Earnest Money in Colorado: Learn to Seal Your Property Deal Faster

Colorado's commercial real estate market is seeing some structural changes. In this dynamic and fast-paced landscape, good real estate deals aren’t just hard to find – they’re also increasingly hard to close. Smart use of earnest money in Colorado has become more important than ever.

But understanding your earnest money Colorado requirements isn't only about knowing the percentages you lock up in escrow. It's more about reading which sectors are distressed and which are resilient, and how to raise soft deposits in a market where interest rates remain stubbornly high while traditional financing has tightened.

On top of that, Colorado also updated its earnest money release protocols with better legal protection and stricter dispute resolution timelines. Investors who aren’t up to date with these changes risk losing deposits or missing deals entirely.

In this updated CRE guide on earnest money in Colorado, we’ll walk investors through everything they need to know about:

- How much earnest money is required in Colorado across property types

- What's changed in Colorado's CRE market

- Colorado's new earnest money release form and refund procedures

- Updated payment timing and methods that align with 2025 best practices

- Pro tips for protecting deposits in today's financing environment

- How soft deposit financing creates competitive advantages when capital is tight

The markets are moving and competition is stiff. Read on how to gain an edge in real estate transactions with earnest money in Colorado.

[Looking to move quickly on Colorado CRE opportunities but struggling with earnest money requirements? Sign up for flexible soft deposit financing options designed for today's market — with approval in just 48 hours.]

How much earnest money is required in Colorado

How much earnest money is required in Colorado for commercial real estate deals in 2025? The standard amount of earnest money sits between 1% and 5% of the purchase price, but market conditions create huge variations across areas and property types.

Earnest money transactions — sometimes called good faith deposits or soft deposits — are payments buyers make upfront to demonstrate serious intent to purchase a property, whether that’s a home purchase or big CRE deal.

Buyers deposit funds in an escrow account with an escrow agent or title company when signing purchase agreements, and these deposits normally credit as a down payment toward the closing cost.

If deals collapse due to valid contingencies, buyers usually recover their earnest money. Walk away without justification? Sellers keep it.

But more on how earnest money disputes are decided in Colorado later. Let’s first get more specific on earnest money amounts.

Unlike residential transactions in a home buying process, where earnest money amounts are relatively standardized, commercial real estate operates in a more negotiable landscape where deposit requirements can swing from less than 1% to 15% of the sale price, depending on market dynamics.

Here's what earnest money in Colorado looks like across sectors in 2025:

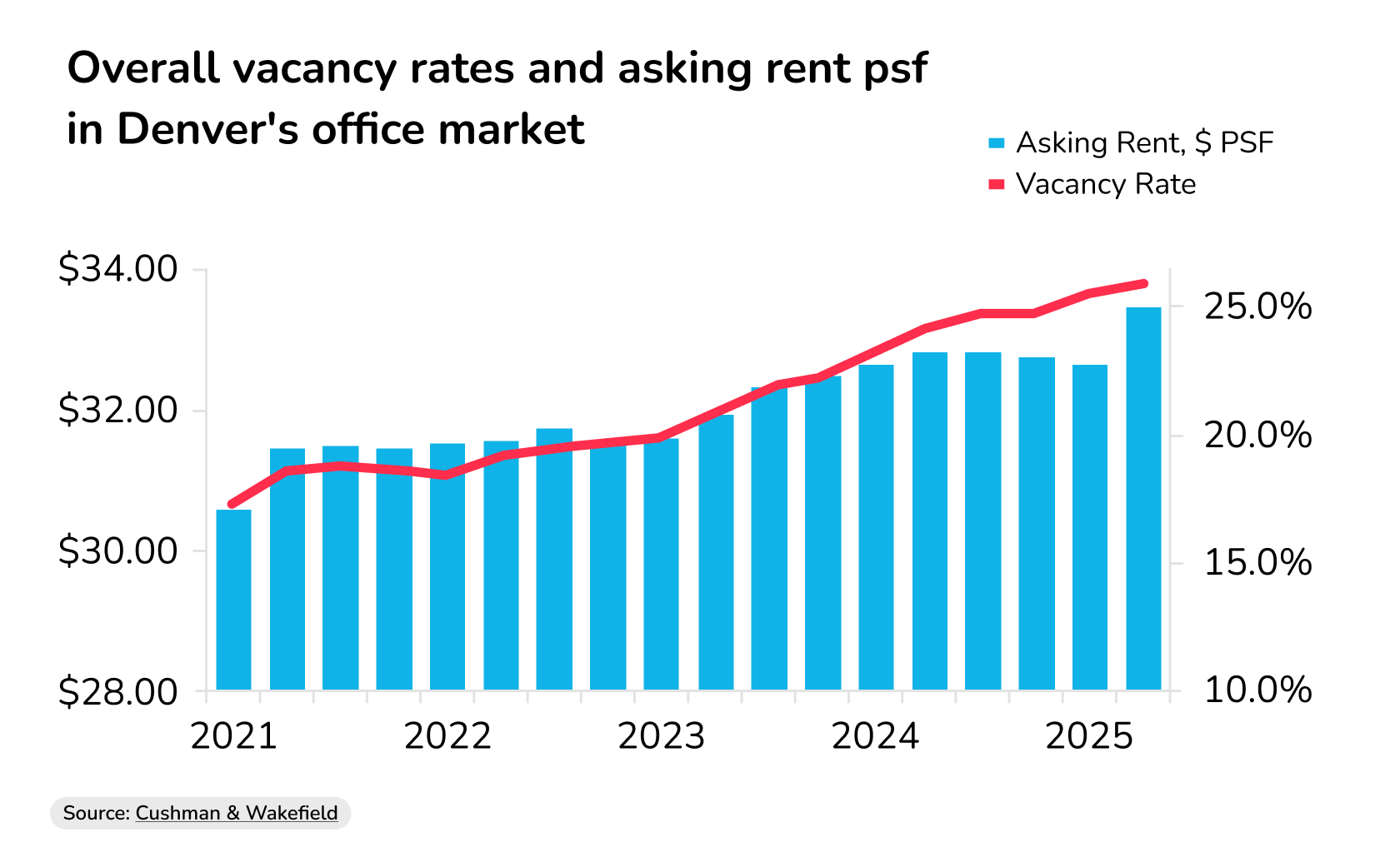

CRE in Colorado: Office properties

Office properties are deeply distressed, with overall vacancy rates in Metro Denver hitting 25.9% in Q2 2025, according to CRE consultancy Cushman & Wakefield, and net absorption rates falling. This gives buyers tremendous leverage and lowers earnest money amounts.

Source: Cushman & Wakefield

CRE in Colorado: Industrial properties

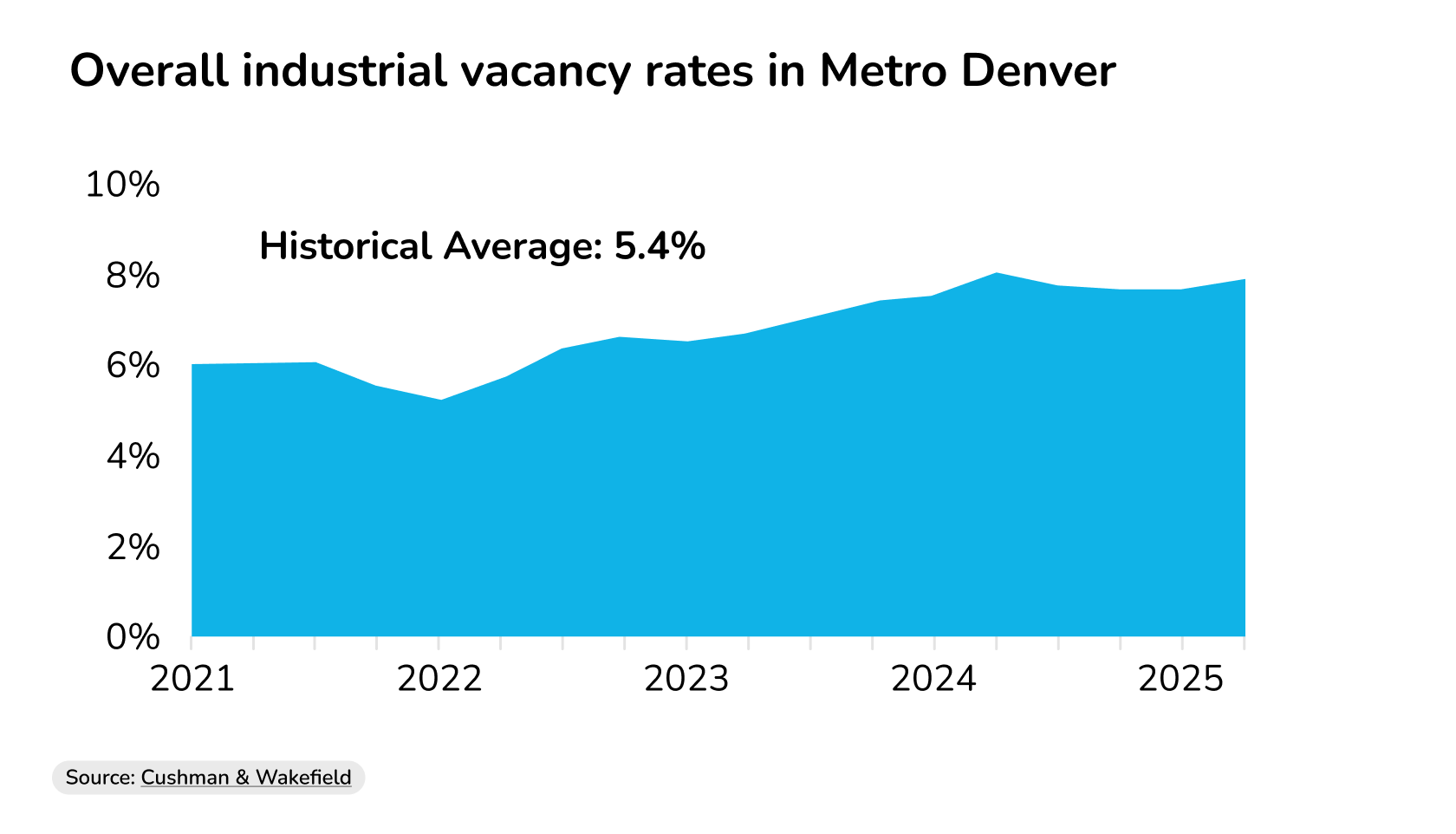

Industrial properties show moderately weak fundamentals at 7.9% vacancy rates and climbing, as Denver’s unemployment rate remains above national averages. Expect to pay standard soft deposits between 2-5%.

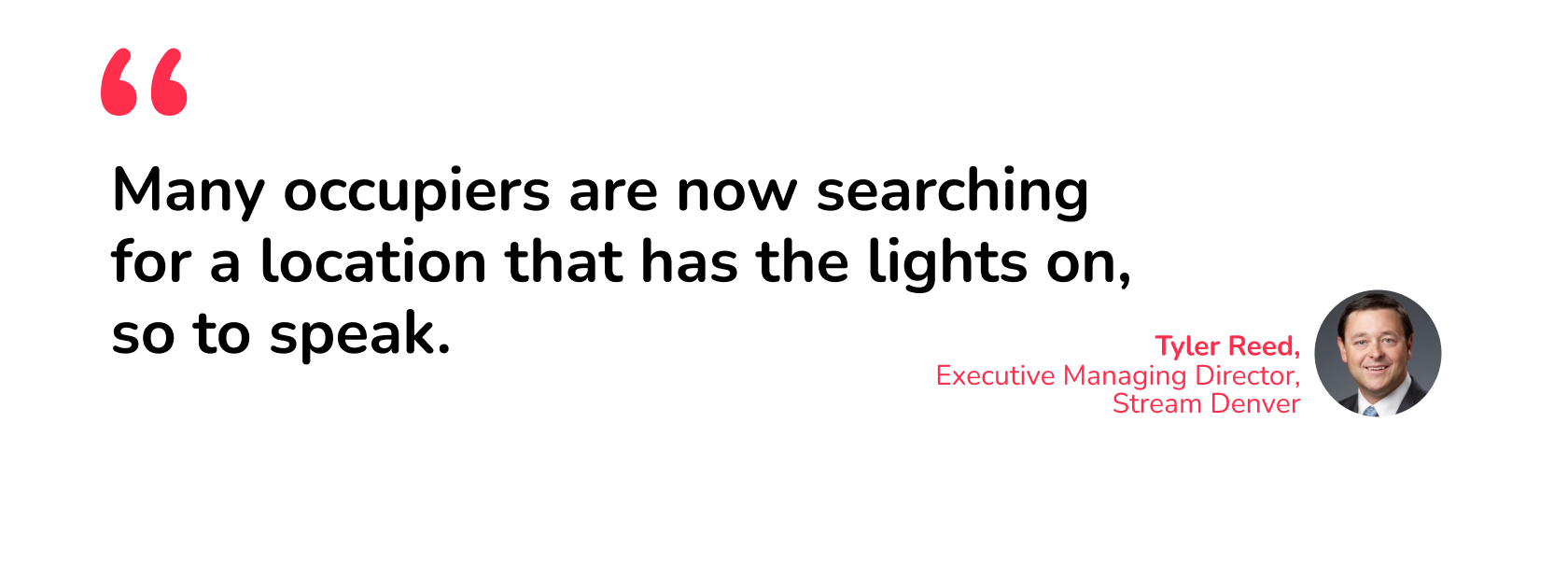

However, Tyler Reed, Executive Managing Director for Stream Denver, notes Denver industrial is "experiencing positive growth" and remains "on pace to remain within historical averages" for absorption rates despite reported negativity. What he sees is a flight towards turn-key facilities.

Overall industrial vacancy rates in Metro Denver

Source: Cushman & Wakefield

“Many occupiers are now searching for a location (whether within a new construction or infill building) that has the lights on, so to speak, with speculative office suites, certificates of occupancy, and all the elements needed for rapid occupancy entirely in place,” Reed notes. With higher demand, CRE developers with such properties can demand bigger soft deposits during the negotiation process.

CRE in Colorado: Data centers

Data center properties deserve special attention as a subsector. Data centers command premium demand and high soft deposits as the AI infrastructure boom drives demand. Denver now hosts 20.1 megawatts across 27 facilities, CBRE reports, with Flexential breaking ground on its fifth Denver center.

CRE in Colorado: Retail properties

Retail properties dominate as the strongest sector. Retail properties in select submarkets are commanding premium earnest money deposits as investors compete for scarce inventory. Colorado Springs retail vacancy sits at just 5.2%, according to local CRE firm Rocky Mountains CRE.

CRE in Colorado: Multi-family properties

The multifamily sector is stabilizing in North Colorado amid strong leasing demand and moderating construction, supported by solid rent levels and a balanced pipeline, CRE platform Crexi reports. Buyers should look at normal to elevated earnest money rates.

Colorado Spring has earned Realtor.com's #1 housing market ranking at the start of 2025 – with a projected 27.1% year-over-year sales growth. Prime locations in Colorado Springs require higher deposits and fast negotiation.

What's changed in the CRE market – and what it means for earnest money

These earnest money variations reflect deeper structural shifts reshaping Colorado's commercial real estate landscape — shifts that determine who holds leverage during negotiations.

Metro Denver's economy grew 2.7% in Q2 2025, according to the CBRE, a little below the national 3.0%. Unemployment hit 4.8%, up 70 basis points year-over-year and above the 4.1% national rate. Weak job growth translates directly to rising vacancies and cautious tenant demand.

These trends should cool down the property markets in Colorado, with sellers accepting overall lower deposits because they feel pressure to close deals.

However, tight capital markets have pushed earnest money in the opposite direction. With traditional loans harder to come by and federal rates higher for longer, sellers will want assurance that buyers won't walk away due to financing problems after having tied up the seller’s property for 60-90 days.

Similarly, buyers need better protection when lenders tighten requirements. Financing contingencies matter more than ever, as do other common contingencies like inspection contingency.

Colorado’s new earnest money release form and refund procedures

The Colorado Real Estate Commission addressed these and other protection concerns by updating its earnest money release protocols in new real estate brokers contract forms. The state's Division of Real Estate mandates the EMR83-6-21 form — officially "Earnest Money Release (with Mutual Release and Indemnification)" from January 22, 2022.

This updated earnest money release form for Colorado strengthens mutual release provisions, requiring both parties to release all transaction-related claims when earnest money returns. It adds indemnification language protecting escrow agents from liability when following proper procedures.

Most significantly, the form establishes a 120-day deadline for parties to initiate legal action on disputed earnest money. Disputes previously dragged on indefinitely, tying up funds while both parties rack up costs with real estate attorneys. The new timeline forces faster resolution.

When is earnest money refundable? Financing contingencies deserve special attention with today’s capital constraints. Buyers must demonstrate "reasonable efforts" in obtaining financing, with multiple lender contacts and complete documentation. Purchase contracts should explicitly define expectations to avoid disputes over genuine effort versus cold feet.

Buyers can lose their deposits through breach of contract without valid contingency protection — missing deadlines, walking away after contingencies expire, or failing to deposit earnest money as agreed all trigger forfeiture. In such cases, earnest money is non-refundable.

Earnest money payment timing and methods

When does earnest money in Colorado get paid? Standard purchase contracts require deposits within 2-4 business days after agreement execution, though distressed office deals sometimes negotiate 10-day windows.

Wire transfers dominate as the preferred method — immediate verification, same-day clearing, clean audit trails. Cashier's checks work but take an additional 3-5 days to clear.

Never transfer earnest money into a seller’s bank account directly. Colorado law mandates that deposits flow through licensed escrow agents or title companies. Direct payments void EMR83-6-21 protections.

Title companies handle most transactions, managing escrow through closing. Timing matters competitively in commercial real estate purchases. Hot sectors like Colorado Springs retail expect 24-48 hour deposits, signaling serious intent when multiple buyers compete.

5 tips for protecting your soft deposit in Colorado’s CRE market

Smart investors protect earnest money Colorado deposits through strategic contingency structuring, a critical step in a dynamic market where deals are fast-paced and lending is tight. Below are five tips to help you draft better real estate contracts and protect your soft deposit.

- Financing contingencies need precision

Explicitly define "reasonable efforts". Specify minimum lender contacts (three to five), documentation deadlines, and acceptable rate ranges tied to current federal benchmarks. Include termination provisions if rates exceed predetermined thresholds, protecting deposits when conditions deteriorate. - Due diligence periods deserve negotiation

Standard 30-60 days often prove insufficient in today's financing environment. Request 60-90 days for complex deals requiring multiple lender conversations. More time means better financing odds before earnest money goes "hard" (non-refundable). - Inspection contingencies extend beyond physical condition Include language covering financial verification—rent rolls, tenant credit, and lease terms. Discovering misrepresented income triggers valid termination, protecting deposits.

- Attorney timing matters

Contracting a good commercial real estate attorney before signing an agreement (instead of after disputes) can save a lot of headaches. Legal review ($2,000-$5,000) proves trivial compared to losing six-figure deposits through poor contract language. - Structure earnest money in tranches when possible

Initial "soft" deposit (refundable), then "hard" deposit (non-refundable) after the due diligence. This offers both parties peace of mind, protecting capital while demonstrating escalating seller commitment.

How soft deposit financing creates a competitive edge in today’s market

Colorado's challenging CRE environment and tight financial markets make capital preservation more important than ever. That's where soft deposit financing transforms how investors approach earnest money Colorado transactions.

Traditional financing forces investors to choose: tie up significant capital in escrow for 60-90 days, or lose competitive deals to better-capitalized buyers. Soft deposit financing eliminates this tradeoff entirely.

Duckfund specializes in earnest money deposit financing for commercial real estate investors, covering deposits from $25,000 upward with approval in just 48 hours. Instead of locking cash in escrow accounts, investors maintain liquidity for multiple opportunities—crucial when prime real estate in Colorado Springs or Denver data centers presents time-sensitive deals.

[Duckfund's soft deposit financing solutions empower investors to act swiftly on commercial property opportunities. Schedule a call with Duckfund now to discuss your transaction and get started with the top earnest money deposit provider in the market.]

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence