Earnest Money Deposits vs Down Payments: Clarifying A Common Confusion

Real estate deals rarely fall apart because of a lack of interest. More often, they collapse because of confusion about money, specifically, how much needs to be paid and when.

One of the most common sources of that confusion is the difference between earnest money deposits and down payments.

Many buyers assume they are essentially the same thing, or that earnest money is simply a prepaid down payment. But that assumption can lead to serious problems when it’s time to move a deal forward.

In reality, these two payments serve very different purposes in a real estate transaction. Earnest money signals commitment at the start of negotiations, while the down payment is what ultimately helps secure financing and close the deal.

Understanding how each works and how they interact can make the difference between closing smoothly and scrambling for cash at the last minute.

In this guide, we break down how earnest money deposits work, how down payments work, the key differences between them, and how investors can secure both when pursuing residential or commercial real estate deals.

We’ll cover:

- How do earnest money deposits work?

- How do down payments work?

- Earnest money vs down payment: Similarities and differences

- How to secure earnest money and down payment for real estate deals

[Do you want to close commercial real estate deals, but you don’t have cash to pay earnest money? Sign up for Duckfund to get the cash you need in just 48 hours.]

1. How do earnest money deposits work?

The usage of earnest money deposits in real estate

Also known as a good faith deposit, good faith money, and earnest deposit, this is an amount that the seller (directly or through a real estate agent) requests a potential buyer to pay to show commitment and seriousness towards the purchase of a given property.

“It tells the landlord you're serious enough to take the space off the market while due diligence runs its course,” according to Jack Donahue, founder of Donahue Real Estate Advisors, a CRE advisory firm.

Also, the seller may not schedule a commercial property or home inspection and negotiation without this payment.

Earnest money deposits are now as common in the residential home buying process as in commercial real estate (CRE). Even when the seller does not request it, buyers often propose to pay it as a way of showing commitment and to get an edge over other candidates for the property.

Who receives the earnest money deposit?

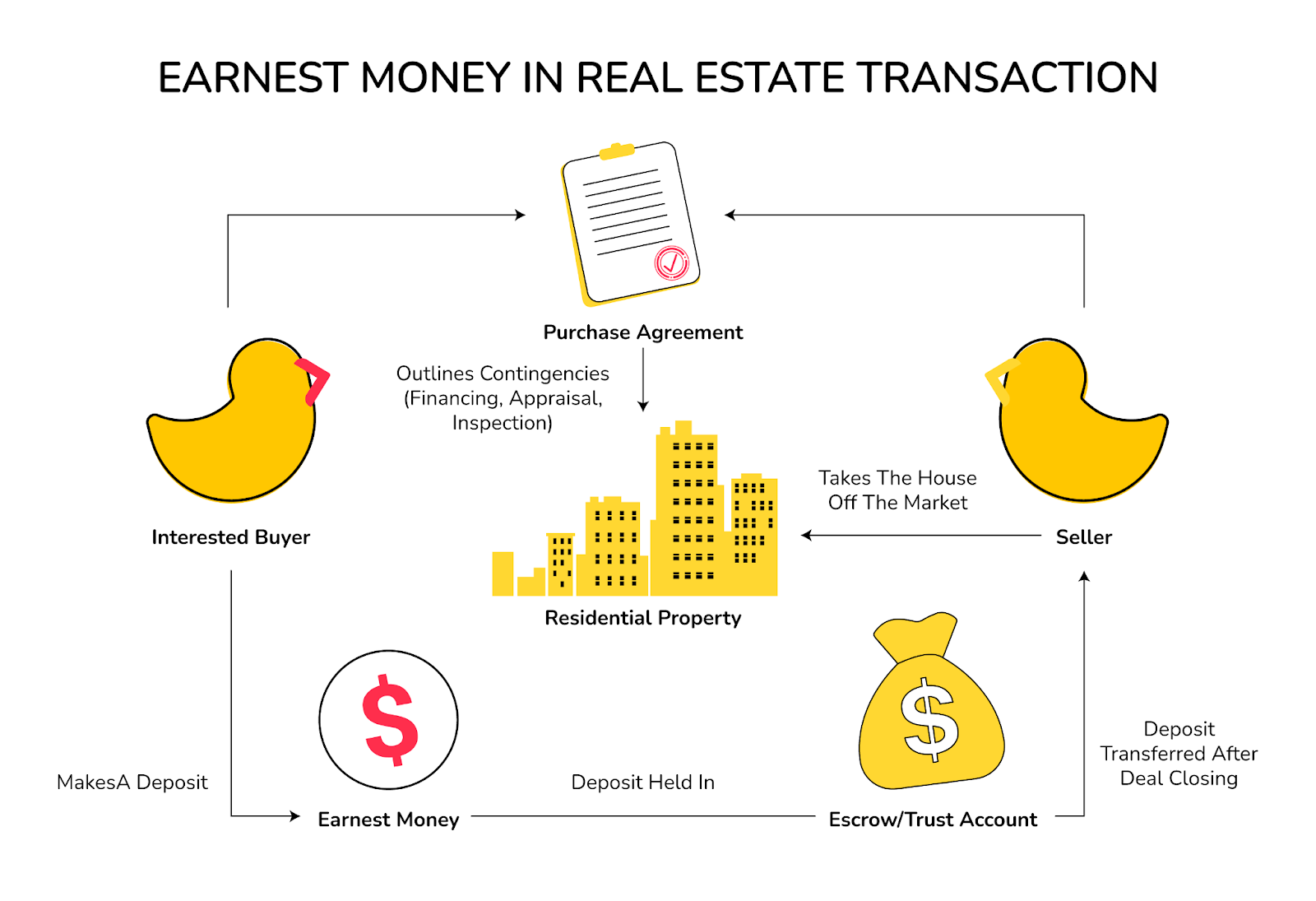

Though it is the seller who requests the earnest money deposit, the money goes to an escrow. The escrow keeps the money on behalf of both the buyer and the seller.

Once the earnest money deposit has been paid to the escrow, the buyer and the seller will prepare and sign a purchase and sale agreement (PSA).

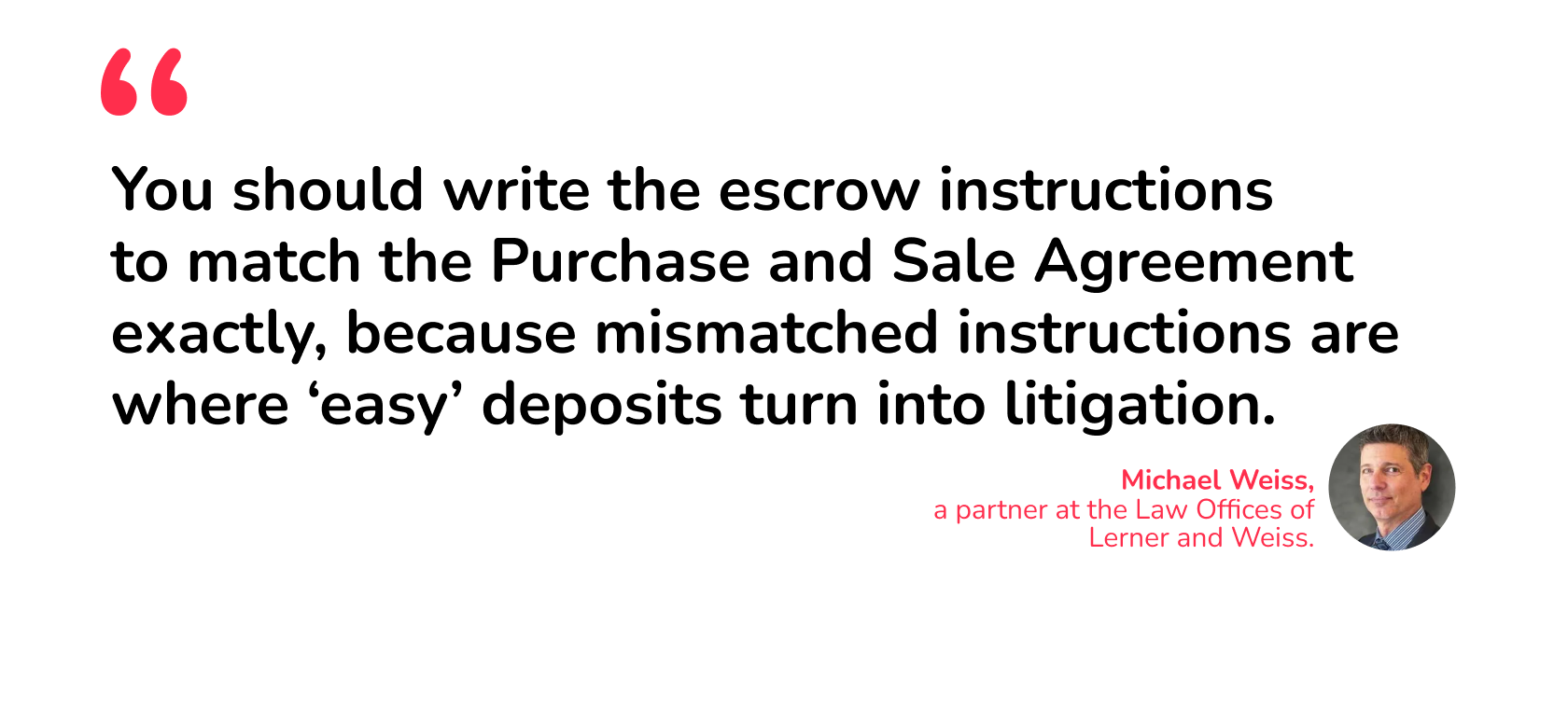

Escrow instructions are based on the PSA. This is why the PSA must be as specific as possible.

“You should write the escrow instructions to match the PSA exactly (who can demand release, what documents trigger release, and how disputes are handled), because mismatched instructions are where ‘easy’ deposits turn into litigation,” according to Michael Weiss, a partner at the Law Offices of Lerner and Weiss.

This structure can be better visualized in the chart below:

Who gets earnest money if a deal falls through?

The payment of the earnest money deposit confers on the buyer the option, but not an obligation, to purchase the property.

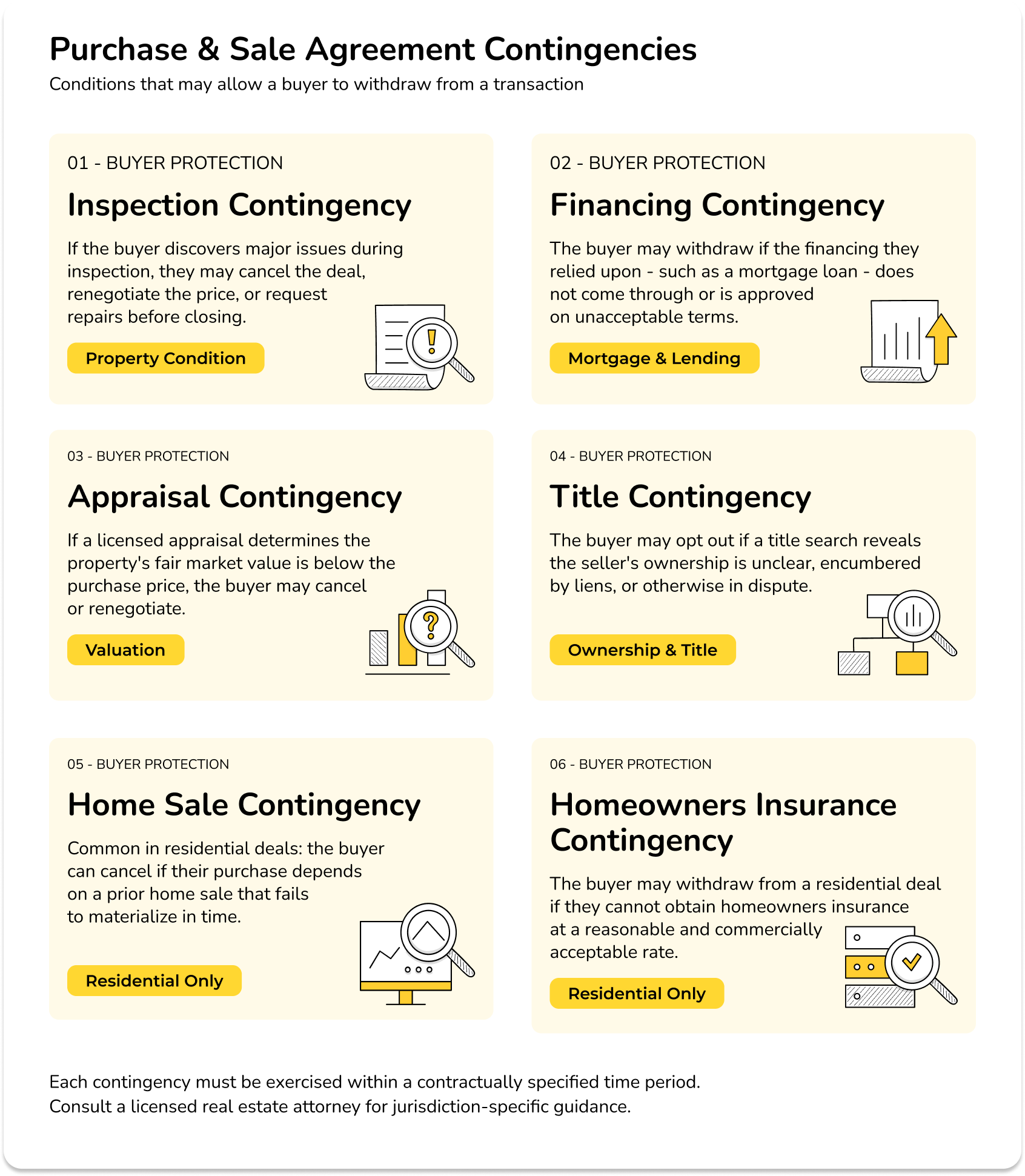

A typical purchase agreement will include contingencies that might make the buyer pull out of the deal. Some of the common contingencies include:

- Inspection contingency: If the buyer (through a property or home inspector) finds major issues with the property, they can cancel the deal, renegotiate the price, or request repairs.

- Financing contingency: The buyer can also opt out of the deal if the financing they were depending upon did not come through.

- Appraisal contingency: If an appraisal shows that the property is not worth the purchase price, the buyer can cancel the deal.

- Title contingency: The buyer can opt out of the deal if the seller’s title to the property is not clear or in dispute.

- Home sale contingency: For residential real estate, the buyer can cancel the deal if the purchase depends on a prior sale of their current home that does not materialize.

- Homeowners insurance contingency: The buyer can pull out of a residential real estate deal if they cannot find homeowners' insurance at a reasonable rate.

You can better visualize these with the chart below:

These contingencies are often time-bound: there is a deadline for inspection, loan approval, title verification, among others. If a buyer pulls out of the deal for a valid contingency whose deadline has expired, the earnest money will be nonrefundable.

Also, there are times when the buyer pulls out of a deal for a reason that is not part of the specified contingencies.

Furthermore, the deal may fall through because the seller is no longer interested.

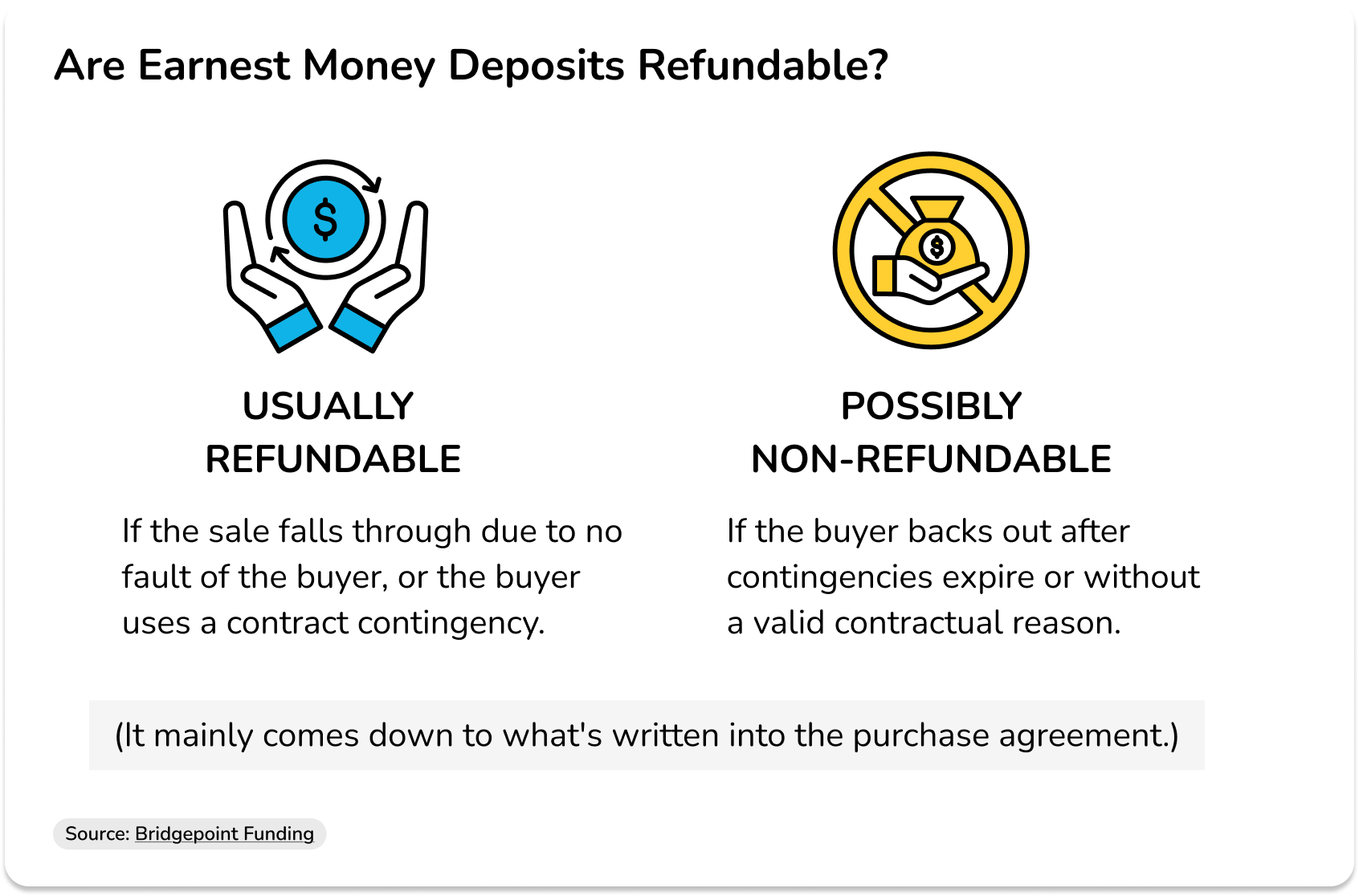

Are earnest money deposits refundable?

The answer to this question depends on why the deal is falling through. Let’s consider the three broad reasons:

- Seller pulls out of the deal: You can get earnest money back if the seller pulls out of the deal, for whatever reason.

- Buyer pulls out of the deal due to preagreed contingencies (within the stated period): The escrow will return the earnest money to the buyer if the buyer pulls out of the deal because of any of the contingencies included in the purchase and sale agreement.

However, as said before, the contingencies must still be valid when the buyer chooses to rely on them.

- Buyer pulls out of the deal for other reasons: The buyer will likely forfeit the earnest money to the seller if they pull out of the deal for a reason not clearly agreed upon in the purchase and sale agreement.

Many buyers choose to claim a refund by taking the matter to court. However, such cases are often decided in favor of the seller. This is because the whole point of the good-faith deposit is to prevent buyers from unnecessarily wasting sellers’ time.

We can summarize all of these in the chart below:

Source: Bridgepoint Funding

What happens to earnest money if the deal succeeds?

Does earnest money go towards the down payment or closing costs when the deal succeeds?

This is one of the key questions that causes confusion about the nature of earnest money deposits and how they differ from down payments.

Earnest money is usually paid out in one of two ways.

First, it can be included as part of the down payment for the property (see below for what a down payment is). That is, if an earnest money deposit of $100,000 has been paid and the down payment is $1,000,000, the buyer will now be required to pay $900,000 instead of $1,000,000.

Secondly, the soft deposit can be used to cover all or part of the closing costs of the deal. Closing costs include loan origination fees, discount points, appraisal fees, title searches, title insurance, surveys, taxes, deed recording fees, and credit report charges, according to Investopedia.

Suppose the earnest money deposit is $100,000, and the closing costs add up to $200,000. Now, the buyer will only be required to pay $100,000 to close the deal.

There are no tight rules on how the earnest money is applied when the deal succeeds. The escrow will act based on the agreement between the seller and the buyer as stated in the purchase and sale contract.

How does the use of EMD differ in commercial and residential real estate?

Since CRE deals are bigger and often involve professional investors, EMD tends to play a larger role.

One manifestation of this is that while EMD in residential real estate can typically range from 1-3% in most markets, it can be as high as 10% in many CRE markets.

“In residential, the earnest money deposit is usually 1-3% of the purchase price,” said Josh Katz, founder of Universal Tax Professionals, a tax advisory firm. “Commercial real estate is a whole different animal. Your EMD can run 5-15% because sellers are taking property off the market for months while you do due diligence.”

Also, while residential real estate contracts are generally standardized, CRE deals are more flexible and customized. Thus, CRE buyers are more likely to compete based on EMD in very competitive markets.

Furthermore, there are often more contingencies in residential real estate. Since the buyers are individuals, there is greater emphasis on consumer protection. Though contingencies also apply in CRE, buyers and sellers are often professional investors who are left to protect themselves by paying attention to every fine detail.

“Residential EMDs have more consumer protections – you can usually get it back if inspection turns up problems,” according to Katz. “Commercial contracts are tighter, you can lose that five-figure deposit faster if you miss a deadline.”

2. How do down payments work?

The usage of down payments in real estate

A down payment is a portion of the purchase price of a property that the borrower pays upfront in a mortgage transaction.

The median down payment in the US is between 10% and 35%, as noted above.

In a mortgage transaction, the down payment serves various purposes.

First, it is a way for the lender to be sure that the borrower has the capacity to make subsequent payments. The logic is that someone who can’t pay a portion of the purchase price now may struggle to meet subsequent monthly payments.

Second, it is a way for the lender to reduce its risk (by reducing the amount it needs to lend to the borrower). This is why lenders with a government guarantee (through FHA loans, SBA loans, and Fannie Mae and Freddie Mac programs) can offer lower down payment requirements than traditional lenders, since they are taking on lower risk.

Third, it is also a way for the borrower to get better loan terms (more on that below). In the US, many real estate buyers, especially in residential real estate, try to pay 20% down payment (even when the requirement is not that high) so they can enjoy lower interest rates, lower monthly mortgage payments, and a waiver of private mortgage insurance (PMI).

Though down payments are very common in real estate transactions, you can still buy commercial property with no money down by exploring creative financing solutions like seller financing, lease-to-own transactions, seller-provided down payment, cross collateralization, and subject to the current mortgage transactions.

Many of these strategies also apply in residential real estate.

How the down payment is handled

The down payment is used immediately to reduce the loan amount the lender needs to advance to the borrower. In other words, the down payment affects the loan-to-value (LTV) or loan-to-cost (LTC) ratio.

For example, if the home’s purchase price is $10 million and the borrower has made a down payment of $2 million (20% of the purchase price), then the lender only needs to lend them $8 million (80% LTV). This is the amount that the purchaser will spread out over the following years, based on the terms of the mortgage.

Furthermore, the down payment, together with the loan advanced by the lender, goes directly to the seller of the property.

Down payment for a property is largely non-refundable if the deal is unsuccessful because of the purchaser. At the point of securing a mortgage and making a down payment, the buyer must have been fully convinced of their interest in the property.

“It’s not uncommon that, in the event that the buyer is unable or unwilling to finalise the order, the down payment is not refundable,” adds Sum Up, a point-of-sale and invoicing company. “If the buyer cancels for any reason, the down payment might not be returned.”

In this case, many buyers prefer to continue with the process and then refinance the mortgage later on.

How does the use of down payment differ in commercial and residential real estate?

Since there are many government-backed loan programs that support homebuyers, the down payment can be very low in residential real estate (as low as 3-5% in some cases).

Though government-backed programs exist in CRE, they are often limited in availability, which makes the typical CRE down payment higher.

For example, while down payment in residential real estate can range from 3-20%, depending on the loan type, it is usually a minimum of 20-30% in CRE, according to Katz.

3. Earnest money vs down payment: Similarities and differences

Now we are back to the most important question: Is earnest money different from down payment?

The simple answer is that they are not the same. We can explicate this further by considering six differences between earnest money and down payments based on everything we have said above.

But before that, let’s consider a few similarities.

Earnest money vs down payments: The similarities

The first similarity is that they both signal the buyer’s commitment to see the deal through. EMD signals this commitment at the signing of the purchase contract and the down payment at the close of the deal.

Secondly, and related to the first point, they both signal the buyer’s ability to complete the transaction. The seller becomes more confident that the deal will not collapse when the buyer can make the relevant earnest money deposit and down payment.

Third, though they both have average rates that are normative, they are still subject to negotiation. In both cases, sellers and buyers can negotiate lower or higher rates, depending on what is beneficial to them.

Earnest money vs down payments: The differences

Having clarified the similarities, let’s turn to the six differences between earnest money and down payments:

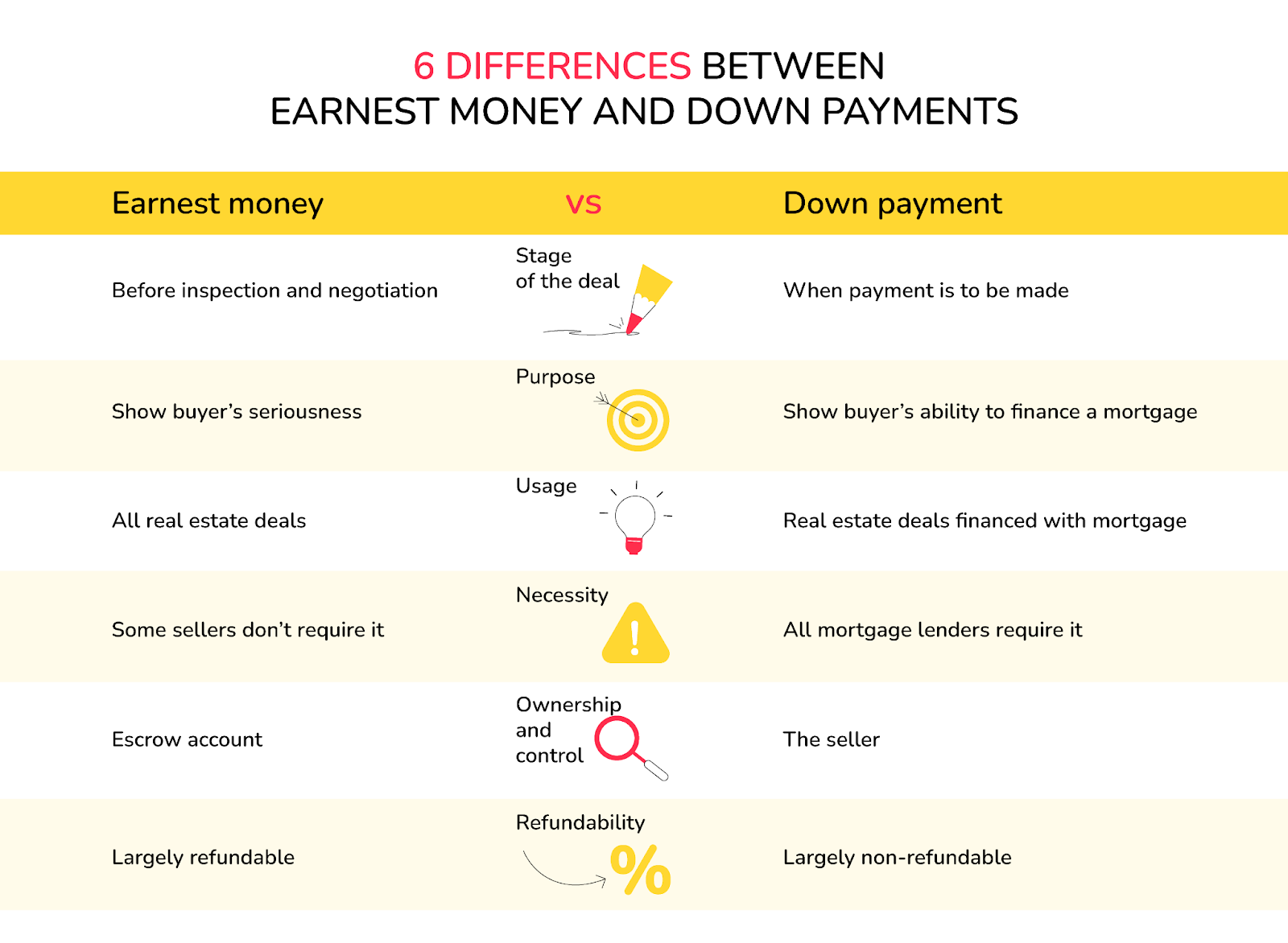

- Stage of the deal: One difference between earnest money and down payments is the stage of the deal at which they are required.

While soft deposit money plays a role at the very beginning of the sales conversation – before inspection and negotiation – a down payment is required once the deal has been finalized, terms have been agreed upon, and an initial payment is required.

“EMD gets you to the table and buys you due diligence time, but the down payment is what actually transfers ownership,” according to Brett Sherman, a real estate broker at Signature Realty, a CRE agency in Miami. “Think of EMD as your entry fee and the down payment as your actual bet.”

- Purpose: Sellers demand earnest money as a show of commitment so that negotiation and inspection (personal checks of the property) can proceed.

On the other hand, it is mortgage lenders that demand a down payment as evidence that the buyer has the financial wherewithal to service the mortgage loan.

Sherman gives an example where a buyer increasing their EMD from 1% to 3% led the seller to restructure the closing timeline. It was a sign that the buyer was serious about the deal.

However, he pointed to instances when the EMD was locked in (and the seller is convinced the buyer is serious), but the deal still fell off because the buyer couldn’t provide the required down payment.

- Usage: Earnest money can be applied to the closing costs of the deal or the down payment. That is, it can be used as credit to pay a part of the closing costs or down payments.

In contrast, the down payment is only used to reduce the amount the buyer needs to borrow from the mortgage lender to close the deal.

- Necessity: Not all sellers require earnest money. There is currently no law mandating it. However, it is a common requirement, especially in very competitive markets. And buyers themselves are suggesting it as a way to gain a competitive advantage.

Conversely, all mortgage deals require some amount of down payment. Though you can get a lower requirement (especially for first-time home buyers and other users of government-guaranteed loans), get the cash from the seller, or use cash substitutes, you still have to pay some down payment.

Similarly, while earnest money can apply to all real estate deals (whether paid for by cash or mortgage financing), down payment only applies to real estate deals financed with commercial property or home loans.

- Ownership and control: Earnest money is usually held with an escrow or title company. If the deal falls through, it is refunded to the buyer or given to the seller, depending on the circumstances. If the deal succeeds, it can be used to pay closing costs or applied to the down payment.

On the other hand, the down payment is owned and controlled by the seller as soon as it is paid.

- Refundability: Another difference between earnest money and a down payment is refundability.

Earnest money only grants the buyer an option to buy. Consequently, the buyer can be refunded if they refuse to go on with the deal due to previously agreed contingencies or the seller pulling out of the deal.

In contrast, the down payment is non-refundable if the purchaser is the reason the deal fell through.

These six differences can be visualized in the chart below:

Why earnest money and down payments are not the same thing

Is earnest money the same as a down payment? Not at all.

Yet, there is a reason why many people are confused about the two.

As we have seen, the earnest money deposit can be applied towards the down payment or closing costs if the deal succeeds, depending on the agreement in the purchase contract.

There are even circumstances where the amount required for the down payment can be the same as the amount paid earlier as earnest money.

For example, suppose the seller requires a 10% earnest money deposit for a property worth $6,000,000. Suppose also that this is an SBA 7(a) loan and you negotiated a 10% down payment. In this case, the same $600,000 you paid to the escrow at the beginning can be given to the seller as a down payment at closing.

But does that mean earnest money is a prepaid down payment? No!

The only thing we can imply from this is that the earnest money deposit can be used for the down payment (in part or in whole). But we have seen that the earnest money deposit can also be used for other purposes – to pay closing costs, for example. Does that mean that it is the same thing as the closing cost? No!

Consider an example from a different context. Suppose a college requires that students pay a certain amount as a caution fee or safety deposit (in case they damage any of its properties).

If the student doesn’t spoil anything, the money paid can be given back to them or applied to their student loan repayment. On the other hand, if they spoil anything, they forfeit all of the money.

Suppose student A didn’t spoil anything and elected to use the money to cover a portion of his outstanding student loan. Can we say the caution fee is the same as a student loan repayment? No! It can only be used for that purpose depending on the circumstances.

Thus, while the amount paid for the two can be similar in some circumstances, and the earnest money deposit can be applied towards the down payment, they are two different things that require different plans.

Why have we labored to clarify the earnest money vs down payment confusion? For the simple reason that understanding the differences will help you make clearer plans.

Consider the issue of timing, for example.

If all you think about is securing a down payment when it’s time to close, you will face a rude awakening when the seller does not allow you to inspect the property or negotiate its price without paying a soft deposit.

This implies that you have to start working on securing the earnest money deposit even before you think about the down payment.

Also, there are circumstances where you get a low earnest money requirement (say 2% of the purchase price) but a high down payment requirement (say 20%).

In this case, securing the earnest money is not a call to rest on your laurels. Even if you apply it to the down payment, there’s still 18% of the purchase price left to secure.

4. How to secure earnest money and down payment for commercial real estate deals

Due to personal or general economic conditions, many real estate investors sometimes struggle to come up with the cash needed for earnest money and down payments.

Does it then mean that such investors are cut off from the commercial real estate market?

Not necessarily.

Regarding down payment, we have seen that there are many creative ways to finance a commercial property without worrying about liquidity: seller financing, lease-to-own transactions, seller-provided down payment, cross collateralization, and subject to the current mortgage transactions, among others.

What about earnest money?

With Duckfund, you can apply for the earnest money deposit you need in less than 2 minutes and get the cash delivered to an escrow within 48 hours.

We provide you with as much earnest money deposit as you need, without requesting your credit score or a credit report.

If you operate in competitive markets, you can propose higher EMD amounts to gain a competitive advantage and enjoy better terms. You can also secure larger EMDs to reduce the amount of cash you will need to make a down payment when it’s time to close the deal.

Duckfund also allows you to secure EMDs for multiple concurrent deals. This can help you quickly build your CRE portfolio without being held back by liquidity struggles.

[Do you want to close multiple real estate deals even when you are illiquid? Sign up for Duckfund’s earnest money deposit financing and get the funds you need within 48 hours.]

Takeaways

- Earnest money is not a down payment. It is a good-faith deposit paid early to show commitment, while a down payment is required at closing in mortgage transactions.

- Earnest money can be refundable under certain conditions. Down payments are generally non-refundable if the buyer backs out.

- Earnest money may be applied toward the down payment or closing costs. But that does not make it the same as either.

- Investors must plan for both separately. Securing earnest money early and preparing for the down payment later are two distinct financial steps.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence