10 Ways How to Buy Commercial Property - With No Money Down (2026)

Nothing is more frustrating for a commercial real estate (CRE) investor than finding the perfect property in the ideal location, only to have no money to purchase it.

Even with mortgage financing, CRE investors need to provide a soft deposit (to inspect the property and negotiate its price), make a down payment (to secure a loan), and pay closing costs (to complete the transaction).

There is no denying that liquidity is significant, especially in prime markets, and temporarily cash-strapped investors may seem to be at a disadvantage.

Yet, an understanding of how to buy commercial property with no money can help commercial real estate investors (beginners and veterans) overcome temporary illiquidity and build profitable portfolios even in prime markets.

In this article, we consider 10 options you can consider if you don’t want to stop exploring profitable CRE deals even when you are temporarily illiquid.

10 ways to buy commercial property with no money

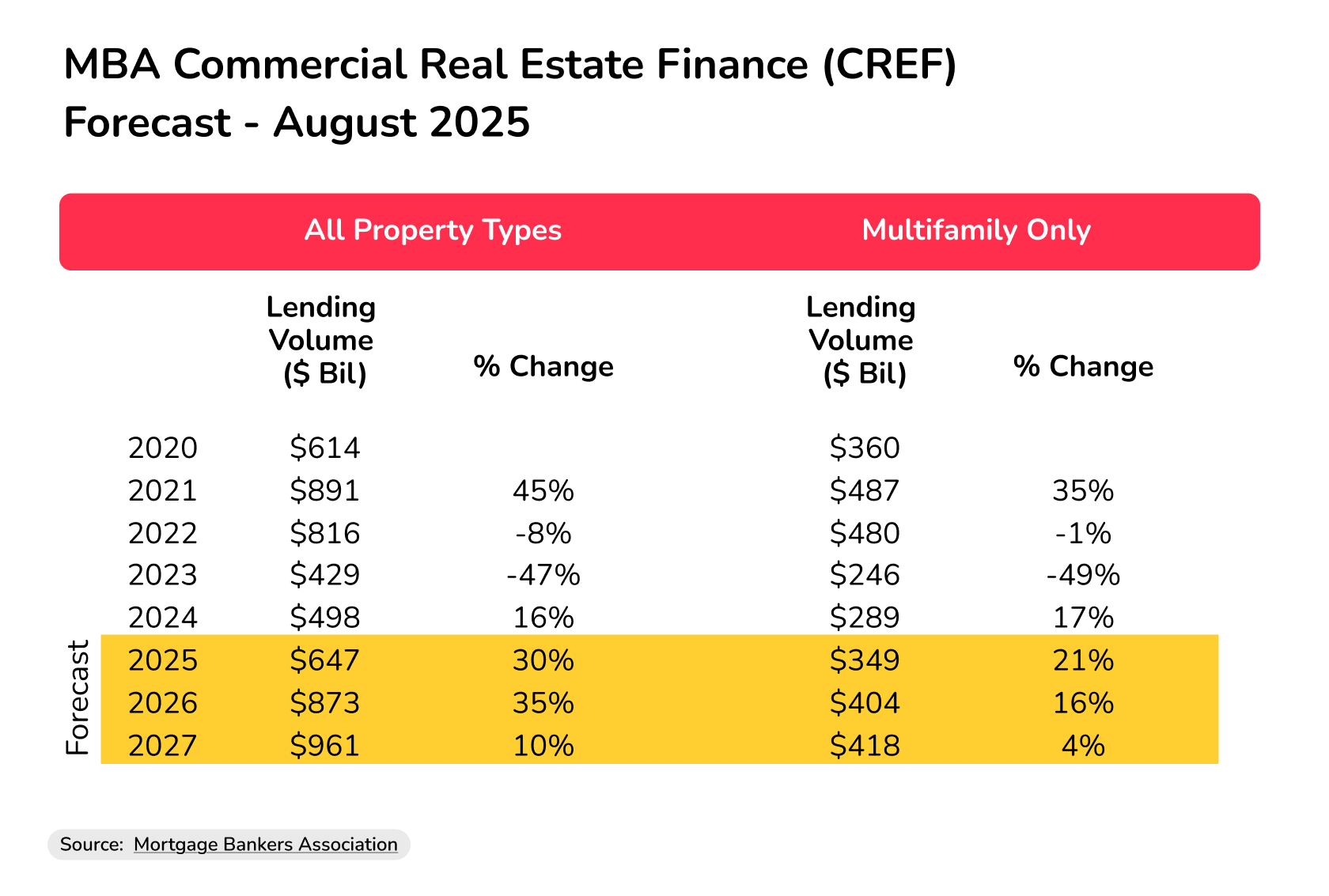

2025 was a year of strong recovery for the CRE market. Deal flow is rebounding, and they will probably reach 2016 levels in 2026, according to GlobeSt, a commercial real estate blog.

Lending volume is projected to grow by 35% in 2025 and 30% in 2026, according to the Mortgage Bankers Association, a trade association of the real estate finance industry.

CRE Lending Volume Forecast

Source: Mortgage Bankers Association

Though banks are gradually easing lending standards, with loan-to-value (LTV) ratios of 56% for nonresidential CRE and 62% for multifamily assets, private investors still dominate CRE investing activity. About 60% of all deals in H1, 2025, came from private investors.

This implies that going into 2026, CRE investors and developers may need to keep prioritizing private and creative financing strategies while waiting for traditional lending to become more generous.

Moreover, the kind of flexibility required to buy commercial property with no money is not available with traditional lending. As a temporarily illiquid investor, your focus should be on these private and creative financing strategies.

Below are 10 options you can consider:

1. Rent or lease to own

A lease-to-own arrangement is a popular option you can pursue if you are interested in how to buy commercial property with no money down.

This arrangement comes in two forms: a lease-option contract that gives you the right to purchase a property you are renting at the end of a given period and a lease-purchase contract that imposes an obligation to buy.

Unlike a regular rental property lease, a part of the rent you pay will be credited towards the future down payment or the eventual purchase price.

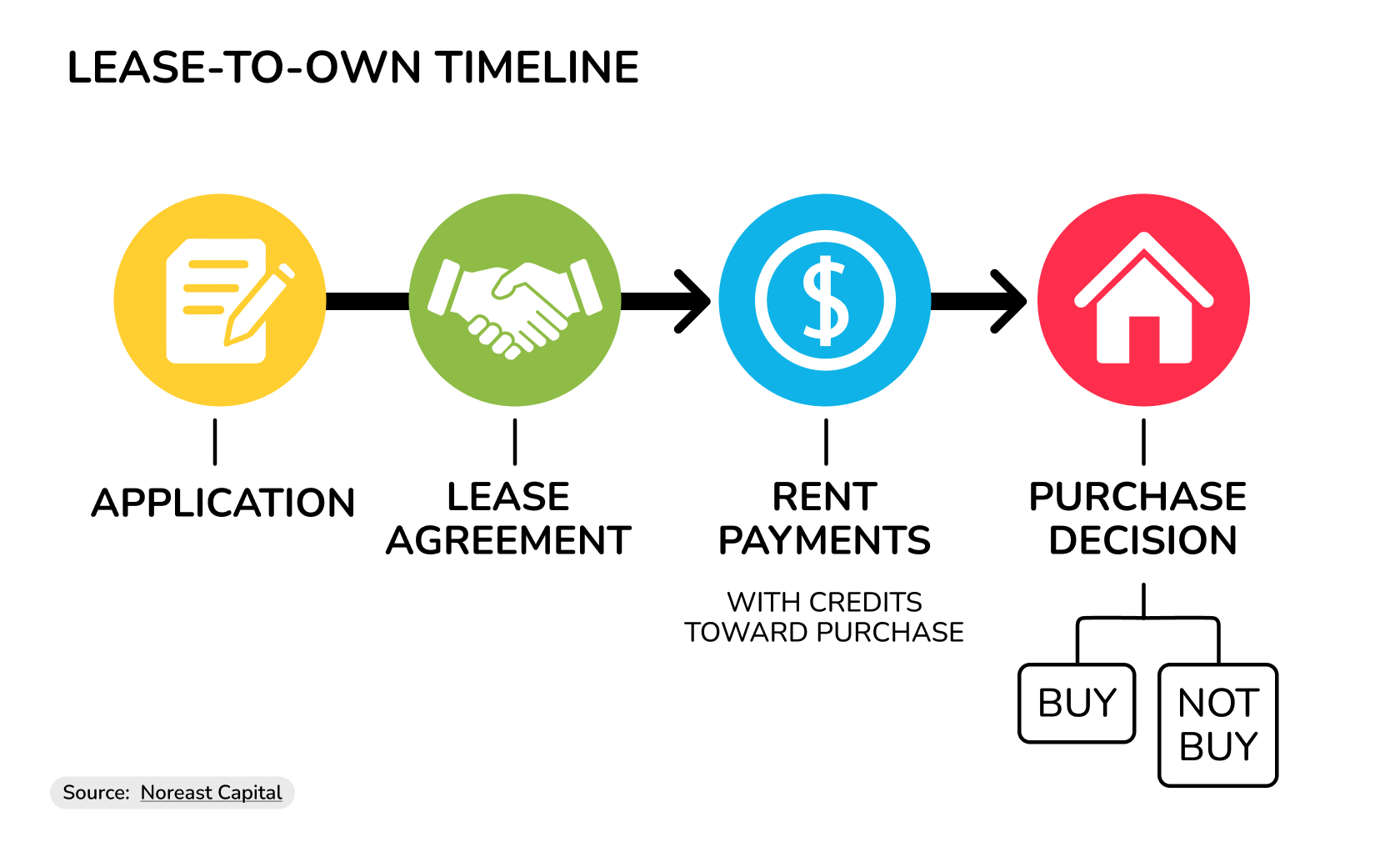

Lease-Option Contract Timeline

Source: Noreast Capital

The eventual purchase price would be specified at the beginning of the lease, so you will know what you are working towards.

The right to purchase the property at a future date comes at a price – the option premium. This fee is usually non-refundable. If you choose to buy the property, some sellers will allow you to apply the option fee to the property value.

An important point to note is that most of the terms that will apply to these contracts are negotiated at the beginning. Therefore, you will need to be sure they are favorable before signing on the dotted line.

If you don’t also have enough money to pay the monthly rent of the lease, you can do a lease arbitrage – rent it out to someone else. You can even rent it out at a higher price than what the landlord demands from you.

However, you need to agree with the landlord before executing a lease arbitrage.

Pros of lease-to-own arrangements

- Save towards a down payment: Temporarily illiquid investors can gradually save towards the down payment they need to finance a mortgage.

- Build equity: In some cases, rent credits can be applied towards the property’s purchase price, which means every rent payment is building equity.

- Flexibility: With lease-option contracts, you can decide to eventually purchase the property or not.

]Cons of lease-to-own arrangements

- Non-refundable payments: In most lease-to-own arrangements, option fees and rent credits are non-refundable. Thus, you will incur some financial loss if you decide not to exercise the option.

- Market risk: If the property’s price rises within the lease period, then agreeing on a lower purchase price at the contract’s beginning becomes beneficial. However, if the real estate market slumps and the property’s price falls, then you will end up paying a premium for the property.

- Complex contracts: Lease-to-own contracts have many components that sellers and buyers have to negotiate. You might need a real estate attorney to handle the complexities.

2. Seller financing

CRE investors started to discover and rediscover creative financing options when the high interest rates of the post-COVID-19 global economy tightened traditional liquidity sources.

One of these discoveries is the importance of seller financing in commercial real estate.

“Traditional lending remains tight due to high interest rates, so buyers are turning to alternative financing,” according to CRE Daily, a real estate blog. “Seller financing, once mostly used for smaller deals, is now more common across all property types.”

Seller financing (owner financing) is an arrangement where the property owner is also the lender or mortgage financier. Thus, instead of making payments to a bank, you make them to the property owner.

One advantage of seller financing is its flexibility. You can negotiate no-down-payment CRE loans with sellers, something that would be harder with banks.

However, this flexibility can come with a higher interest rate or purchase price. In other words, the seller needs to be compensated for the decision to ignore down payments.

Nevertheless, depending on the past relationship you have with them, you may still pay the same price and be subject to the same interest rate, even with no down payment.

Also, most seller financing deals will require a large balloon payment to complete the purchase price after about three to five years. When this time comes, you can refinance with a bank or other CRE lenders.

Pros of seller financing

- Flexible terms: Negotiating with the seller (especially motivated sellers) allows more flexibility compared to a financial institution.

- Faster closing: These deals don’t impose difficult requirements, which makes them easier and quicker to complete.

Cons of seller financing

- Higher interest payment: Flexible terms can come at the cost of a higher interest rate.

- Foreclosure risk: Most seller financing deals give the seller the right to foreclose if the buyer cannot meet up with the payments.

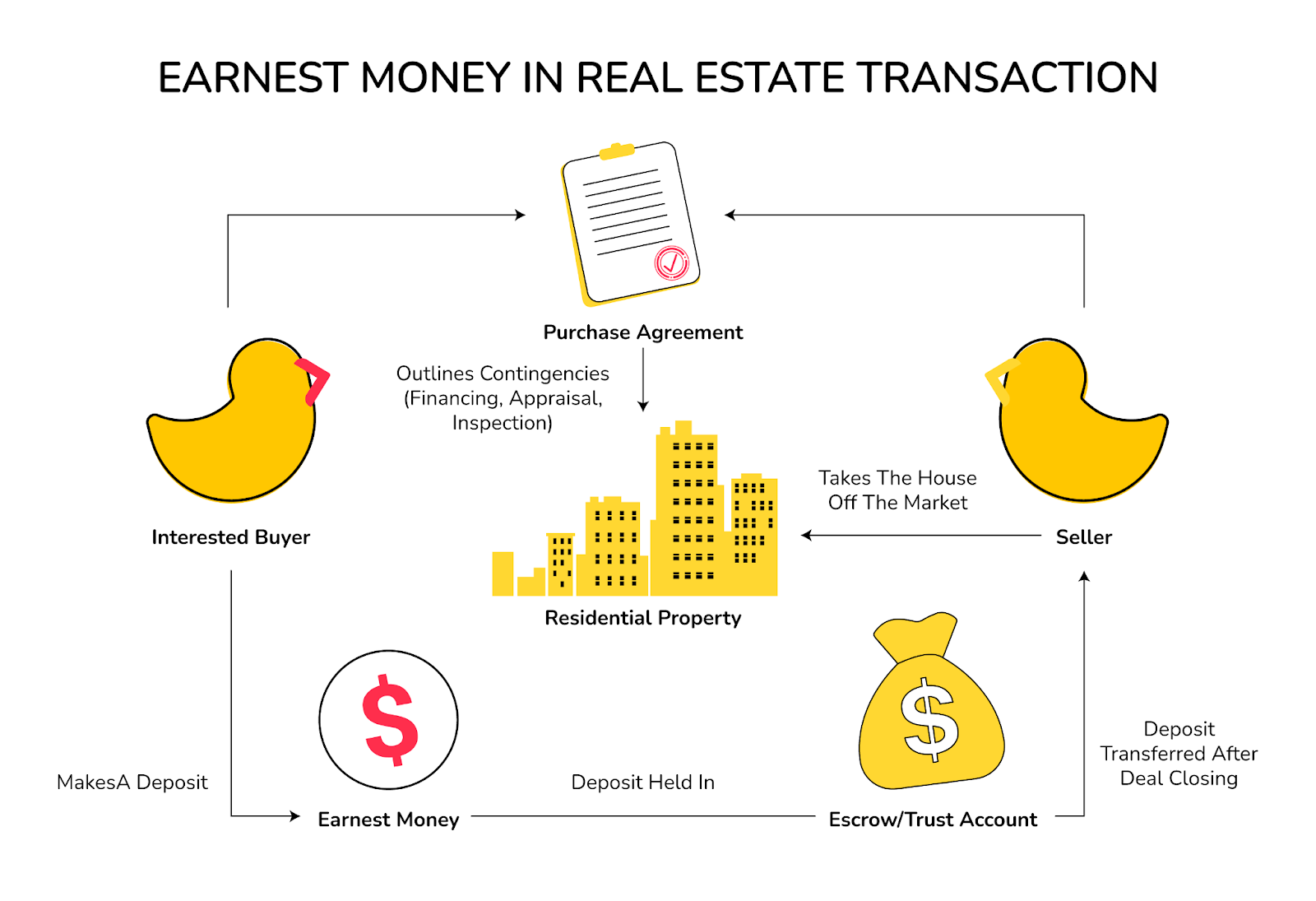

3. Soft deposit financing

Soft deposit financing is a financing arrangement where financing companies help CRE developers and investors pay soft deposits to the relevant escrow.

These deals are structured in a way that makes it easy for investors and developers to decide whether to proceed with a given deal without financial losses.

How does this process work? Below is a snapshot:

- The investor successfully applies for soft deposit financing

- The financing company creates an LLC and a call option agreement between itself and the borrower.

- It is this LLC that signs the commercial real estate purchase and sale agreement and wires the soft deposit to an escrow account.

- If the borrower decides to continue with the deal, they will wire the soft deposit back to the financing company, after which they will possess a 100% stake in the LLC and take control of the purchase and sale agreement.

- If the buyer decides not to go forward with the real estate deal, the financing company will annul the purchase and sale agreement and recover the deposit amount from the escrow account.

How Soft Deposit Financing Works

With this unique system, you can consistently gain access to the soft deposit you need to register an interest in a property of your choice and acquire a purchase option in it.

Consequently, you can buy commercial properties of your choice with no money down.

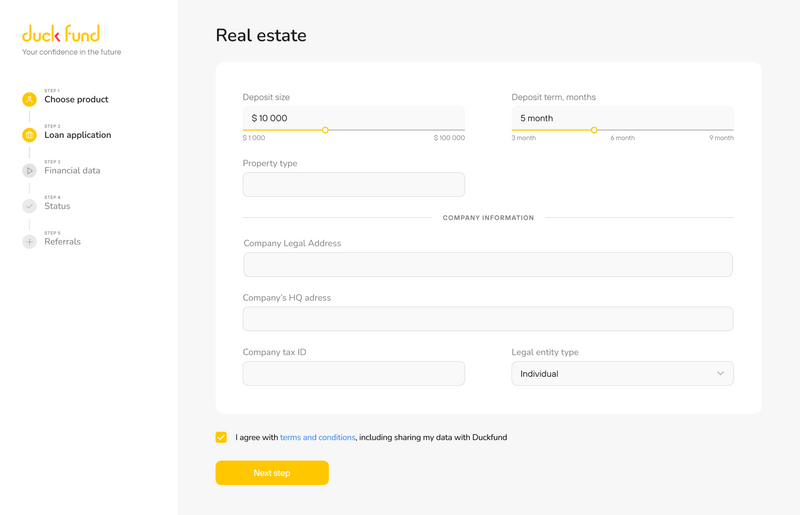

Duckfund is one company providing such soft deposit financing for real estate investors. We have a smooth and fast application process that takes just two minutes. Also, we approve applications within 24 hours (no credit reports required) and release funds within just 48 hours.

Applying for Soft Deposit Financing on Duckfund

We also provide special terms for developers: after the fourth month of the due diligence period, you will pay a lower financing fee.

More importantly, we support investors and developers operating in competitive markets. You can propose a higher soft deposit amount to sellers in such markets, and we will fund it.

Also, we provide soft deposit financing for multiple simultaneous deals. You don’t have to wait to secure one deal before you reapply. We want you to build a portfolio of many profitable real estate investments at the same time.

4. Cash substitutes

Cash substitutes are an alternative if the higher interest rate that comes with seller-provided CRE loans with no down payment is a concern.

Unused properties (cars, appliances, furniture, etc.) and services (accounting, valuation, and legal, etc.) can take the place of cash down payment.

Pros of cash substitutes

- No interest rate or purchase price jack: With cash substitutes, you don’t have to compensate the seller with a higher interest rate or purchase price.

Cons of cash substitutes

- Difficult valuation and negotiation process: The seller might reject what you consider valuable. Even if they accept it, your valuation of it might differ. All of these can lead to protracted negotiations.

4. Seller-provided down payment

Sellers can also support those seeking how to buy commercial property with no money down by offering to pay the down payment needed to secure a mortgage deal.

By now, you are probably asking: “What’s the catch?” You are right to ask that question because there is usually a catch: a higher purchase price.

For example, suppose you want to purchase a property selling for $1,000,000 and with a 10% down payment requirement. If you don’t have the down payment, the seller can offer to make the payment to the mortgage provider.

However, instead of $1,000,000, the seller can budge the price to $1,200,000. In this case, the seller will make the $120,000 down payment. This higher purchase price would then mean higher monthly mortgage payments for you.

For the seller, this is a good deal, since they are now receiving $1,080,000 ($1,200,000 + $200,000 - $120,000) instead of the original $1,000,000.

Pros of seller-provided down payment

- Flexibility: Buyers and sellers can negotiate the impact the seller-provided down payment will have on the purchase price.

Cons of seller-provided down payment

- Higher monthly payments: By paying a higher purchase price, you will have to cope with higher monthly payments.

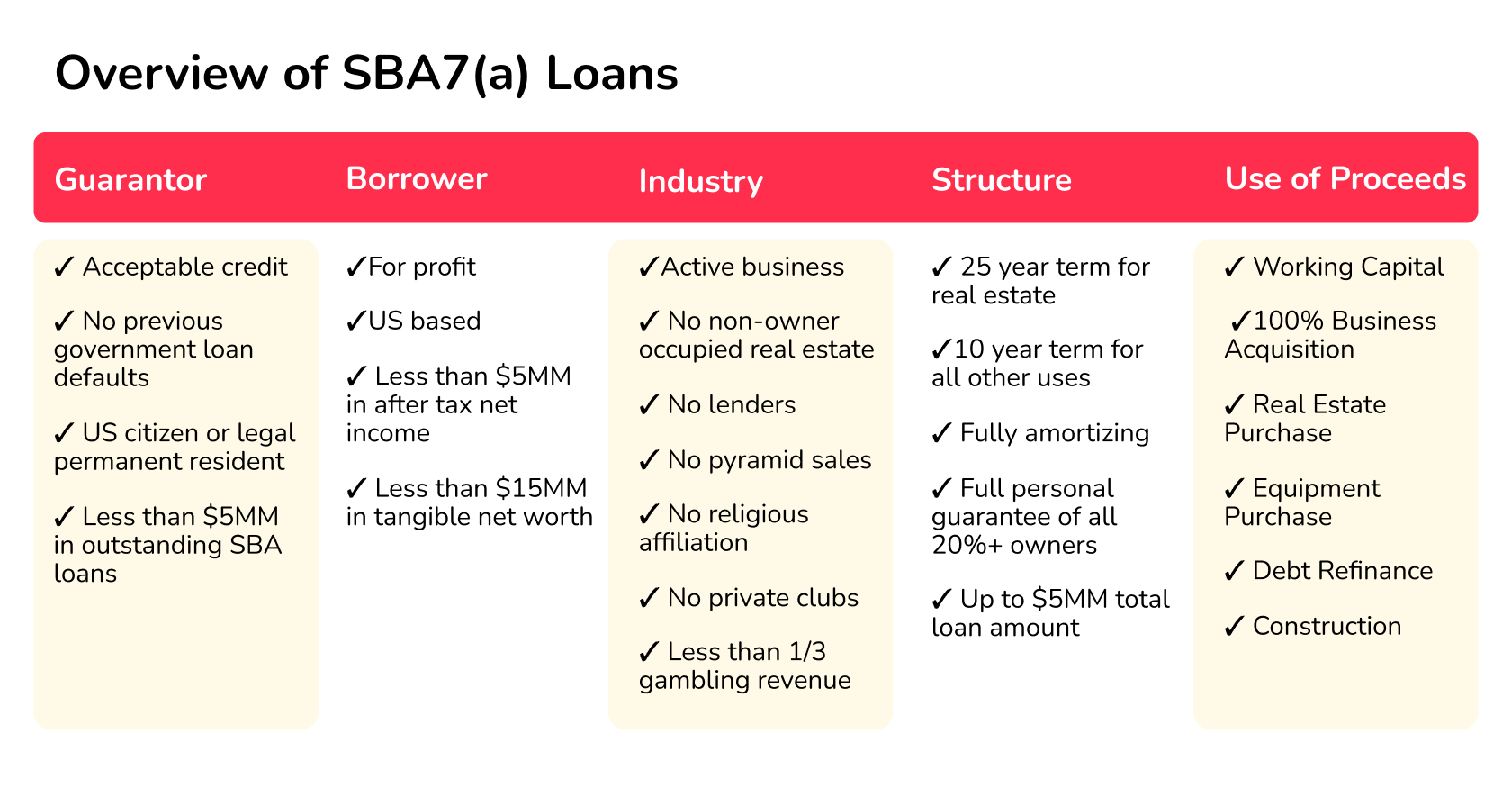

5. Government-backed financing

The government guarantees provided by SBA loans reduce the risk exposure of lenders and make them more willing to offer loans to small businesses.

In a market where traditional lenders are still cautious, as experts expect more CRE sales and foreclosures in 2026 due to the debt maturity wall, SBA loans will become even more important.

The SBA itself does not require a down payment; the terms of the loan are left to the lender.

“Because the bank or lender is providing the loan, they’re in charge of the requisite down payment amounts for an SBA 7(a) loan,” according to the SBA. “There’s no strict down payment amount set by the SBA or any other institution, but lenders often request 10% or more for higher-risk businesses.”

However, a government guarantee and the high standards required to qualify for these loans (strong personal credit, strong business financials, 1.25X debt service coverage ratio, strong cash flow, etc.) mean that some lenders are willing to offer financing without requesting a down payment.

The SBA 7(a) loan is of the most interest to you as a CRE investor.

Loan amounts can go up to $5 million (for renovation, acquisition, refinancing, and improvements), with repayment terms up to 25 years. Interest rates charged by lenders are also capped by the SBA.

Source: Windsor Advantage

These loans require that at least 51% of the property of interest should be owner-occupied; that is, they won’t finance purely investment properties. However, you can refinance the properties down the line and turn them into full investment properties.

Pros of government-backed financing

- Long repayment terms: This is beneficial for investors who prefer long repayment terms and small monthly payments.

- Greater accessibility: The government guarantee makes lenders more willing to lend.

Cons of government-backed financing

- No-down-payment CRE loans are scarce: Though these options are available, they are scarce.

- Requirements can be stringent: Though more accessible than traditional bank loans, they are no less stringent.

6. Subject to the current mortgage

Subject to acquisitions is one of the creative financing methods open to those seeking how to purchase commercial property with no money.

Instead of looking for a down payment to finance a new mortgage, you can take over the old mortgage that the property owner (seller) is currently servicing.

This is often an option when the seller is in a bad financial situation and can’t continue payment, or they have lost interest in the property and are not willing to fork out more mortgage payments.

The loan stays in the seller’s name, but you take ownership of the property and agree to complete the mortgage payments.

Since this is an existing mortgage, you will not make any new down payment to the lender. However, the seller will usually ask for an upfront cash payment to compensate for the equity they have built in the property.

Yet, there are instances where the seller is motivated enough (due to impending foreclosure, for example) to sidestep the upfront payment, ask for a lower amount, or accept cash substitutes.

Pros of subject-to-the-current-mortgage deals

- Flexibility: You can negotiate a lower upfront payment, cash substitutes, or the removal of the upfront payment requirement.

- Current mortgage may be favorable: The current mortgage may have locked in a low interest rate or other terms that are better than what subsists in the current market.

Cons of subject-to-the-current-mortgage deals

- Due-on-sale clauses: Most mortgages have a clause that permits the lender to demand full repayment if the property’s ownership changes. Though lenders rarely exercise the right, the risk remains.

- Complexity: Structuring such deals can be quite complex.

7. Cross-collateralization

Cross-collateralization is a financing agreement where the borrower pledges multiple assets as collateral for a loan.

It is often used as a way to secure a larger loan amount.

However, cross-collateralization can be another way to secure CRE loans with no down payment.

Since both collateral and down payments serve to reduce the lender’s risk exposure, some of them might be willing to swap one for the other.

However, such flexibility is usually available only with private lenders rather than traditional financial institutions.

Pros of cross-collateralization

- Increase borrowing capacity: In addition to exploring how to buy commercial property with no money, cross-collateralization can help you qualify for larger loan amounts.

Cons of cross-collateralization

- Inflexibility: You can’t sell or refinance any of the collateral without the lender’s approval.

- Risk bundling: Default on one property can put all other properties at risk.

8. Partnerships or joint ventures

You can also choose to go the equity route. This involves partnering with other CRE investors or creating a joint venture to invest in a choice property.

The interesting thing about such equity options is that not everyone has to contribute money.

As a sponsor or general partner in a joint venture or syndication, you can contribute by evaluating the property, finding investors, structuring the deal, overseeing the purchase, arranging profit distributions, etc.

There are also sweat equity arrangements where a developer provides project management, construction oversight, and property management while another partner (the capital partner) provides the needed funds.

Pros of partnerships or joint ventures

- Loss sharing: If the property runs at a loss, you can bear the cost with other investors.

- Larger properties: Joint ventures can help to secure large properties that a single person relying on debt financing may not.

You can do this across all CRE types: multifamily, retail, industrial, office buildings, and data centers, among others.

Cons of partnerships or joint ventures

- Structuring partnerships or joint ventures can be difficult: This becomes even more complicated when one partner does not contribute cash.

- Equity dilution: You have to share the profits from the property with other investors.

9. Soft deposit loans

So far, we have focused on the down payment. In actual practice, the soft deposit or earnest money deposit is the first out-of-pocket payment.

It has become a norm for sellers to insist on them before they will allow property inspection or negotiation.

Therefore, this is the first call of duty if you are considering how to buy commercial property with no money down.

You can secure soft deposit loans from private money lenders and P2P (online) lenders. These are more accessible than traditional lenders, and they don’t impose exacting requirements.

However, a higher interest rate is often the price of simplicity and accessibility.

Pros of soft deposit loans

- Accessibility: These loans have lower barriers to entry. For example, they won’t usually ask about your credit score.

- Fast disbursal: These private lenders make money available in no time.

- Flexibility: You can negotiate loan terms, though there is always a cost to this flexibility. For example, if you want a longer term, you might have to pay a higher interest rate.

Cons of soft deposit loans

- Higher fees: They charge higher interest rates compared to traditional lenders.

- Lax regulation: Since private lenders have limited regulation, they can resort to predatory practices and impose onerous terms.

Are you ready to close more commercial real estate deals even when you don’t have the required soft deposit? Sign up for Duckfund’s soft deposit financing and get the cash you need within 48 hours.

Takeaways

- Temporary illiquidity shouldn’t stop you from acquiring your choice commercial real estate investments.

- Creative financing options like lease-to-own contracts, seller financing, government-backed financing, and subject to current mortgage deals, among others, can help you acquire property with no down payment.

- Investors and developers considering how to purchase commercial property with no money can also explore equity financing options like partnerships and joint ventures.

- Soft deposit loans and soft deposit financing (including solutions like Duckfund) can also help secure soft deposit when you are illiquid.

Real Estate

Financing

- Approval within 24 hours

- Fund multiple properties at once

- No full deposit upfront — soft deposit only

- Apply in under 2 minutes

Secure your next development — zero upfront capital required.

Start with Duckfund’s Sign Now, Pay Later model.- No capital commitment

- Close faster

- Scale with confidence