” says Jack Donahue, SIOR, President and Advisor of Donahue Real Estate Advisors. “ I’ve seen this play out in various Pittsburgh deals.”

In these cases, the investor needs financing options that buy time, such as gap funding, rather than the ticking clock that short-term capital brings with it.

What is soft deposit financing, and how is it different?

Soft deposit financing is a solution for a later stage of real estate transactions: to cover the soft deposit, or earnest money deposit (EMD), that confirms your serious intent to buy real estate.

The need for this type of financing is real: earnest money in commercial real estate can now reach up to 10% of the property value in hot markets, and often runs into hundreds of thousands of dollars.

If you don’t have this type of down payment ready, then a soft deposit lender – like Duckfund – will quickly fund this amount on your behalf. They’ll put it into an escrow account while you and your team work through diligence, lender timelines, and equity questions.

You might find yourself asking the question, “Is earnest money refundable?” In short, yes, but while the deposit remains soft.

Your EMD is protected during the contingency period, giving you the right to walk away and recover your deposit if diligence reveals a problem, your financing falls through, or the deal simply doesn't stack up. Once the deposit goes hard, however, that protection expires.

In contrast to transactional funding, soft deposit financing buys you time while you find out whether the deal works. It keeps you in the deal while you work through diligence and your lender underwrites, without tying up capital you might need elsewhere.

How much does soft deposit or earnest money lending cost?

The best soft deposit providers work on a quick turnaround, so they price for speed. But what you pay depends heavily on which type of lender you use, and on what their fee is actually calculated against.

It's worth clearing up a common mix-up first. A traditional bank won't fund your earnest money deposit at all: it underwrites the acquisition loan, and its origination fee (typically 0.5%-1%) is charged on the loan amount, not the property's value. So a bank isn't really an option for covering your deposit in the first place.

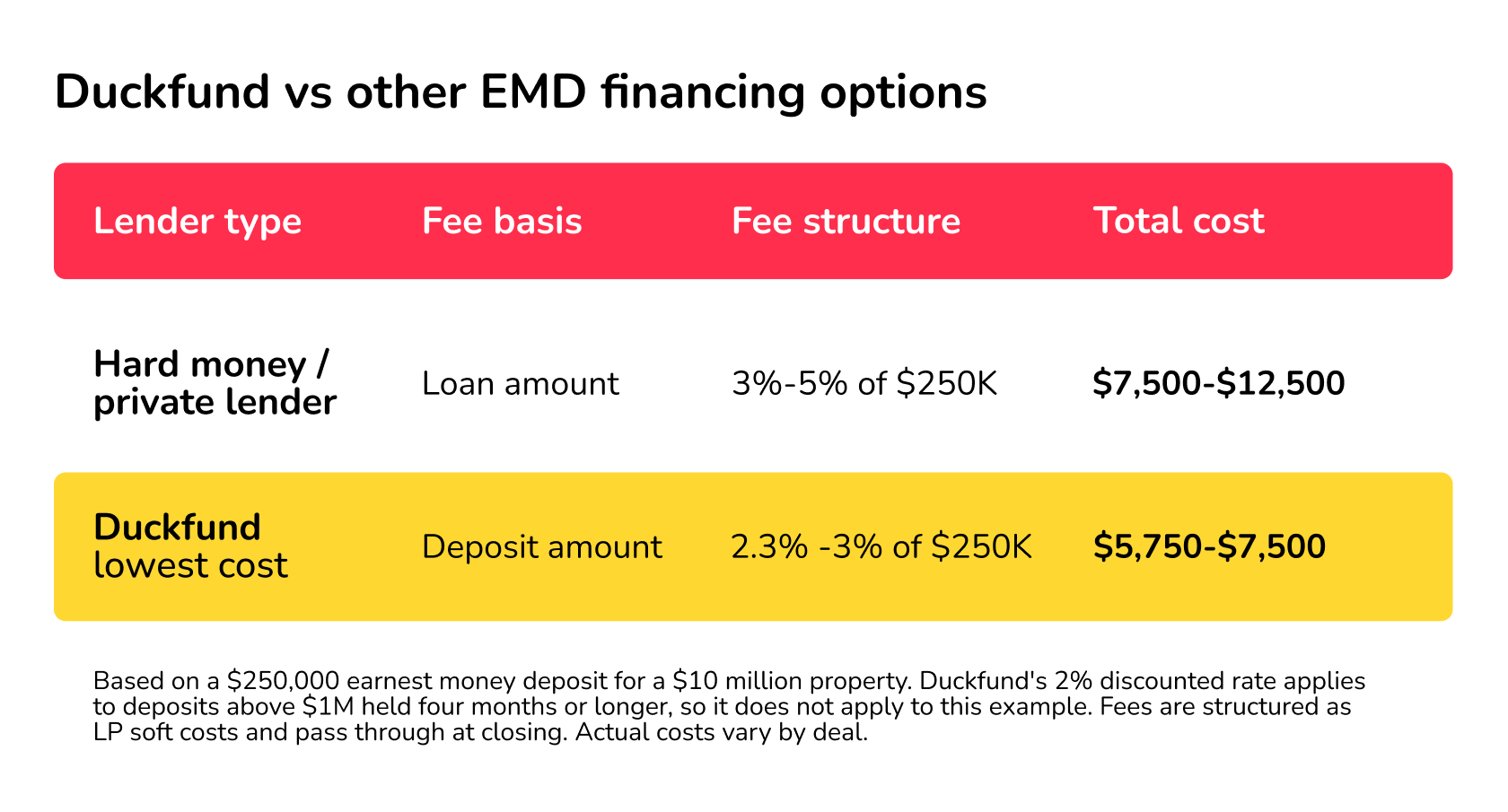

The lenders that will fund your EMD price it very differently:

- Transactional lenders can charge up to 40% of the deposit, but they're built for wholesalers running same-day double closings, not CRE sponsors acquiring a $10 million asset, so that pricing rarely applies to a deal like yours.

- Hard money and private lenders typically charge 3%–5% of the amount they fund.

Duckfund's structure is more economical. We charge a fee of 2.3%–3% of the deposit amount, with a discounted rate of 2% available for deposits above $1 million held for four months or longer. Fees are structured as LP soft costs and pass through at closing.

Here's how that plays out on a $250,000 earnest money deposit for a $10 million property:

The numbers speak for themselves: the cost of soft deposit or earnest money lending varies greatly depending on which provider you use.

Yet beyond the cost difference, the more important point is this: soft deposit financing isn't a cheaper version of transactional funding — it's a different tool entirely, built for a different stage of the deal.

Using the right one at the right moment is what keeps your capital working and your deal alive.

Secure your next deal in 48 hours with Duckfund

If you have a double deal ready to go, with timelines and end buyer in sync, then transactional finance is an ideal funding lever.

Most CRE purchases don’t have this. First, you must work through a purchase agreement or wait on a lender, and transactional lending will simply add a ticking clock to the process. Instead, you need capital that buys you time.

Duckfund was designed just for this. We fund your earnest money deposit in 48 hours, with no collateral and no credit score check, so your own liquidity stays free while your deal takes shape.

The wrong tool at the wrong stage costs you deals. The right one wins them.

Duckfund funds your EMD in 48 hours, no collateral required. Sign up for Duckfund and keep your capital free while your deal takes shape.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence